- Weekly global market focus

- T-note prices stabilize but the markets remain on notice

- Senate begins consideration of $1.9 trillion pandemic aid bill

- Pandemic improvement stops

- Q4 earnings season tails off

Weekly global market focus — The U.S. markets this week will focus on (1) Treasury yields after last week’s upward spike, (2) whether Fed officials this week in various speeches continue to take a laissez-faire approach to the rise in Treasury yields, (3) progress on the $1.9 trillion pandemic aid bill in the Senate, (4) the tail end of Q4 earnings season, and (5) key U.S. economic reports including today’s Feb ISM manufacturing index (expected -0.1 to 58.6) and Friday’s payroll report (expected modest at +180,000).

China’s PMI reports on Sunday were mildly weaker than expected. The Feb manufacturing PMI fell -0.7 to 50.6, weaker than expectations of -0.3 to 50.3. The Feb non-manufacturing PMI fell -1.0 to 51.4, which was weaker than expectations of -0.4 to 52.0.

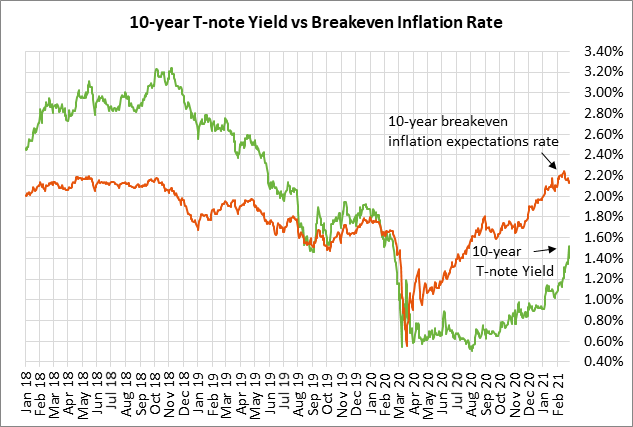

T-note prices stabilize but the markets remain on notice — The 10-year T-note yield last Friday fell back from last Thursday’s 1-year high of 1.61% and closed the day at 1.40%. However, the markets remain on notice that yields are likely to rise in the coming months as the pandemic ebbs and the economy returns to normal. The current 10-year T-note yield of 1.40% is still 52 bp below the pre-pandemic level of 1.92% seen at the end of 2019.

The 10-year T-note market last week temporarily went into a meltdown mode on a variety of concerns. The markets were mainly alarmed by the comments by Fed Chair Powell and other Fed officials suggesting that the Fed is ok with the rise in yields and views it as a positive sign of market expectations for a full economic recovery.

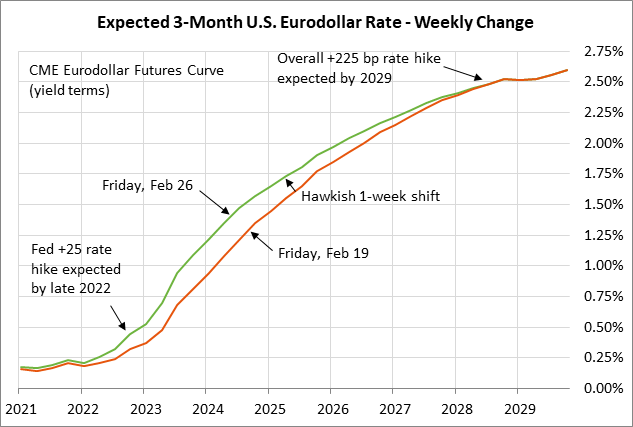

The market took those Fed comments as a sign that the Fed might be willing to taper its QE program and raise interest rates sooner than earlier thought. Indeed, the Eurodollar futures curve on a yield basis rose sharply last week by about +25 bp for the 2022-24 contracts. The market is now expecting the Fed’s first rate hike by late-2022 versus previous expectations of mid-2023.

The sharp rise in T-note yields seen since late 2020 has been due to (1) the emergence of effective Covid vaccines that could end the pandemic by 2022, (2) the massive amount of stimulus passed by Congress, with more on the way, and (3) the sharp rise in inflation expectations. The 10-year breakeven inflation expectations rate is currently at 2.15%, which is just 11 bp below the mid-Feb 6-1/2 year high of 2.26%. The breakeven rate is even +36 bp higher than the pre-pandemic level of 1.79%.

Senate begins consideration of $1.9 trillion pandemic aid bill — The House late last Friday approved President Biden’s $1.9 trillion pandemic aid bill and sent it to the Senate for its consideration. The Senate will likely make some changes that would require the House to pass the revised version. Democratic leaders have promised to get the bill passed before unemployment benefits start running out in just two weeks on March 14.

The main sticking point for the pandemic aid bill is the hike in the minimum wage to $15 per hour, which the Senate parliamentarian has already ruled cannot be in the bill because it violates budget reconciliation rules. The stock market is watching carefully because some Democratic Senators are talking about imposing a tax related to the minimum wage so that it can qualify for budget reconciliation.

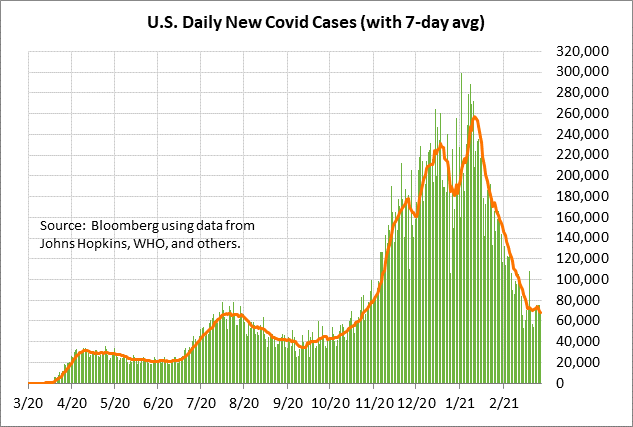

Pandemic improvement stops — The month-long plunge in new Covid infections stalled last week, highlighting the fact that the pandemic is far from over. The pandemic will not be over until the U.S. can reach herd immunity and the level of community transmission has virtually disappeared. At that point, social distancing can largely be abandoned and the economy can return to normal.

The number of new U.S. Covid infections last Monday fell to 54,612, which was just slightly above the mid-Feb 4-1/4 month low of 53,410, according to data compiled by Bloomberg. However, the new infection level then rose through the rest of last week. The 7-day average of new U.S. Covid infections plunged from mid-January through mid-February, but that decline has now slowed to a crawl. Nevertheless, the 7-day average of new daily U.S. Covid infections on Saturday still fell to a 4-month low of 68,203.

The vaccination figures continue to rise, with the U.S. administering 70.5 million vaccine doses so far at a rate of 1.45 million doses per day, according to the Bloomberg vaccine tracker. So far, 6.8% of the U.S. population has received the 2-dose vaccine regimen, while 14.2% of the population has received one dose.

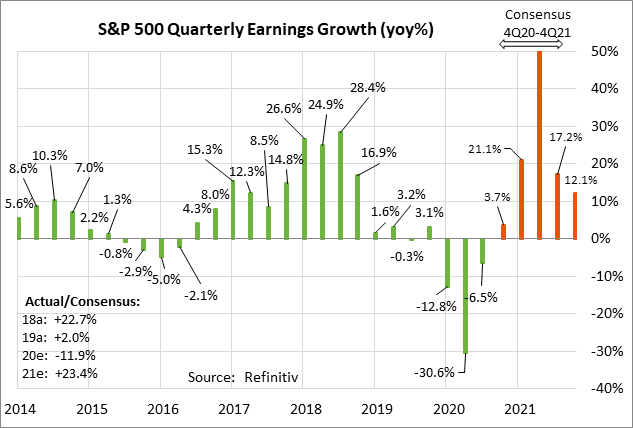

Q4 earnings season tails off — Q4 earnings season tails off this week with reports from only 16 of the S&P 500 companies. Notable reports this week include Target, Ross Stores, and HP Enterprise on Tuesday; Costco, GAP, and Kroger on Thursday, and Berkshire Hathaway on Friday.

Q4 earnings reports have been better than expected, providing support for the stock market. Of the 479 SPX companies that have reported thus far, 80.0% have beaten the consensus, which is much better than the long-term average of 65.3% and the 4-quarter average of 75.5%, according to Refinitiv.

The consensus is for SPX earnings growth in Q4 of +4.2% (+8.2% ex-energy), which is substantially better than the consensus of -10.3% as of January 1, according to Refinitiv. The consensus is for calendar-year 2021 SPX earnings growth to recover by +23.4% after the expected -11.9% decline in 2020.