- Is the month-long decline in the 10-year T-note yield over?

- Unemployment claims report will be watched for any signs of labor market weakness

- U.S. LEI expected to fade after strong 3-month stretch

- 5-year TIPS expected to produce a negative yield

Is the month-long decline in the 10-year T-note yield over? — The 10-year T-note yield on Wednesday rebounded higher from Tuesday’s 5-month low of 2.163% and closed the day +4.60 bp at 2.214%. The 10-year T-note yield in the past month has plunged by an overall +46 bp.

The sharp decline in the 10-year T-note yield since mid-March has been driven by (1) the weak Q1 economic data, (2) ideas that the Fed will curtail rate hikes when it expects to start reducing its balance sheet “later this year,” (3) the slow-moving Republican agenda which has curbed inflation expectations and expectations for Fed rate hikes to address fiscal stimulus, (4) the unexpected decline in the March core CPI to +2.0% y/y from Feb’s +2.2%, and (5) short-covering in T-note prices by hedge funds and speculators who were previously heavily short T-notes on expectations for T-note yields to move quickly up to the 3% area.

How low can the 10-year T-note yield go? There are potential near-term events that could cause the 10-year T-note yield to go even lower such as: (1) if centrist Emmanuel Macron were to be knocked out of the French presidential race in this Sunday’s first round of voting by far-left Melenchon, setting up a second-round Le Pen-Melenchon contest, (2) if the weak U.S. Q1 economic data starts to spread into Q2, or (3) if geopolitical risks such as North Korea substantially worsen.

The fact remains that despite the 43 bp drop in the 10-year yield to Wednesday’s close from the 2-1/2 year high of 2.64% posted in mid-December, the current 10-year yield of 2.21% is still 38 bp higher than it was on the day before the Nov 8 election (1.83%).

The current 38 bp post-election premium could continue to evaporate if the U.S. economy is starting to see some fundamental weakness or if it appears that Republicans will not be able to pass any tax reform package at all. However, things have not yet become that bad since the Q1 economic weakness was probably just transitory (as the Fed believes) and since the Republicans are likely to eventually pass some version of tax reform. That would mean that the 10-year T-note yield may have already seen the bulk of its near-term drop (barring a knock-out of Macron in Sunday’s French election).

The T-note market is waiting for further comments from Fed officials to see how the Fed is reacting to the current situation. Market expectations for Fed tightening have dropped substantially in recent weeks since the market is now discounting only a little more than two rates hikes (+56 bp) through the end of 2018, which is dramatically more dovish than the Fed-dot forecast for five more +25 bp rate hikes (+125 bp) through the end of 2018. The market is now discounting only a 47% chance of a rate hike at the June FOMC meeting.

We suspect that Fed Chair Yellen will not start softening up her language unless she sees that the Q1 economic weakness is spreading into Q2. However, the markets will be carefully watching for any comments by Fed officials that suggest they are losing faith in the Fed’s dogma of two more rate hikes this year.

Unemployment claims report will be watched for any signs of labor market weakness — Both the initial and continuing unemployment claims series remain in very good shape. Initial claims are only +7,000 above the 44-year low of 227,000 posted in February and continuing claims are only +41,000 above the 17-year low of 1.987 million posted in early March.

However, the markets will be watching today’s report carefully to see if the weak March payroll report of +98,000 was just a fluke or whether it was an early warning signal of impending labor market weakness. Today’s initial claims report is for the survey week of the April payroll report, which boosts the significance of today’s claims report. However, there may also be some distortions in today’s claims report from Easter-holiday seasonal distortions.

U.S. LEI expected to fade after strong 3-month stretch — The market consensus for today’s March leading indicators report is for a small increase of +0.2% m/m. The LEI is due for a slowdown after showing three consecutive months of strong +0.6% gains. On a year-on-year basis, the LEI in February rose to a 1-1/3 year high of +3.1%, up sharply from the +0.7% level seen as recently as Nov 2016.

The strength in the LEI from Dec-Feb should be a positive factor for the U.S. economy. However, U.S. consumer spending slumped in Feb-March and there are concerns that Q1 weakness may turn into something more than the usual first-quarter residual seasonal weakness seen in recent years.

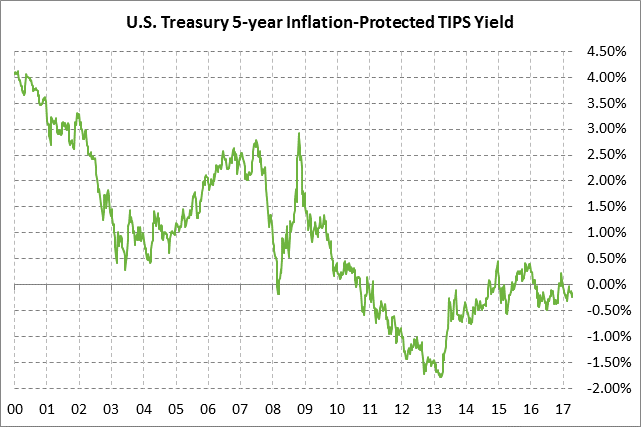

5-year TIPS expected to produce a negative yield — The Treasury today will sell $16 billion of 5-year TIPS in a new issue. The Treasury in recent years has followed a pattern of selling a new 5-year TIPS in April and then conducting reopenings of that issue in August and December. The benchmark 5-year TIPS was quoted at -0.150% late Wednesday afternoon.

The 12-auction averages for the 5-year TIPS are as follows: 2.43 bid cover ratio, $36 million in non-competitive bids, 6.2 bp tail to the median yield, 14.5 bp tail to the low yield, and 49% taken at the high yield. The 5-year TIPS is slightly below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 59.2% of the last twelve 5-year TIPS auctions, which is slightly below the average of 59.5% for all recent Treasury coupon auctions.