- Fed Chair Powell not expected to spring any surprises in today’s testimony

- U.S. PPI expected to surge

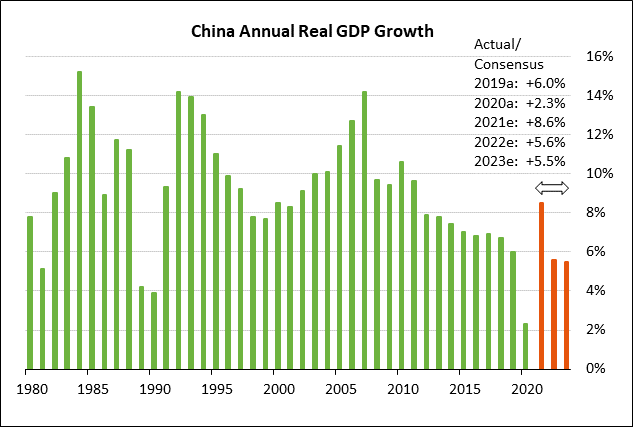

- China GDP expected to be weak

Fed Chair Powell not expected to spring any surprises in today’s testimony — Fed Chair Powell today will appear before the House Financial Services Committee to deliver the Fed’s semi-annual monetary policy report to Congress. Mr. Powell will appear tomorrow before the Senate Banking Committee for the second day of his testimony.

Mr. Powell today is expected to reiterate the Fed’s recent themes and is not expected to spring any surprises on the markets. The Fed is still in the phase of trying not to rock the boat and cause any surge in interest rates that could threaten the recovery.

Regarding QE tapering, Mr. Powell is likely to reiterate his recent theme that even though the Fed started discussing when to taper QE, it is too early for a tapering decision because not enough progress has been made on the Fed’s employment goals.

The minutes from the June 16-17 FOMC meeting made that point by saying, “The committee’s standard of ‘substantial further progress’ was generally seen as not having yet been met, though participants expected progress to continue.” However, the minutes also said that “Various participants mentioned that they expected the conditions for beginning to reduce the pace of asset purchases to be met somewhat earlier than they had anticipated at previous meetings.”

A survey taken by Bloomberg in June showed a consensus that the Fed’s early warning of QE tapering will come at either the August Jackson Hole conference or the following FOMC meeting on September 21-22. That survey showed that 33% of the respondents then expect the formal announcement of QE tapering in September, 10% in October or November, and 33% in December.

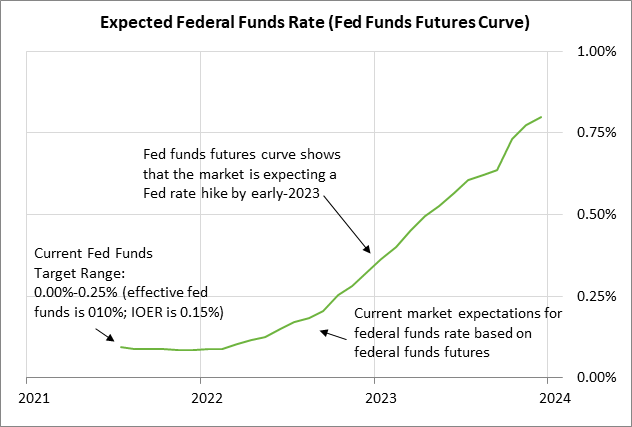

While QE tapering is on the horizon, the market believes that the Fed’s first +25 bp rate hike is more than a year away in early 2023, according to the federal funds futures market. The market is expecting a total of two rate hikes in 2023.

Meanwhile, FOMC members have turned more hawkish about rate hikes. The new FOMC dot-plot from the June 16-17 meeting showed that 7 of the 18 FOMC members are now expecting at least one +25 bp rate hike in 2022, and 11 of the 18 members are expecting a total of at least two rate hikes by the end of 2023.

Mr. Powell today is also likely to reiterate the Fed’s view that the current inflation surge is transitory. The Fed in the minutes from its last meeting on June 16-17 called the inflation surge “transitory.” Mr. Powell also said after the meeting that the Fed expects inflation to moderate over time as supply bottlenecks abate. He said, “Our expectation is that these high inflation readings that we’re seeing now will start to abate.”

However, Mr. Powell also said that if inflation or expectations jump “materially above what we would see as consistent with our goals, and persistently so, we wouldn’t hesitate to use our tools to address that.†The bond market was certainly happy to hear that the Fed would act on inflation if that became necessary. The Fed’s inflation resolve is currently in question since that the Fed is explicitly planning to allow inflation to temporarily rise above its 2% target to ensure that its 2% average target is met over time.

Meanwhile, the Fed today will release its Beige Book survey of the U.S. economy. The markets will watch today’s report to gauge the strength of the economy as well as the extent of bottlenecks and price surges. The last Beige Book report, released on June 2, said, ” The national economy expanded at a moderate pace from early April to late May, a somewhat faster rate than the prior reporting period. Several Districts cited the positive effects on the economy of increased vaccination rates and relaxed social distancing measures, while they also noted the adverse impacts of supply chain disruptions.”

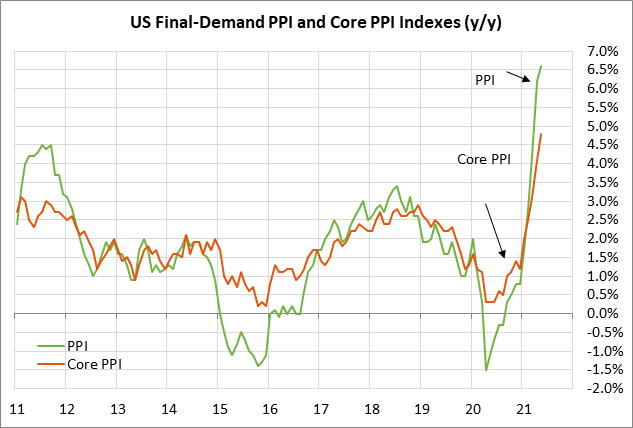

U.S. PPI expected to surge — The consensus is for today’s June final-demand PPI to show an increase of +0.6% m/m and +6.8% y/y, which would be fairly close to May’s report of +0.8% and +6.6%, respectively. The June core PPI is expected to show smaller increases of +0.5% m/m and +5.1% y/y after May’s report of +0.7% and +4.8%, respectively.

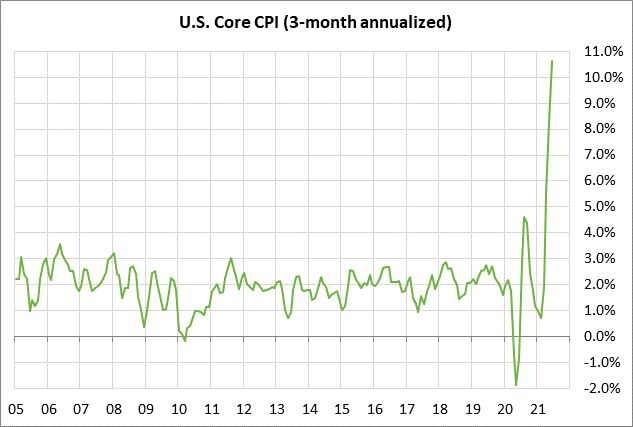

Yesterday’s June CPI report of +0.9% for both the headline and core reports was substantially stronger than expectations of +0.5% for the headline figure and +0.4% for the core figure. On a year-on-year basis, the June headline CPI was up +5.4% and the core CPI was up +4.5%. On a 3-month annualized basis, the June CPI was up by an extraordinary +9.7% and the core CPI was even worse at +10.6%.

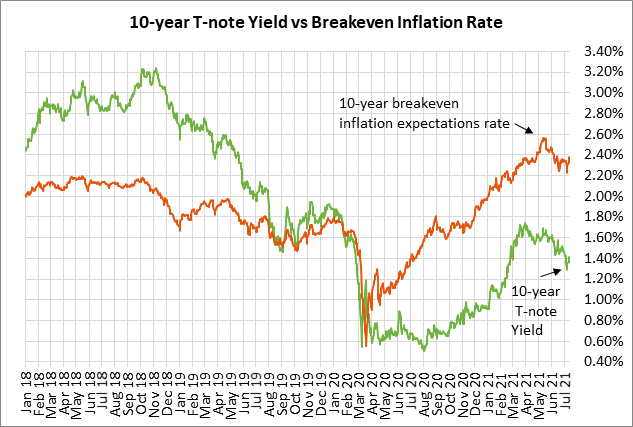

Yesterday’s CPI surge caused the 10-year breakeven inflation expectations rate to rise by +4 bp to 2.38%, posting a new 1-month high and bringing the 3-session surge to a total of +14 bp. However, the breakeven rate is still 21 bp below May’s 8-1/4 year high of 2.59%.

There were some signs that the CPI surge is partly transitory since about half of the CPI increase was tied to pandemic reopening categories, according to analysis by Bloomberg.

China GDP expected to be weak — The consensus is for today’s China Q2 GDP report to show an increase of only +1.0% q/q, which would be a bit better than Q1’s increase of +0.6% q/q but would translate to an annualized figure of only +4.0%, a paltry growth rate for China. There is some concern that today’s Chinese GDP report might be worse than expected since the Chinese government late last Friday unexpectedly eased monetary policy by cutting the bank reserve requirement ratio by -0.50 bp, which freed up about $154 billion in bank liquidity.