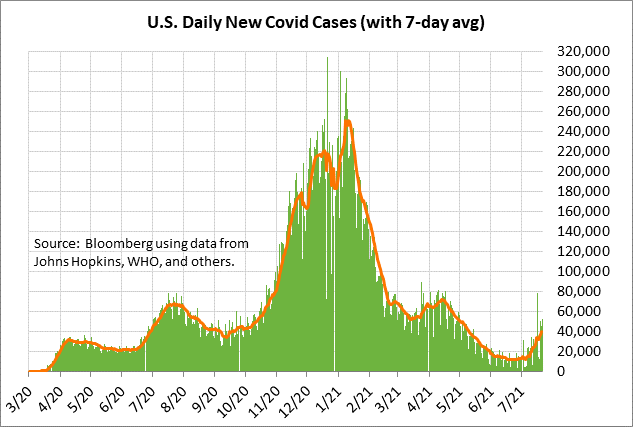

- Rising U.S. Covid infection rate sparks worries about slower economic growth

- Bipartisan infrastructure bill may get another vote next week

- FOMC’s consideration of QE tapering may be slowed by the Delta variant

Rising U.S. Covid infection rate sparks worries about slower economic growth — The U.S. Covid infection rate continues to rise and cause market worries about weaker U.S. economic growth. Most states seem unlikely to impose new restrictions. However, as reports emerge about the new pandemic risks, a larger number of people may scale back their traveling, visits to restaurants, and attendance at public events, thus undercutting economic growth.

The stock market has already displayed jitters in recent weeks from worries that the U.S. economy has already passed its peak. The markets were already expecting weaker economic growth as fiscal stimulus fades, but now the Delta variant is adding to those worries.

The consensus is for U.S. GDP growth to decelerate to +7.1% in Q3 and +5.1% in Q4 from the expected peak of +9.0% in Q2. For calendar-year 2021, GDP growth is expected to be very strong at +6.6%, but growth is then expected to decelerate to +4.2% in 2022 and a more normal +2.4% in 2023.

New Covid infections have been sweeping the country due to the spread of the more transmissible Delta variant. The CDC said earlier this week that the Delta variant accounts for 83% of new U.S. Covid infections. The Delta variant is spreading particularly fast in states that have low vaccination rates.

U.S. Covid infections have tripled in just the past month as the Delta variant sweeps the country. The 7-day average of new U.S. Covid infections on Wednesday rose to a new 2-1/2 month high of 40,062 cases, which is more than triple the 16-month low of 11,351 posted just a month ago on June 23.

The CDC reports that 48.8% of the U.S. population is now fully vaccinated, and 56.4% have received at least one dose. Bloomberg reports that the U.S. has administered an average of 532,836 doses per day, which is little changed from the past several weeks despite the new warnings about the Delta variant.

Bipartisan infrastructure bill may get another vote next week — The bipartisan group of Senators is reportedly close to reaching a final agreement on an infrastructure bill. They are hoping to complete the legislative text by Monday and also receive scoring from the CBO on the pay-fors. If a final agreement is reached with the support of at least 10 Republican Senators, then Senate Majority Leader Schumer has said that he will hold another cloture vote for bringing the bill to the Senate floor for debate. That cloture vote could happen early next week.

The bipartisan infrastructure bill has slowed the Democrats’ consideration of the $3.5 trillion budget resolution since Democrats are unsure whether they will need to cover the $579 billion of spending contained in the infrastructure bill. Also, Senate Budget Committee Chairman Bernie Sanders has to make sure he has all 50 Democratic Senators on board with the $3.5 trillion budget resolution since the resolution won’t pass if even one Democratic Senator is opposed.

Mr. Sanders has said he may not have the budget resolution ready for a vote until early August. The Senate is currently scheduled to leave for its summer recess on August 6 and not return until after Labor Day. Passage of the budget resolution will set the stage for a $3.5 trillion reconciliation bill that will be considered by the Senate this autumn.

FOMC’s consideration of QE tapering may be slowed by the Delta variant — The FOMC at its meeting next week on Tuesday and Wednesday is expected to continue the QE tapering discussion that began at its last meeting on June 15-16. However, the FOMC next week is not expected to announce that it is close to QE tapering. Instead, the FOMC is likely to stress that the conditions have not yet been met for QE tapering.

The FOMC next week may even sound a bit more dovish than its June meeting since U.S. Covid infections have more than tripled since the June meeting. The Delta variant is a worrisome development for the Fed since there is no way to tell when the current spike in new infections may end. The Fed is not likely to proceed with QE tapering until the Delta variant has been contained and infections are down to a relatively low level.

Prior to the Delta variant, the markets were generally expecting the Fed to give an early warning of QE tapering at either the August Jackson Hole conference or the September 21-22 FOMC meeting. However, the Delta variant may push that schedule back by at least 1-2 months, depending on the course of the pandemic.

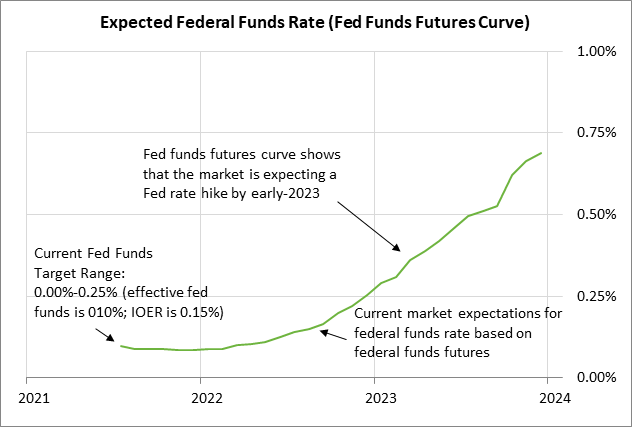

The markets in the past several weeks have significantly scaled back expectations for Fed tightening. The market is not expecting the Fed’s first +25 bp rate hike until 2023, which is about 1-1/2 years away. On a yield basis, the Dec 2023 federal funds futures contract in the past three weeks has eased by 14 bp to 0.66%, which means the market is discounting just 56 bp of tightening through the end of 2023 from the current effective federal funds rate of 0.10%.