- T-note meltdown shakes stock market

- House set to approve $1.9 trillion pandemic aid package today

- Final-Feb U.S. consumer sentiment expected to be revised slightly higher

- U.S. PCE deflator expected stable despite high inflation expectations

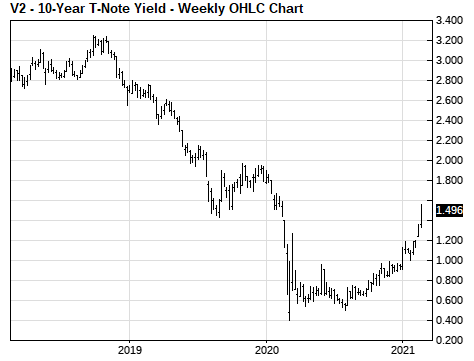

T-note meltdown shakes stock market — The U.S. stock market finally reacted to the recent surge in T-note yields after the March 10-year T-note futures contract on Thursday plunged by about 1-1/2 points to a 1-year nearest-futures low. The 10-year T-note yield on Thursday soared to a new 1-year high of 1.61% and closed the day up +14 bp at 1.52%. The T-note yield has now soared by +20 bp this week and by an overall +63 bp this year. The 10-year T-note yield is now only 40 bp below the pre-pandemic level of 1.92% seen at the end of 2019.

Stocks fell sharply on Thursday with a -2.45% sell-off in the S&P 500 and a -3.56% sell-off in the Nasdaq 100 index.

The Treasury market on Thursday gave up hope of a Fed rescue and capitulated after two Fed officials reinforced Fed Chair Powell’s comment on Tuesday that the Fed views the surge in yields as a good sign that the markets are now expecting a full economic recovery.

Even after two days of sharp T-note price losses on Tuesday and Wednesday, two Fed officials on Thursday piled on. Kansas City Fed President George said, “the notable rise in longer-term interest rates does not warrant a monetary response.” St. Louis Fed President Bostic said the recent rise in yields is “probably a good sign” as it reflects a better U.S. economic growth outlook.

European officials, by contrast, are trying to prevent European bond yields from rising. ECB chief economist Lane on Thursday said ECB officials are “closely monitoring the evolution of longer-term nominal bond yields and will buy bonds flexibly to prevent undue tightening that is inconsistent with countering the downward impact of the pandemic on the projected path of inflation.”

Global bond yields rose sharply yesterday in sympathy with the U.S. T-note market. The 10-year German bund yield climbed to an 11-month high of -0.22%, and the 10-year UK gilt yield rose to a new 11-month high of 0.83%. Japan’s JGB 10-year yield jumped to a 2-1/4 year high of 0.15%.

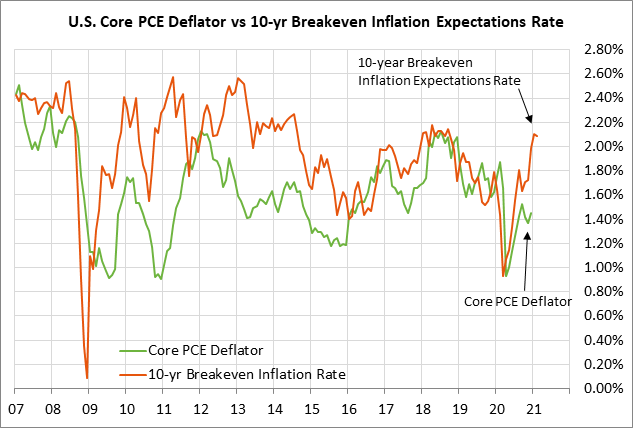

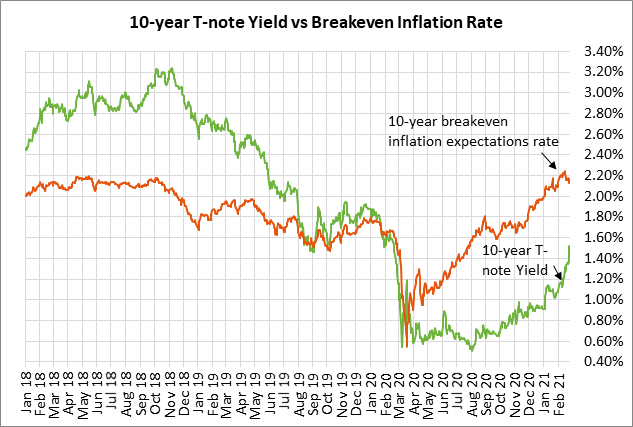

The sharp rise in T-note yields seen since late 2020 has been due to (1) the emergence of effective Covid vaccines that could end the pandemic by the end of 2021, (2) the massive amount of stimulus passed by Congress, with more on the way, and (3) the sharp rise in inflation expectations. The 10-year breakeven inflation expectations rate is currently at 2.10%, which is just 16 bp below the mid-Feb 6-1/2 year high of 2.26%. The breakeven rate is currently +31 bp higher than even the pre-pandemic level of 1.79%.

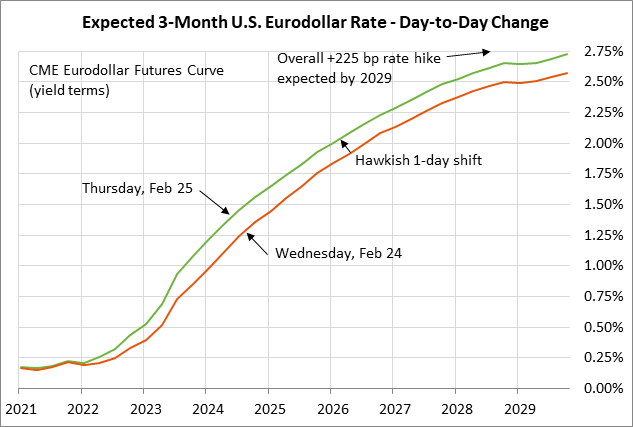

Yesterday’s surge in interest rates was not isolated to the long-end of the yield curve. Indeed, the Eurodollar futures on a yield basis rose sharply yesterday by as much as 15-20 bp as the market discounted a quicker return to a normal economy and thus an earlier-than-expected Fed rate hike.

The markets are now expecting the Fed’s first +25 bp rate hike in about 1-1/2 years in late-2022, versus previous expectations for a rate hike by early-2023. The markets are now expecting an overall rate hike of about +250 bp by 2029, which is about 20 bp more than the +230 bp rate hike expected earlier this week.

House set to approve $1.9 trillion pandemic aid package today — The House today is expected to approve President Biden’s $1.9 trillion pandemic aid bill. The Senate will then consider the bill, and will likely make some changes that would require the House to pass the revised version. Democratic leaders have promised to get the bill passed before unemployment benefits start running out on March 14.

The pandemic aid bill still needs some adjustment because it currently exceeds $1.9 trillion, in violation of the Senate’s budget reconciliation rules. In addition, the Senate parliamentarian last night ruled that the minimum wage hike to $15 per hour cannot be in the bill. However, the final bill end is still likely to be near $1.9 trillion and will provide substantial additional stimulus to the economy in the coming months.

Final-Feb U.S. consumer sentiment expected to be revised slightly higher — The consensus is for today’s final-Feb University of Michigan U.S. consumer sentiment index to be revised slightly higher by +0.3 points to 76.5, leaving the index down by -2.5 points from January rather than the preliminary decline of -2.8 points.

The consumer sentiment index showed back-to-back declines in Jan-Feb as the pandemic peak in January took its toll. However, consumer sentiment should improve substantially in March due to the plunge in Covid cases and hopes that the growing availability of vaccinations will end the pandemic by the end of this year.

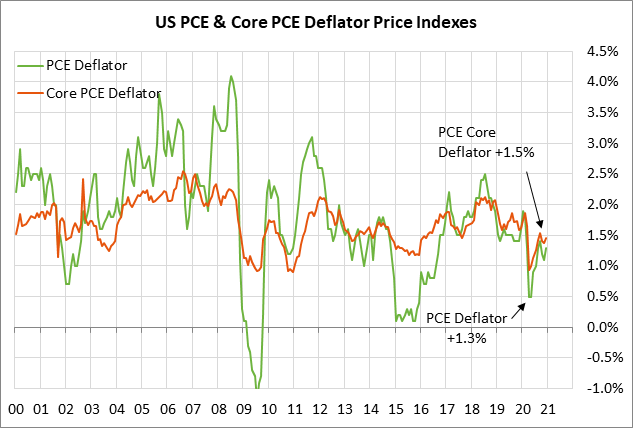

U.S. PCE deflator expected stable despite high inflation expectations — The consensus is for today’s Jan PCE deflator to rise slightly to +1.4% y/y from December’s +1.3% y/y. However, the Jan PCE core deflator is expected to ease slightly to +1.4% y/y from December’s +1.5% y/y.

The headline and core PCE deflators are currently well below the Fed’s +2.0% inflation target. However, the inflation statistics on a year-on-year basis are expected to be elevated in the next several months because of the low year-earlier base during the worst of the pandemic shutdowns. The markets will therefore be looking more closely at the 3-month annualized inflation figures than at the year-on-year figures over the next few months. The Fed, in any case, is actively pushing for an above-2% inflation rate, which means the markets won’t be too worried about a near-term rise in inflation.