- Fed’s Beige Book to give update on pandemic resurgence and supply chain disruptions

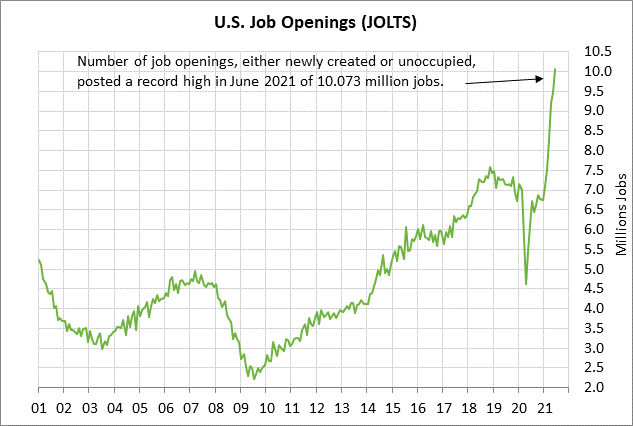

- U.S. JOLTS job openings expected to post new record high

- 10-year T-note auction

Fed’s Beige Book to give update on pandemic resurgence and supply chain disruptions — The Fed today will release its Beige Book survey of the regional U.S. economies.

In the last Beige Book released on July 14, the survey concluded that, “The U.S. economy strengthened further from late May to early July, displaying moderate to robust growth. Sectors reporting above-average growth included transportation, travel and tourism, manufacturing, and nonfinancial services. Energy markets improved slightly, and agriculture had mixed results. Supply-side disruptions became more widespread, including shortages of materials and labor, delivery delays, and low inventories of many consumer goods.”

The markets today will be scouring the Beige Book to gauge the impact from the pandemic’s resurgence. The markets will also be waiting for the Fed’s latest information about the extent to which bottlenecks continue to plague the supply chain and constrain economic growth.

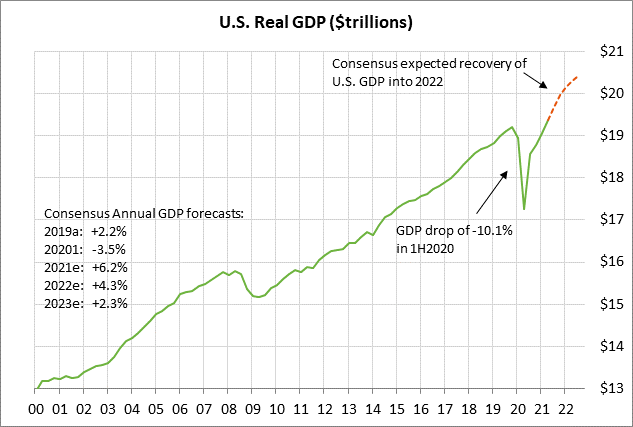

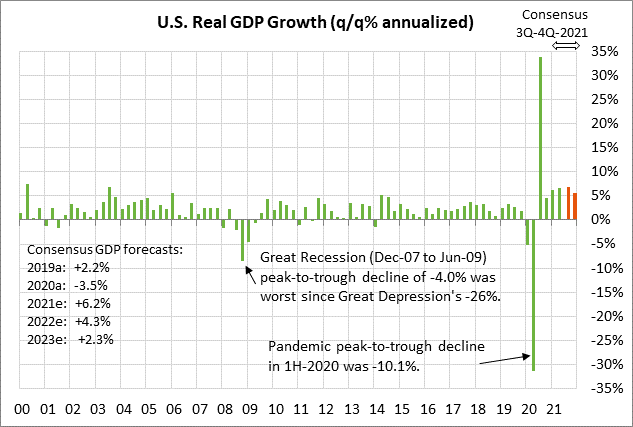

The consensus is that U.S. GDP growth is peaking in the current 3rd-quarter at +6.9% (q/q annualized) and will then start sliding back to more normal growth rates as stimulus wears off and pent-up demand is satisfied. The consensus is for U.S. GDP growth to ease to +5.6% in Q4, +3.8% in Q1-2022, and +3.0% in Q2-2022.

On a calendar year basis, the consensus is for U.S. GDP growth to peak this year at +6.2%, easily overcoming the -3.5% decline seen in 2020 and posting the strongest growth rate in 37 years, i.e., since 1984. GDP growth is then expected to ease to +4.1% in 2022 and +2.3% in 2023.

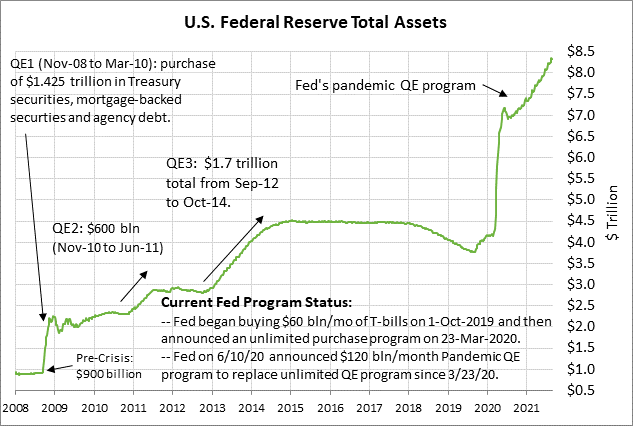

Today’s Beige Book is being released ahead of the FOMC meeting in two weeks on Sep 21-22. The markets are on guard for the possibility that the FOMC at that meeting might formally announce that it will begin QE tapering later this year, or on January 1, 2022.

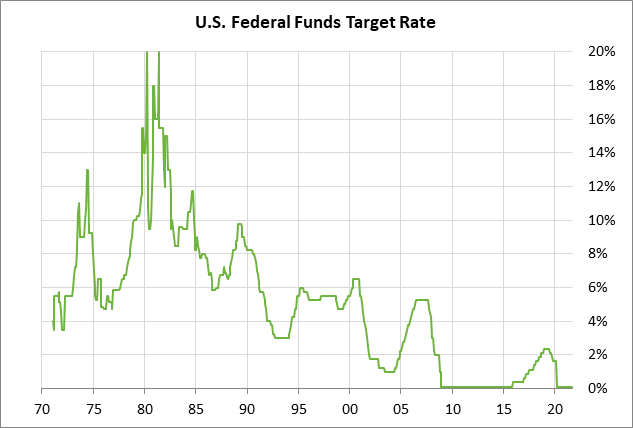

The Fed at its upcoming September meeting will release new economic projections and a new set of Fed-dot forecasts for the funds rate. The last set of Fed dots, released after the June 15-16 FOMC meeting, showed that FOMC members were expecting rate hikes sooner than they were in the previous dot-plot from March. The June dot-plot showed that 11 of 18 FOMC officials saw two rate hikes by the end of 2023, up from only 5 members in March who were expecting at least two rate hikes. Moreover, 7 of 18 members saw a rate hike as early as 2022, up from only 4 in March.

Fed Chair Powell, in June’s post-meeting press conference, tried to downplay the importance of the dot-plot, but the fact remains that the dot-plot showed that individual FOMC members turned significantly more hawkish. Mr Powell said, “The dots are not a great forecaster of future rate moves. These are of course individual projections, they’re not a committee forecast, they’re not a plan. And we did not actually have a discussion of whether liftoff is appropriate in any particular year, because discussing liftoff now would be highly premature — it wouldn’t make any sense.”

U.S. JOLTS job openings expected to post new record high — The consensus is for today’s July JOLTS job openings to show an increase of +25,000 to 10.098 million. The JOLTS job openings series in June soared by +590,000 to a record high of 10.073 million (data from 2000).

U.S. businesses are advertising for a record number of job openings as the economy reopens from the pandemic and as businesses struggle to replace workers. There are widespread reports of labor shortages in some industries where some workers have shifted job specialties or are seeking higher wages to take back their previous jobs.

However, businesses may be getting a little more cautious about hiring due to the pandemic’s resurgence and the increase in pandemic restrictions. It would not be surprising to see job openings start to fall back to more normal levels as more people get hired and as the economy downshifts to more normal growth rates.

10-year T-note auction — The Treasury today will sell $38 billion of 10-year T-notes in the first of two reopenings of the 1-1/4% 10-year T-note of August 2021 that the Treasury first sold last month. The Treasury will conclude this week’s coupon package by selling $24 billion of 30-year T-bonds on Thursday.

The 12-auction averages for the 10-year are as follows: 2.42 bid cover ratio, $17 million in non-competitive bids, 5.0 bp tail to the median yield, 68.4 bp tail to the low yield, and 51% taken at the high yield. The 10-year is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.2% of the last twelve 10-year T-note auctions, which exactly matches the median for all recent Treasury coupon auctions.