- U.S. deflator expected to remain high in August

- Final-Sep U.S. consumer sentiment index expected unrevised

- U.S. ISM manufacturing index expected to show another decline but remain generally strong

U.S. deflator expected to remain high in August — Today’s PCE deflator, which is the Fed’s preferred inflation measure, is expected to show that inflation remained high in August. The Fed continues to insist that the current inflation surge is transitory. However, it appears that the transitory effects are going to extend well into next year.

Inflation is currently being pushed higher by a variety of factors, including (1) supply chain shortages and disruptions, (2) high shipping costs, (3) high fuel costs, including both petroleum products and natural gas, (4) labor market shortages, and (5) tight supply of a variety of products and services due to the surge in the economy.

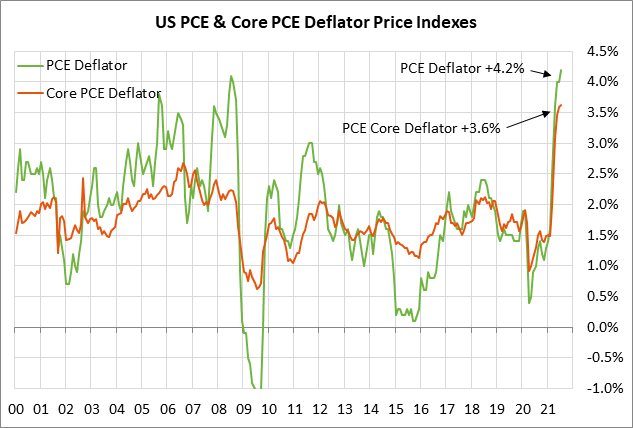

The consensus is for today’s Aug PCE deflator to show an increase of +0.3% m/m and +4.2% y/y, which would be close to July’s report of +0.4% m/m and +4.2% y/y. Meanwhile, today’s Aug PCE core deflator is expected to show an increase of +0.2% m/m and +3.5% y/y, close to July’s report of +0.3% m/m and +3.6% y/y.

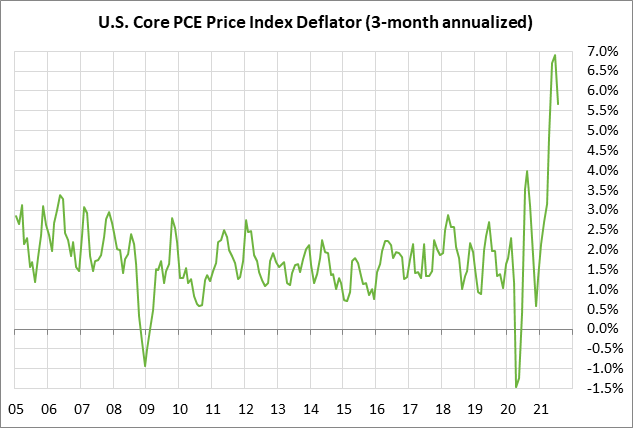

The headline deflator in July reached a 30-year high of +4.2% y/y, while the core deflator in June-July reached a 29-year high of +3.6% y/y. While the year-on-year figures are high, the 3-month annualized figures are even worse. On a 3-month annualized basis, the July deflator rose by +6.1% and the core deflator rose by +5.7%. Those figures were at least below the peaks of +6.9% seen for the headline deflator in May and for the core deflator in June.

There was some good news in the CPI data for August that has already been released. The headline CPI rose by only +0.3% m/m, and the core CPI rose by only +0.1% m/m. However, the CPI on a 3-month annualized basis in August was still up by +6.8% for the headline figure and +5.4% for the core figure.

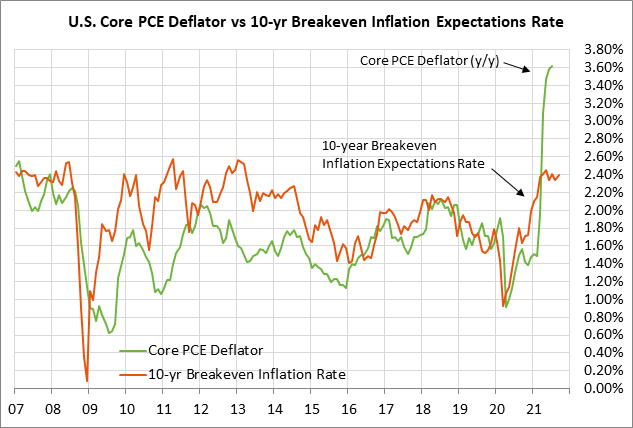

The markets continue to be relatively sanguine about the inflation outlook and expect the inflation statistics to ease next year as reopening effects abate and as companies catch up on boosting supply. The 10-year breakeven inflation expectations rate, which measures the difference between the 10-year nominal and TIPS yields, is currently near 2.38%, which is within the relatively narrow range seen over the past three months.

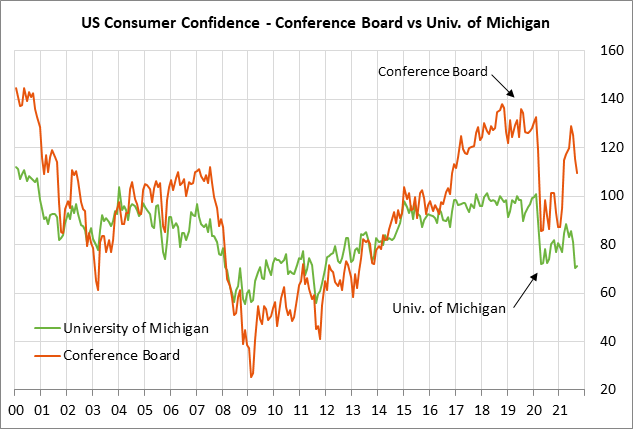

Final-Sep U.S. consumer sentiment index expected unrevised — Today’s final-Sep University of Michigan U.S. Sep consumer sentiment index is expected to be unchanged from the early-Sep level of 71.0, which would leave the index up by +0.7 points from August.

The consumer sentiment index in early September rebounded higher by only +0.7 points after the index in August plunged by -10.9 points to a 10-year low of 70.3. The index in August fell below even the worst level seen in April 2020 during the pandemic economic shutdowns.

U.S. consumer confidence fell sharply in August due to the surge in Covid infection rates and the increase in pandemic restrictions. Also, the labor market weakened in August, as seen by the fact that payrolls rose by only +235,000, far below expectations of +620,000. Consumers are also on the defensive due to inflation and the high price of gasoline.

However, consumers may be overly pessimistic given that the Covid infection rates have recently dropped. The 7-day average of new daily U.S. Covid infections this week has dropped to a 1-1/2 month low.

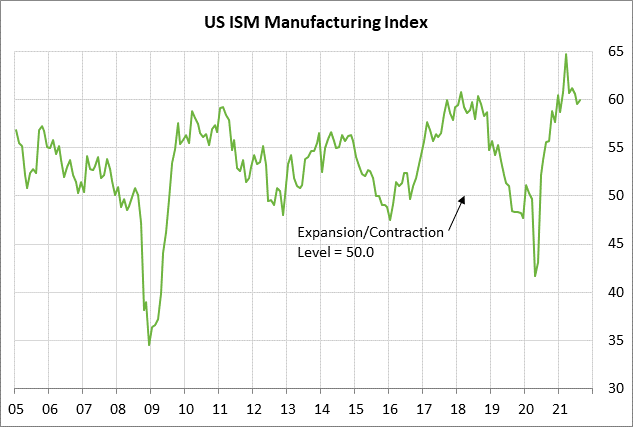

U.S. ISM manufacturing index expected to show another decline but remain generally strong — The consensus is for today’s Sep ISM manufacturing index to show a -0.4 point decline to 59.5, exactly reversing August’s +0.4 point increase to 59.9.

The ISM index has faded from March’s 37-year high of 64.7, but August’s report of 59.9 was still a strong level that indicates manufacturing executives remain very confident about the U.S. manufacturing sector. In addition, the Aug new orders sub-index remained very strong at 66.7, which indicated that there is a strong pipeline of orders ready to be filled.

While the manufacturing sector is seeing a huge influx of orders, the sector has also been hobbled by a variety of obstacles, including tight component and chip supplies, shipment disruptions, and high input prices. However, these obstacles should slowly abate in coming months as companies catch up on their orders and increase supply. In addition, U.S. GDP growth is expected to fall back to earth in coming quarters, thus easing the supply squeeze.

Markit today will revised its September U.S. manufacturing PMI. The Markit U.S. manufacturing PMI in early September fell by -0.6 points to 60.5, which did not bode well for today’s ISM report for September.