Weekly market focus — The U.S. markets this week will focus on (1) the expected passage by the House on Tuesday of the $1.9 trillion pandemic aid bill, (2) whether T-note yields continue to see upward pressure, (3) whether crude oil prices continue to rise and push inflation expectations higher, and (4) the Treasury’s sale of $120 billion of 3, 10 and 30-year securities.

Overseas, the ECB at its meeting on Thursday is expected to leave its policy variables unchanged but is likely to continue its effort to talk bond yields lower. In China, the markets are watching the week-long National People’s Congress that lasts through this week, which is China’s most important political meeting of the year.

Stock market suffers from higher T-note yields but remains optimistic about an economic recovery — The S&P 500 index last Thursday fell sharply by -1.34% and posted a new 5-week low on concern about higher interest rates. However, the S&P 500 last Friday was then able to stage a pre-weekend recovery rally and closed +1.95%.

Stocks on Friday rallied on the stronger-than-expected U.S. Feb payroll report of +379,000 (vs expectations of +200,000) and the upward revision for Jan payrolls by +117,000 to +166,000 from +49,000. The stock market on Friday also remained optimistic about the economy with the impending passage of the $1.9 trillion pandemic aid bill and the declining pandemic infection rates.

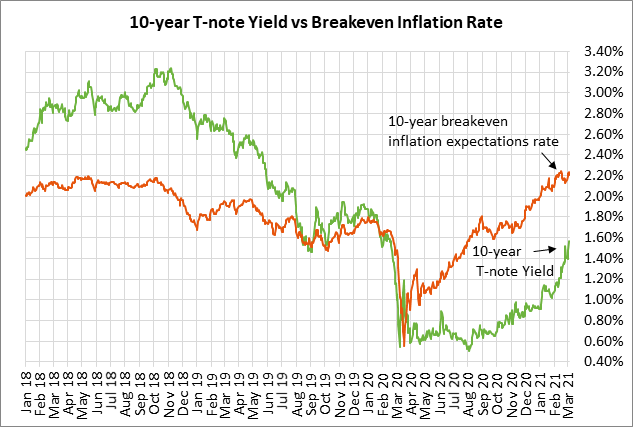

The stock market on Friday was also pleased that the 10-year T-note yield came off its early 1-year high of 1.62% and closed the day little changed at 1.57%. However, the stock market remains concerned about the +66 bp surge seen in the 10-year T-note yield so far this year from the end-2020 level of 0.91%.

The T-note yield has surged due to expectations for a big improvement in the U.S. economy this year due to the fading pandemic and the massive fiscal stimulus out of Washington. T-note yields have also risen sharply due to the sharp rise in inflation expectations, driven by expectations for a stronger economy and by the sharp rally in oil prices seen since last November. The T-note yield last week rose further after Fed Chair Powell said he would only become concerned about the rise in T-note yields if the rise became “disorderly.” That confirmed that the Fed is fine with the recent rise in T-note yields since it is being driven by expectations for a full economic recovery.

Pandemic aid bill is nearly a done deal with the House voting Tuesday — The Senate on Saturday approved the $1.9 trillion pandemic aid bill. The House is expected to take up the revised bill on Tuesday. After passing the bill, the House will send it to President Biden for his signature. That schedule would meet the Democrats’ goal of passing the bill before some unemployment benefits expire this coming Sunday (March 14).

The Senate’s final bill removed the hike in the minimum wage, as expected. The bill left intact the extra $300 per week unemployment benefit but extended it out until September 6. The bill also trimmed the salary limits for the $1,400 stimulus check. The $1,400 stimulus checks and the overall $1.9 trillion of spending is expected to give the U.S. economy a strong boost over the next few months. The consensus is currently for U.S. GDP to show a solid increase of +5.5% this year, overcoming the -3.5% decline seen in 2020.

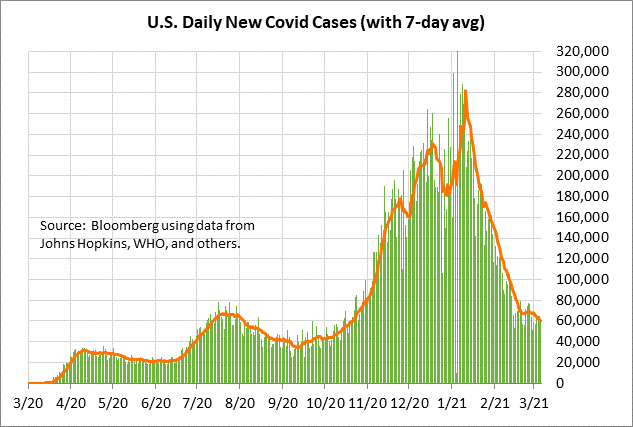

Pandemic improvement slows to a crawl — The 2-month-long plunge in new Covid infections has stalled in the past two weeks, but the new infection level is still moving slightly lower. The 7-day average of new U.S. daily Covid infections fell to a 4-month low of 60,685 on Saturday. That was down nearly 80% from the record high of 281,871 posted in mid-January. However, the current infection level is still near the peak seen last summer and is well above the first peak seen in spring 2020.

The daily vaccination rate last week reached a record high of 2.16 million doses per day. The single-dose Johnson & Johnson vaccine was approved a week ago, and J&J vaccine doses will be flooding into vaccinations centers with a total of 100 million doses expected by the end of June, which by itself is enough to vaccinate 30% of the U.S. population.

The U.S. has so far administered 87.9 million doses, according to the Bloomberg vaccine tracker. So far, 9.0% of the U.S. population has received the 2-dose vaccine regimen, and 17.3% of the population has received one dose, for a total of 26% of U.S. population now having at least some immunity from vaccine doses.

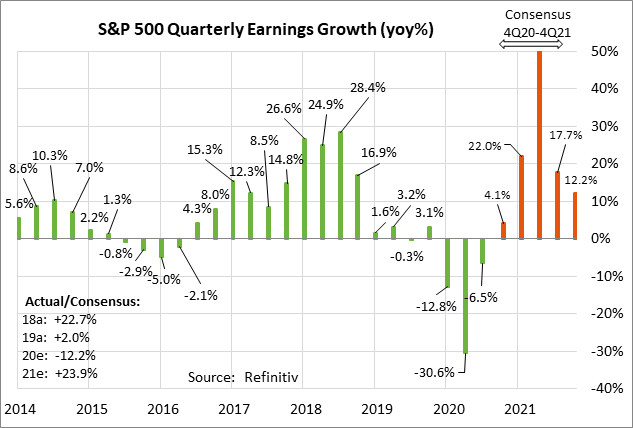

Q4 earnings season finishes off — Q4 earnings season is virtually over, with only 4 of the S&P 500 companies reporting this week. Notable reports this week include Oracle and Campbell Soup on Wednesday, and Ulta Beauty on Thursday.

Q4 earnings reports have been better than expected. Of the 495 SPX companies that have reported thus far, 79.4% have beaten the consensus, which is much better than the long-term average of 65.3% and the 4-quarter average of 75.5%, according to Refinitiv.

The consensus is for SPX earnings growth in Q4 of +4.1% (+8.1% ex-energy), which is substantially better than the consensus of -10.3% as of January 1, according to Refinitiv. On a quarterly basis, earnings growth is expected to pick up sharply due to the low year-earlier base, with +22.0% earnings growth in Q1, +51.2% in Q2, +17.7% in Q3, and +12.2% in Q4. On a calendar year basis, the consensus is for SPX earnings growth of +23.9% in 2021, overcoming the -12.0% decline in 2020.