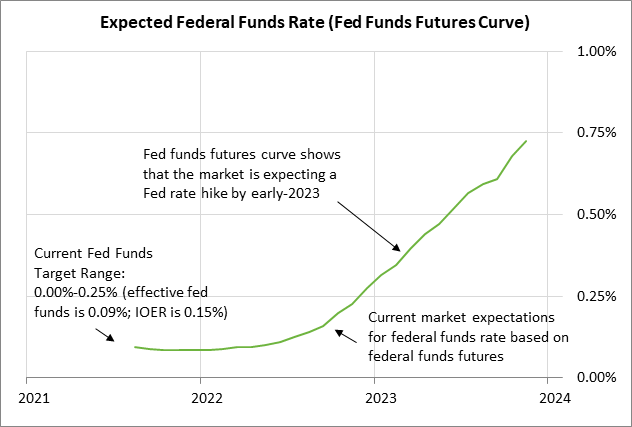

- Markets wait to see if Fed Chair Powell today will provide an early warning about QE tapering

- U.S. PCE deflator expected to remain very high

- U.S. consumer sentiment expected to remain weak despite small upward revision

Markets wait to see if Fed Chair Powell today will provide an early warning about QE tapering — The markets are on guard for the possibility that Fed Chair Powell today will deliver an explicit warning that QE tapering is near. Mr. Powell today will speak remotely at the Jackson Hole conference at 10 AM ET.

The Fed already delivered a tapering warning of sorts with last Wednesday’s release of the July 27-28 FOMC meeting minutes, which said that most participants “judged that it could be appropriate to start reducing the pace of asset purchases this year.”

However, there were “several” FOMC members who thought that QE tapering wouldn’t be appropriate until next year. Also, the macroeconomic situation since the July 27-28 FOMC meeting has deteriorated due to the pandemic’s resurgence, which means there might be less enthusiasm among FOMC members for near-term QE tapering.

The markets will therefore be waiting for Fed Chair Powell today to give the Fed’s latest guidance about the expected timing of QE tapering. The markets won’t be shocked if Mr. Powell delivers a clear early warning about QE tapering. However, there is likely to be some disappointment since a significant number of market participants seem to be hoping that Mr. Powell today will defer a warning and will continue his theme that it is still too early to taper QE due to uncertainties caused by the delta variant.

Despite such dovish hopes, the FOMC seems likely to officially announce QE tapering at its next meeting on September 21-22 or the following meeting on November 2-3. If Mr. Powell expects a QE tapering decision in less than four weeks at the September meeting, then he may want to give an explicit warning today, so the markets are not caught off-guard when that announcement is delivered. The Fed knows that it must clearly telegraph its intentions on QE tapering if it doesn’t want another taper tantrum, such as the one that occurred in 2013.

An obvious time for the Fed to actually start the QE tapering process would be January 1, 2022, thus allowing for adjustments to be based on calendar quarters. Some FOMC members have already said they want the QE tapering program to be finished by as soon as mid-2022.

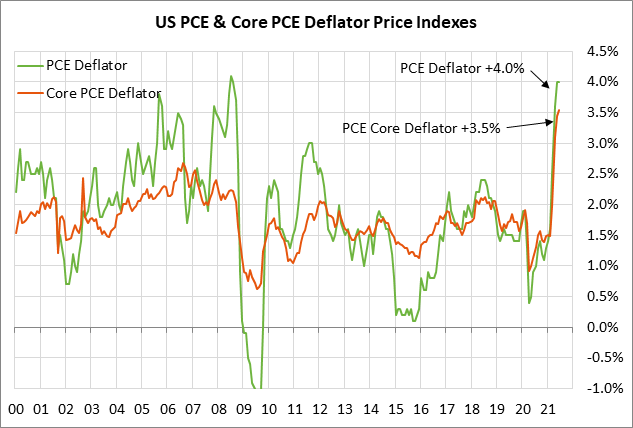

U.S. PCE deflator expected to remain very high — The consensus is for today’s July PCE deflator to show increases of +0.4% m/m and +4.1% y/y, which would be close to the June report of +0.5% m/m and +4.0% y/y.

Meanwhile, today’s July core PCE is expected to show increases of +0.3% m/m and +3.6% y/y, which would be close to June’s report of +0.4% m/m and +3.5% y/y.

U.S. inflation is extremely high at present but at least appears to be peaking. On a 3-month annualized basis, the headline CPI in July eased to +8.4% from June’s +9.7%, while the core CPI eased to +8.1% from June’s +10.6%. The PCE deflator on a 3-month annualized basis in June was up +6.6%, and the core deflator was up +6.7%.

The market continues to generally agree with the Fed that the current surge in inflation is transitory. The Fed points out that much of the strength in the inflation statistics is in sectors of the economy that have been squeezed by the economic reopening. The consensus is that inflation will ease later this year and into 2022 as supply shortages ease and as the U.S. economy decelerates to more normal growth rates.

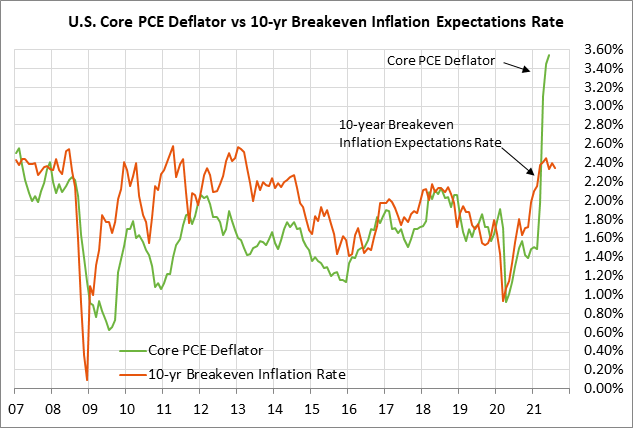

The market is discounting only a mildly elevated inflation rate looking forward. The 10-year breakeven inflation expectations rate is currently at 2.35%. That is well above the pre-pandemic level of 1.75%, but down from May’s 8-1/2 year high of 2.59%.

The markets so far believe that the Fed will not fall behind the inflation curve and will withdraw its stimulus in time to prevent any systemic surge in inflation. The general feeling seems to be that the global economy remains in the disinflationary conundrum that it was in before the pandemic and will return to that low-inflation environment once the pandemic is over.

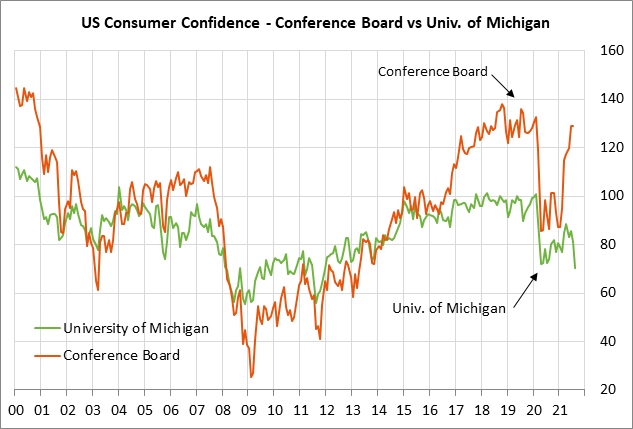

U.S. consumer sentiment expected to remain weak despite small upward revision — The consensus is for today’s final-Aug University of Michigan U.S consumer sentiment index to be revised higher by +0.6 to 70.8 after the sharp -11.0 point drop to 70.2 seen in the preliminary report for August.

The markets did not expect the plunge in the consumer sentiment index in early August to a new 9-3/4 year low, which took out even the previous pandemic low of 71.8 posted in April 2020. Consumers are clearly alarmed by the resurgence of the pandemic and the return of some pandemic restrictions. Consumers are also reacting negatively to the surge in inflation and high gasoline prices, which are taking a bite out of their wallets.

However, there is room for consumer sentiment to improve in coming months since the economic outlook is much better than it was last April. The Fed and the U.S. government have pumped the U.S. economy full with massive amounts of monetary and fiscal stimulus, and the U.S. economy is growing so fast that it has run into many supply obstacles. The resurgence of the pandemic is clearly a major disappointment, but as the vaccination levels continue to improve, the pandemic should still fade going into next year and allow a more normal economy and labor market to emerge.