- T-note yields continue to rise as Powell testifies today

- Senate Republicans block CR/debt ceiling hike as expected, while Pelosi delays House infrastructure vote until Thursday

- U.S. consumer confidence expected to show a small recovery

- U.S. home prices expected to show another sharp increase

- 7-year T-note auction

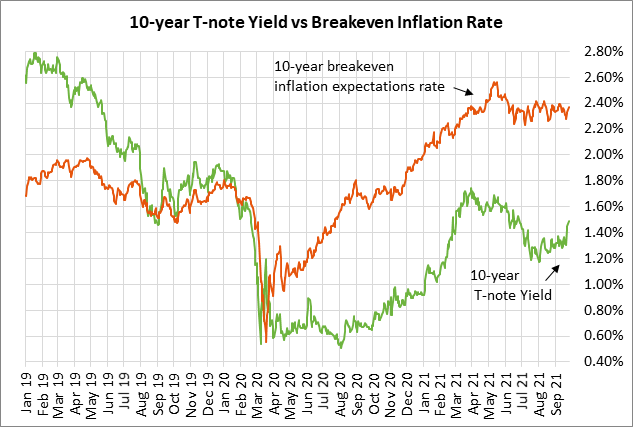

T-note yields continue to rise as Powell testifies today — Fed Chair Powell and Treasury Secretary Yellen will appear today before the Senate Banking Committee regarding the CARES Act and the response of the Fed and the Treasury to the pandemic.

The markets will be watching for the unlikely possibility that Mr. Powell tries to walk back the hawkish outcome of last week’s FOMC meeting. Treasury yields have surged since last week’s FOMC meeting. The 10-year T-note yield on Monday rose to a 3-month high and closed the day +4 bp at 1.49%, up +19 bp since last week’s FOMC meeting. The Dec 2023 federal funds futures contract (on a yield basis) has risen sharply by +13 bp since last week’s FOMC meeting to Monday’s 2-1/2 month high of 0.775%, reflecting market expectations for an overall 70 bp rate hike by the end of 2023 from the current effective funds rate of 0.08%.

Nevertheless, the Fed isn’t likely to be alarmed by the surge in Treasury yields. As with other recent interest rate surges, the Fed is likely to take the latest surge in stride as the predictable result of a slow return to a more normal economy and interest rate environment.

The FOMC last week made clear that QE tapering is likely to be officially announced at the next FOMC meeting on November 1-2. Also, FOMC members became more hawkish on their dot-plot forecasts, with half of the FOMC members now forecasting at least one rate hike by the end of 2022. The dot-plot indicated a median forecast that the Fed will raise its funds rate to 1.0% by the end of 2023.

Senate Republicans block CR/debt ceiling hike as expected, while Pelosi delays House infrastructure vote until Thursday — The Senate on Monday failed to pass a procedural motion to proceed with the combined CR and debt ceiling suspension bill that the House passed last week. The measure failed due to the expected filibuster by the Republicans. It is now up to Democrats to determine whether they are willing to strip out the debt ceiling suspension and just pass a clean CR, which would avert a government shutdown on Friday. Democrats must also figure out how to raise or suspend the debt ceiling before the Treasury’s X-date, which falls somewhere between October 15 and November 4 according to the Bipartisan Policy Center.

Meanwhile, House Speaker Pelosi delayed a vote until Thursday from Monday on the $550 billion infrastructure bill. She said she never brings bills to the floor that won’t pass. Progressive House Democrats are refusing to support the infrastructure bill until the $3.5 trillion reconciliation package is finished. Democrats are furiously trying to come up with a reconciliation package that both House and Senate Democrats can pass. Ms. Pelosi said it is self-evident that the size of the package is going to be smaller than $3.5 trillion.

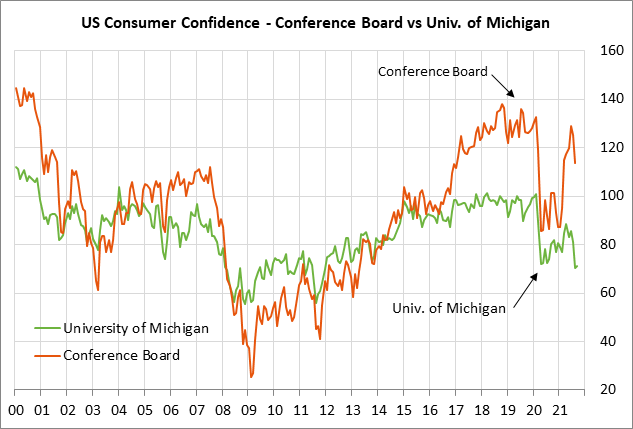

U.S. consumer confidence expected to show a small recovery — The consensus is for today’s Conference Board U.S. Sep consumer confidence index to show a small recovery of +1.2 points to 115.0, following August’s -11.3 point plunge to a 6-month low of 113.8.

U.S. consumer confidence fell sharply in August due to the surge in Covid infection rates and the increase in pandemic restrictions. Also, the labor market weakened in August, as seen by the fact that payrolls rose by only +235,000, far below expectations of +620,000. Consumers are also on the defensive due to inflation and the high price of gasoline.

However, consumers may be overly pessimistic given that the Covid infection rates have dropped over the past week. The 7-day average of new daily U.S. Covid infections on Sunday fell to a new 1-1/2 month low of 120,560.

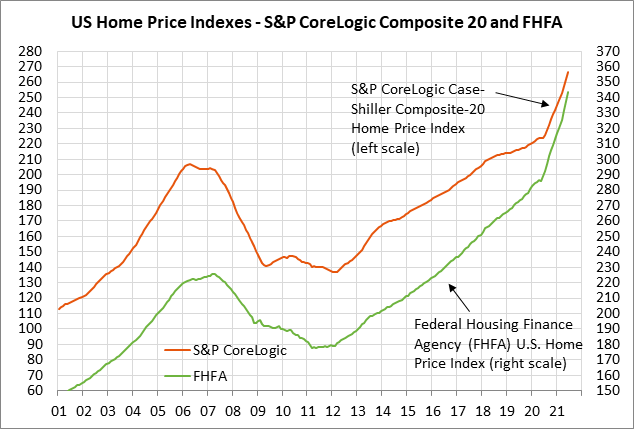

U.S. home prices expected to show another sharp increase — U.S. July home prices are expected to show a continued surge. The consensus is for the July FHFA house price index to rise sharply by +1.5% m/m, adding to June’s rise of +1.6% m/m. The consensus is for today’s July S&P CoreLogic composite-20 home price index to show rises of +1.7% m/m and +20.0% y/y, close to June’s report of +1.8% m/m and +19.1% y/y.

Relative to the pre-pandemic levels, the FHFA index is up by +22% and the Composite-20 index is up by +19%. Home prices have surged during the pandemic due to both strong demand and tight supplies.

U.S. existing home are down from the spike up to a 15-year high seen in October 2020, but are still higher than before the pandemic. Meanwhile, the supply of homes on the market remains very tight at 2.6 months, well below the 4-decade average of 6.6 months.

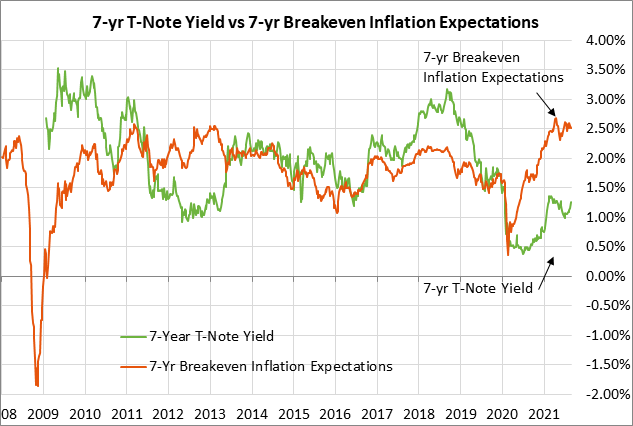

7-year T-note auction — The Treasury today will sell $62 billion of 7-year T-notes. The benchmark 7-year T-note yield yesterday posted a new 3-1/2 month high of 1.31% and closed the day +4 bp at 1.30%. The markets are nervous about today’s auction since the 7-year T-note auction over the past year has periodically seen some very disappointing results.

The 12-auction averages for the 7-year are: 2.30 bid cover ratio, $15 million in non-competitive bids, 6.0 bp tail to the median yield, 51.8 bp tail to the low yield, and 40% taken at the high yield. The 7-year T-note is the third least popular security among foreign investors and central banks, behind the 3-year and 2-year T-notes. Indirect bidders, a proxy for foreign buyers, have taken an average of 58.8% of the last twelve 7-year T-note auctions, which is well below the median of 62.4% for all recent Treasury coupon auctions.