Markets expect QE tapering to be announced at 2-day FOMC meeting that begins today — The markets are unanimously expecting the FOMC at its 2-day meeting that begins today to announce QE tapering. Fed Chair Powell on Wednesday will deliver his usual post-meeting press conference, but the FOMC is not due to release a new Summary of Economic Projections or Fed-dot forecast until its next meeting on December 14-15.

The Fed has clearly telegraphed that a QE tapering announcement is likely at this week’s meeting. The FOMC in its post-meeting statement at its last meeting on Sep 21-22 said, “The economy has made progress toward these goals. If progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.”

The minutes from that meeting, which were released on October 13, also telegraphed a QE tapering announcement. The minutes said, “Participants noted that if a decision to begin tapering purchases occurred at the next meeting, the process of tapering could commence with the monthly purchase calendars beginning in either mid-November or mid-December. The minutes added, “Participants generally assessed that, provided that the economic recovery remained broadly on track, a gradual tapering process that concluded around the middle of next year would likely be appropriate.”

The FOMC minutes went so far as to lay out the tapering path under discussion, saying, “The path featured monthly reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities.

Fed Chair Powell, in comments delivered on October 22, reinforced the likelihood of a QE tapering announcement this week, although he was careful to reiterate that the Fed is not close to raising interest rates. Mr. Powell said, “We are on track to begin a taper of our asset purchases, that, if the economy evolves broadly as expected, will be completed by the middle of next year.” He added, “I do think it is time to taper and I don’t think it is time to raise rates.”

The FOMC seems convinced that now is the right time to begin QE tapering since the inflation situation has become more of a concern. Fed officials previously insisted that the inflation surge from the economic reopening would be “transitory.” However, the minutes from the Sep 21-22 FOMC meeting indicated that Fed officials were becoming more concerned about inflation. The minutes said, “Most participants saw inflation risks as weighted to the upside because of concerns that supply disruptions and labor shortages might last longer and might have larger or more persistent effects on prices and wages than they currently assumed.”

Mr. Powell, in his comments on October 22, said that supply-chain constraints that have led to elevated inflation “are likely to last longer than previously expected, likely well into next year.” However, he added that “it is still the most likely case” that as those constraints ease, as they eventually will — and as job gains move up — inflation will move back down closer to our 2% goal.”

Atlanta Fed President Bostic has been very vocal about rejecting the Fed’s previous thesis that inflation is “transitory. On October 12, Mr. Bostic said that he thought inflation pressures have lasted too long to still be considered “transitory.” He said, “I believe evidence is mounting that price pressures have broadened beyond the handful of items most directly connected to supply-chain issues or the reopening of the services sector.”

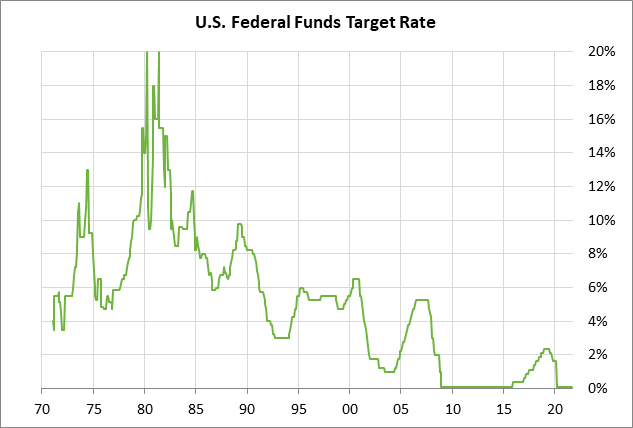

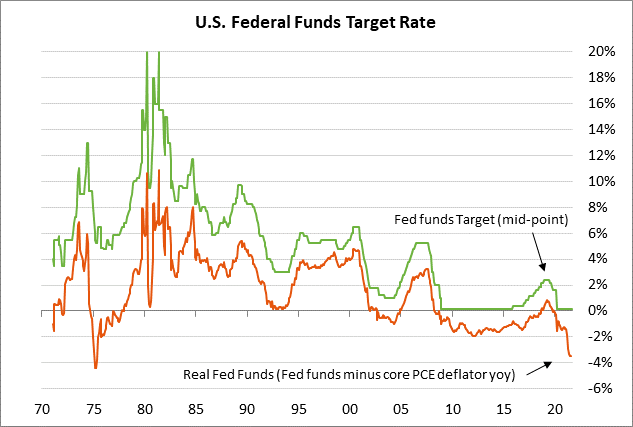

Heightened inflation concerns have led the market to expect the Fed’s first rate hike much sooner than earlier expected. This past summer, the markets were not expecting the Fed’s first rate hike until early 2023. However, markets are now discounting a strong chance of two Fed rate hikes by the end of 2022.

FOMC members at their last meeting on Sep 21-22 turned significantly more hawkish. The Fed-dot forecast from that meeting showed that two more FOMC members were expecting at least one rate hike in 2022, bringing the total to 9 members who were expecting at least one rate hike in 2022. That meant that half of the 18 FOMC members in September were expecting at least one rate hike in 2022, and the other half were expecting rates to remain unchanged. FOMC members have likely turned more hawkish since the Sep 21-22 meeting since the Covid infection figures have dropped by about 60% since that meeting.

For the end of 2023, the dot-plot’s median forecast is for the funds rate to be at 1.0%, implying three rate hikes for a total rate hike of more than 75 bp. By the end of 2024, the median forecast is for a funds rate of 1.75%, which implies a total rate hike of nearly 175 bp.

This week’s FOMC meeting is likely to cause increased market talk about whether President Biden will reappoint Mr. Powell as the Fed Chair when his term expires in less than three months on January 31, 2022.

The markets still think that Mr. Powell has a very good chance of being reappointed despite reports that emerged on October 18 that Mr. Powell sold some $5 million worth of stock from his personal account around October 2020 when the stock market was tanking. However, Mr. Powell said the sales involved mutual funds, not individual stocks. He also said he was fully compliant with the central bank rules and that government ethics officers approved the sales. The markets don’t seem to think those stock fund sales will be an obstacle to Mr. Powell’s reappointment.