- FOMC outcome prompts dovish market response although Fed raises its long-term neutral-rate estimate

- US/Japan trade talk agreement takes Japan tariff threat off the table for now

- President Trump says he will sign spending bills to avert a U.S. government shutdown on Sunday night

- Claims report expected to see distortions from Florence

- 7-year T-note yield falls ahead of today’s auction

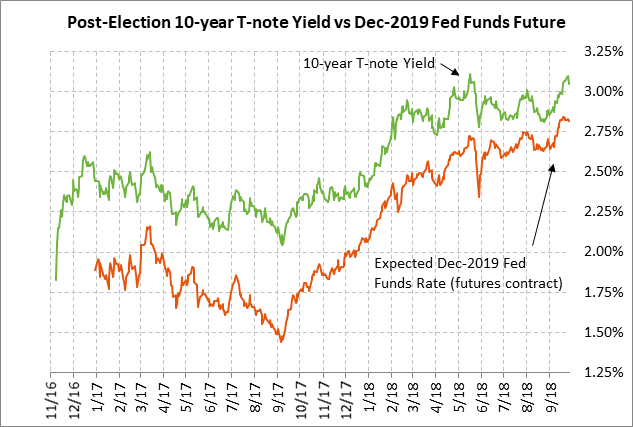

FOMC outcome prompts dovish market response although Fed raises its long-term neutral-rate estimate — The markets reacted dovishly to the outcome of yesterday’s FOMC meeting. The federal funds futures curve was unchanged for the late-2018 contracts but turned slightly more dovish by 2 bp for the late-2019 contracts. T-note yields showed a larger reaction with the 10-year T-note yield falling by -5 bp to 3.05%.

The decline in T-note yields was accentuated by (1) a short-covering rally, and (2) the -0.98% sell-off in Nov WTI oil prices from the EIA report of a +1.85 mln bbl rise in oil inventories, which helped push the 10-year breakeven inflation expectations rate lower by -2 bp to 2.15%.

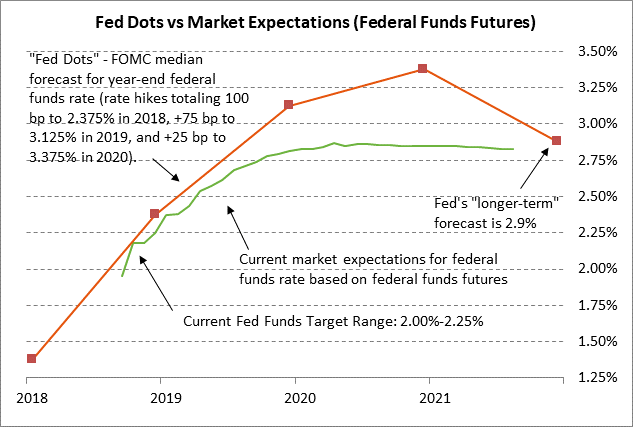

The dovish response to the FOMC meeting was prompted by relief that the FOMC did not boost its Fed-dot forecasts and by the Fed’s decision to drop the description its of monetary policy as being “accommodative.” While Fed Chair Powell said that move had no implications for the future course of interest rates, the markets nevertheless took the action as a sign that the Fed believes the funds rate is not far from the neutral rate. On that note, the FOMC actually took the slightly hawkish action of raising the median estimate of the long-term neutral rate to 3.0% from 2.9%.

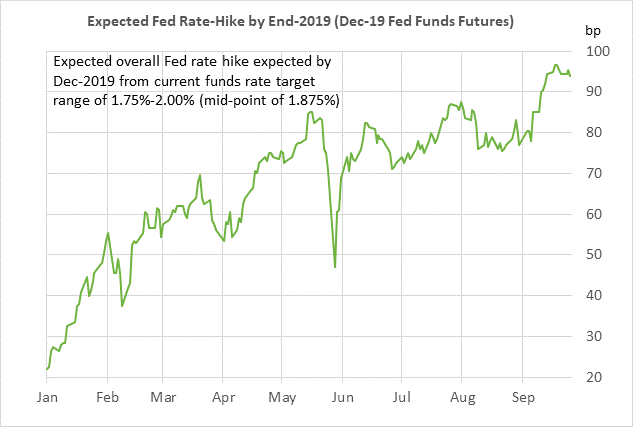

Looking ahead, there wasn’t much change in the market’s outlook for Fed policy after yesterday’s +25 bp rate hike to 2.00%/2.25%. The market is now discounting nearly a 100% chance that the Fed will implement its fourth rate hike of the year at the meeting after next on Dec 18-19. The market then believes the Fed will conclude its rate hike regime with two rate hikes in 2019, leaving the funds rate thereafter near 2.85%. The FOMC, by contrast, currently expects to keep tightening up to a funds rate peak of 3.38%, as reflected in the median Fed-dot forecast.

US/Japan trade talk agreement takes Japan tariff threat off the table for now — President Trump and Japanese Prime Minster Abe after their meeting yesterday in New York announced that the U.S. and Japan agreed to engage in bilateral trade talks focused on autos. Mr. Trump agreed to table his threat of a 25% tariff on Japanese autos while the talks are ongoing. The status of US/Japan trade relations is now similar to that of US/EU relations, where President Trump has agreed not to announce any new tariffs while negotiations are proceeding.

That leaves China and Canada as the market’s main two sources of trade concerns. Canada and the U.S. will presumably continue their NAFTA talks even though they will almost certainly miss this Sunday’s deadline. However, Mr. Trump at any time could announce a U.S. withdrawal from NAFTA and a 25% penalty tariff on Canadian autos.

President Trump on Wednesday had negative words for Canada, saying of Prime Minister Trudeau that, “His tariffs are too high, and he doesn’t seem to want to move, and I’ve told him ‘forget about it.'” Mr. Trump added, “We’re very unhappy with the negotiations and the negotiation style of Canada. We don’t like their representative very much.”

Regarding China, President Trump at any time could officially announce that procedures will begin for slapping tariffs on the last $267 billion of Chinese goods.

President Trump says he will sign spending bills to avert a U.S. government shutdown on Sunday night — President Trump on Wednesday said that he will sign the necessary spending bills to avert a government shutdown starting on Sunday night when the new fiscal year begins even though the bills do not contain his border-wall funding. Congressional Republicans worked hard to prevent a government shutdown and potential political damage just six weeks ahead of the Nov 6 mid-term elections. President Trump will have his chance for a “good government shutdown” on Dec 7 to try to force his border-wall funding when the continuing resolution expires for part of U.S. government operations.

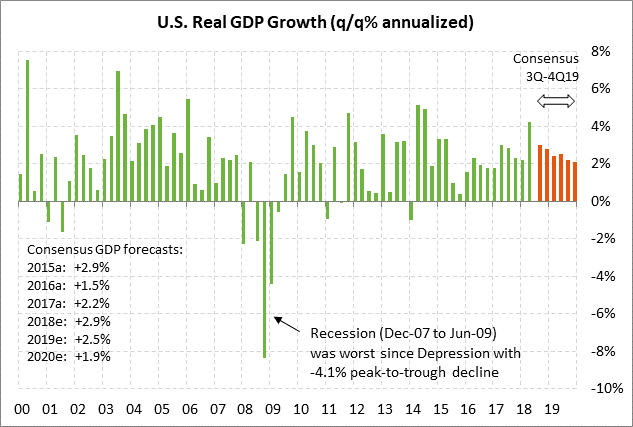

U.S. Q2 GDP expected unrevised — The consensus is for today’s Q2 real GDP report to be unrevised from the last estimate of +4.2%. Looking ahead, the consensus is for real GDP to ease from Q2’s stellar pace to +3.0% in Q3 and +2.8% in Q4. On a calendar year basis, the consensus is for strong GDP growth of +2.9% in 2018 due in large part to fiscal stimulus. However, the consensus is for GDP growth to then ease to +2.5% in 2019 and +1.9% in 2020 as stimulus fades from the Jan 1 tax cuts.

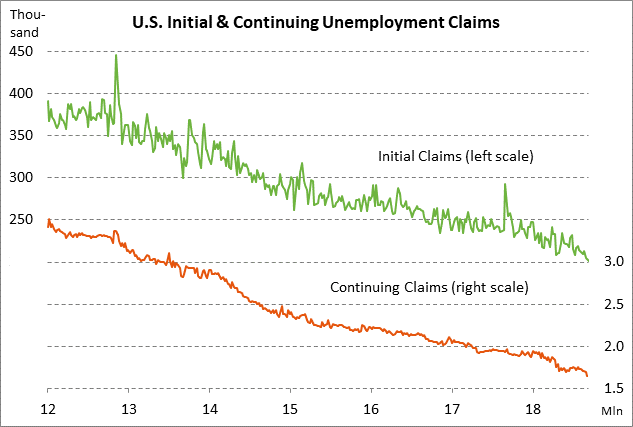

Claims report expected to see distortions from Florence — The unemployment claims data is in very favorable shape with layoffs near multi-decade lows. However, the unemployment claims data is currently being distorted by Hurricane Florence which resulted in significant business disruptions and the temporary closure of unemployment offices. The consensus is for today’s initial claims report to rise +9,000 to 210,000 after last week’s -3,000 drop to a 49-year low of 201,000. The consensus is for continuing claims to rise by +33,000 to 1.678 million, reversing part of last week’s -51,000 drop to a 45-year low of 1.645 million.

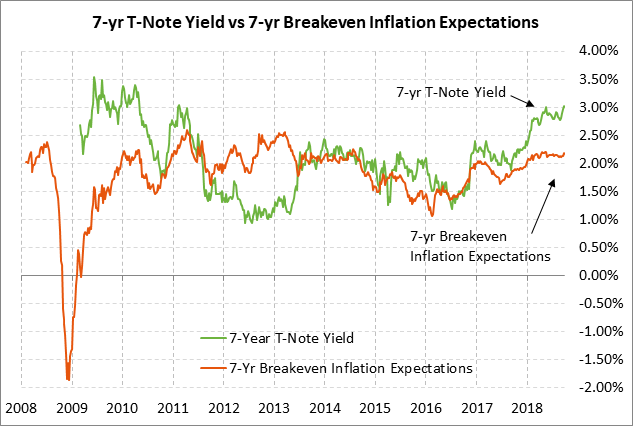

7-year T-note yield falls ahead of today’s auction — The Treasury today will sell $31 billion of 7-year T-notes, concluding this week’s T-note package. Today’s 7-year T-note issue was trading at 3.01% in when-issued trading late yesterday, which is 6 bp below Tuesday’s 4-1/4 month high of 3.07% and 7 bp below May’s 7-1/2 year high of 3.08%. The 12-auction averages are: 2.52 bid cover, $15 million in non-competitive bids, 4.7 bp tail to the median yield, 28.2 bp tail to the low yield, 48% taken at the high yield, and 63.8% taken by indirect bidders (slightly better than the median of 63.5% for all recent Treasury coupons).