- U.S. deflator expected to remain strong

- U.S. personal income and spending expected mixed

- Final-Oct U.S. consumer sentiment expected unchanged

- U.S. employment cost index expected to strengthen

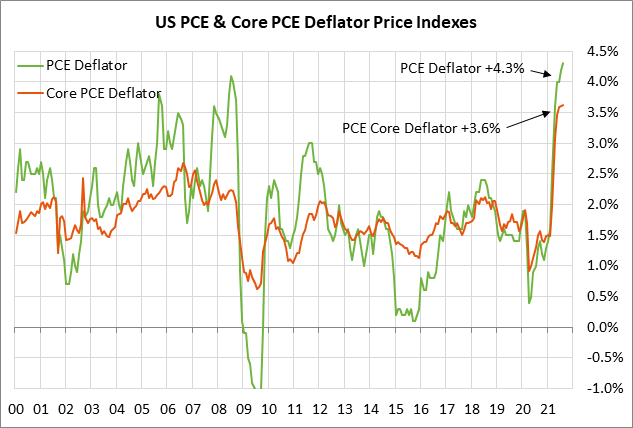

U.S. deflator expected to remain strong — Today’s PCE deflator, which is the Fed’s preferred inflation measure, is expected to show continued strength and is likely to cause the markets to remain concerned about the inflation outlook.

Fed Chair Powell last Friday said that supply-chain constraints, which have led to elevated inflation, “are likely to last longer than previously expected, likely well into next year.” However, he added that “it is still the most likely case” that as those constraints ease, as they eventually will — and as job gains move up — inflation will move back down closer to our 2% goal.”

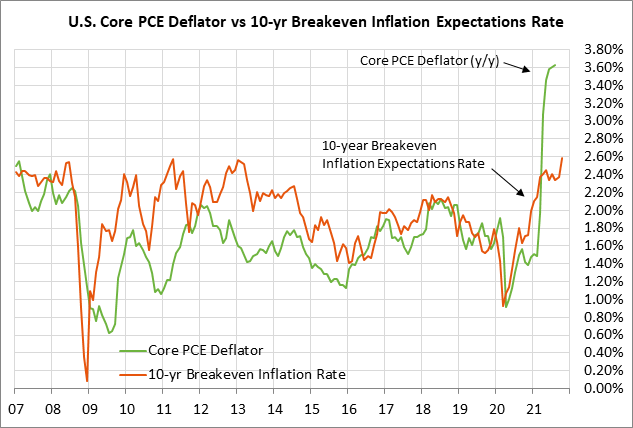

While the Fed continues to insist that the inflation surge will be temporary, the markets have pushed the 10-year breakeven inflation expectations rate sharply higher in the past several weeks. The breakeven rate on Wednesday rose to a new 9-year high of 2.70%, although it then fell sharply on Thursday to 2.59%.

The consensus is for today’s Sep PCE deflator to show an increase of +0.3% m/m and +4.4% y/y, following the August report of +0.4% m/m and +4.3% y/y. Today’s Sep core PCE deflator is expected to show an increase of +0.2% m/m and +3.7% y/y, following the August report of +0.3% m/m and +3.6% y/y.

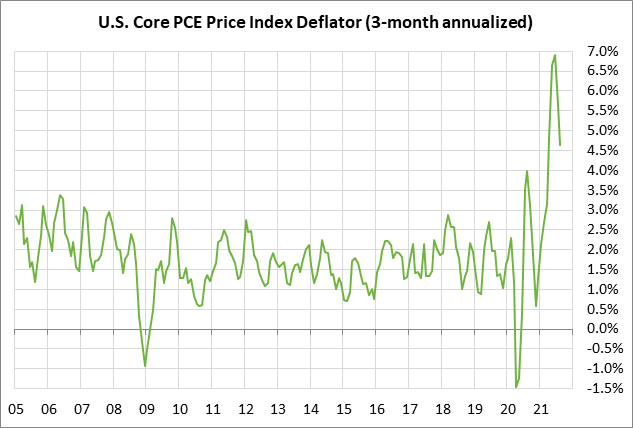

The year-on-year inflation figures continue to be distorted by last year’s very low base due to the pandemic economic shutdowns, which means the markets are focusing mainly on the shorter-term inflation measures. In that regard, there is some good news as the deflator eases on a 3-month annualized basis.

On a 3-month annualized basis, the headline deflator eased to +5.5% in August from the peak of +6.9% seen in May. Meanwhile, the core deflator in August eased to +4.6% from the peak of +6.90% seen in June. Still, those are high inflation figures that raise concern about whether inflation next year will in fact ease back to the Fed’s target of +2%.

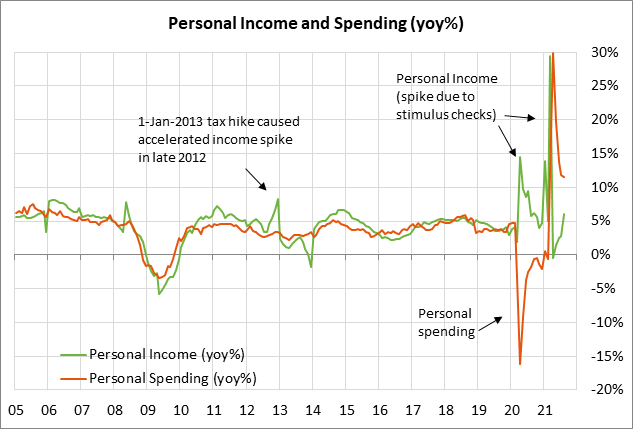

U.S. personal income and spending expected mixed — The consensus is for today’s Sep personal income report to show a decline of -0.2% m/m, reversing Aug’s rise of +0.2% m/m. U.S. personal income was undercut in recent months as stimulus checks ran out, but income remains strong as wages rise and as the total level of U.S. employment continues to rise.

Today’s Sep personal spending report is expected to show another strong increase of +0.6% m/m, adding to August’s gain of +0.8% m/m. Consumers continue to engage in fairly active spending activity on pent-up demand as the pandemic ebbs.

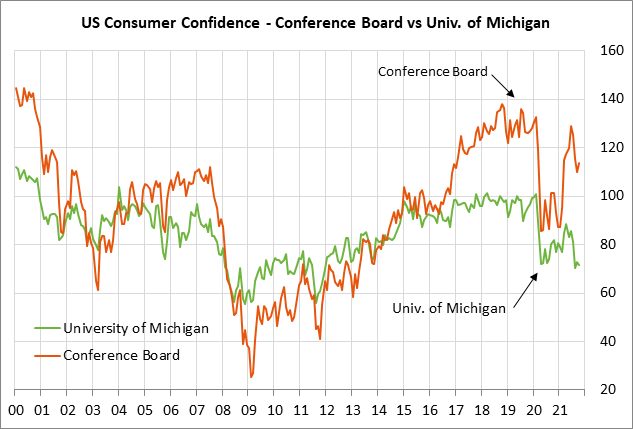

Final-Oct U.S. consumer sentiment expected unchanged — Today’s final-Oct University of Michigan U.S. consumer sentiment index is expected to be unrevised from the early-Oct report of 71.4.

The U.S. consumer sentiment index in August plunged by -10.9 points to a 10-year low of 70.3 as the pandemic surged. Consumer sentiment in August was even lower than the worst level of 71.8 seen in April 2020 during the depths of the economic shutdowns in spring 2020. Consumers this past July and August were unsure about how bad the pandemic’s resurgence might get and whether there might be new shutdowns in the U.S. economy.

Consumer sentiment then showed a +2.5 point upward rebound in September, but lost ground again by -1.4 points in early October. Consumers through October continued to be worried about the fall-out from the pandemic’s resurgence, even though Covid infections fell sharply through October.

U.S. consumer sentiment has also been hurt by the surge in gasoline prices, which is taking a bite out of consumer pocketbooks. Consumers are also being hurt by inflation and the general rise in the price of many products and services, which is reducing their purchasing power.

Looking ahead, however, consumer confidence should see some underlying support starting in November due to the sharp drop in U.S. Covid infections that began in mid-September. The sharp drop in Covid infections will make more people more willing to go out to shop, go to restaurants, attend entertainment events, and travel.

Also, consumers should feel better due to sharp rise in home and stock prices, which has substantially boosted household wealth. In addition, wages are rising and jobs are plentiful. All in all, the picture looks favorable for consumers over the next few quarters.

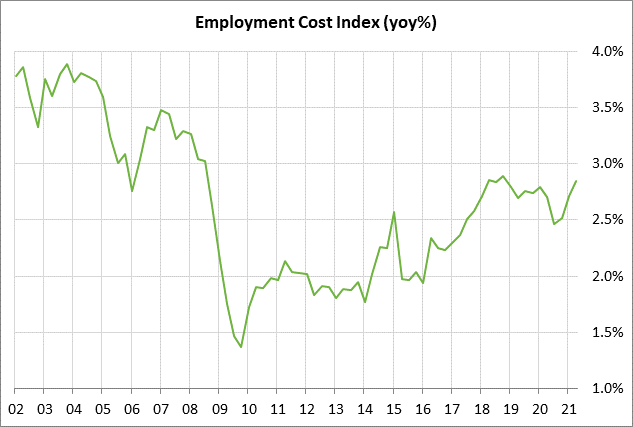

U.S. employment cost index expected to strengthen — Today’s Q3 employment cost index is expected to show an increase of +0.9% q/q, strengthening from the Q2 report of +0.7% q/q. The ECI is the broadest measure of employment costs.

The ECI has strengthened this year, rising to a 2-1/2 year high of +2.8% y/y in June, which was just below the 13-year high of +2.9% posted in 2018. Wages and salaries are currently on the upswing as businesses have trouble finding qualified employees and as many employees are quitting their jobs for greener pastures, forcing employers to raise wages and salaries.