- Unemployment claims expected to show continued labor market strength

- U.S. productivity expected to turn negative

- U.S. Sep trade deficit expected to widen to a new record

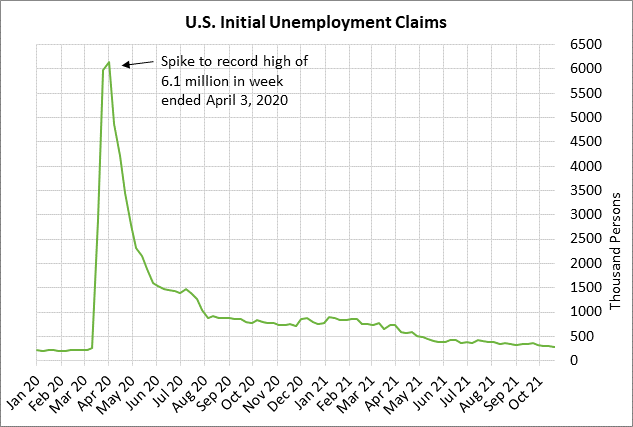

Unemployment claims expected to show continued labor market strength — The consensus is for today’s weekly initial unemployment claims report to show a -6,000 decline to 275,000, adding to last week’s decline of -10,000 to 281,000. Initial claims last week fell to a new 1-1/2 year low.

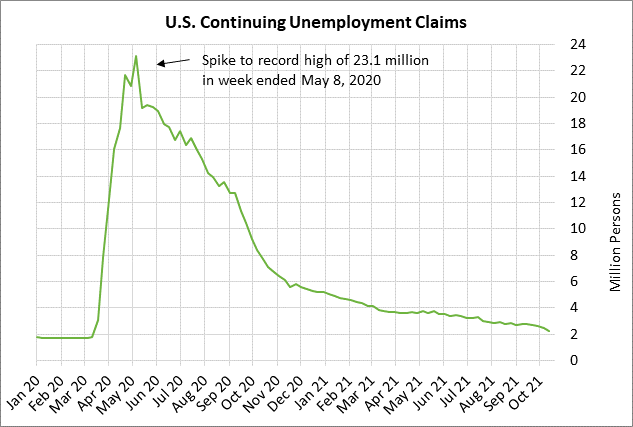

Today’s continuing claims report is expected to show a -96,000 decline to 2.147 million, adding to last week’s -237,000 decline to 2.243 million. Continuing claims are in strong shape as the series last week fell to a new 1-1/2 year low.

Friday’s Oct payroll report is expected to show a moderate gain of +450,000. The markets are hoping for a substantial improvement from the disappointing Sep payroll report of +194,000, which was much weaker than expectations at the time of about +500,000. The consensus is for Friday’s Oct unemployment rate to be unchanged from September at 4.8%. The unemployment rate in October fell sharply by -0.4 points to a 1-1/2 year low of 4.8%.

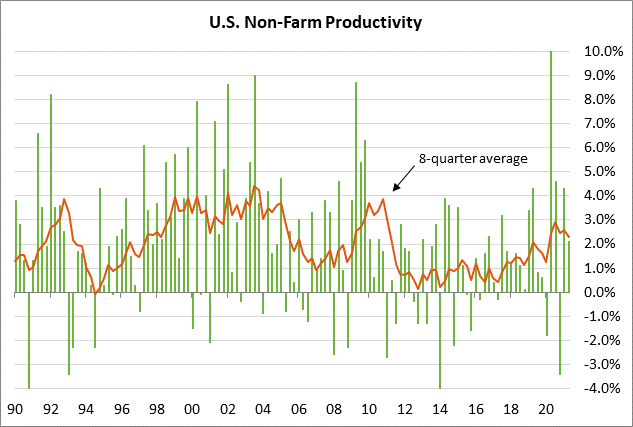

U.S. productivity expected to turn negative — Today’s Q3 nonfarm productivity report is expected to show a decline of -3.1% (q/q annualized), following Q2’s report of +2.1%. The productivity figures have been very volatile during the pandemic.

Productivity earlier this year showed increases of +4.3% in Q1 and +2.1% in Q2 due to the sharp recovery in GDP growth, which boosted the output numerator of the productivity ratio. However, productivity is expected to fade in Q3 due to slower GDP growth (lower productivity numerator) and an increase in hiring and hours worked (increased productivity denominator).

The long-term trend for U.S. productivity continues to slope downwards. U.S. productivity saw strength in the late 1990’s and early 2000’s due to the computer technology and Internet revolution. However, productivity in the 2012-18 years was rather poor since the bulk of technology advances had already been captured. The outlook is for continued ho-hum productivity figures, which would have negative implications for real wages, inflation, and corporate profits.

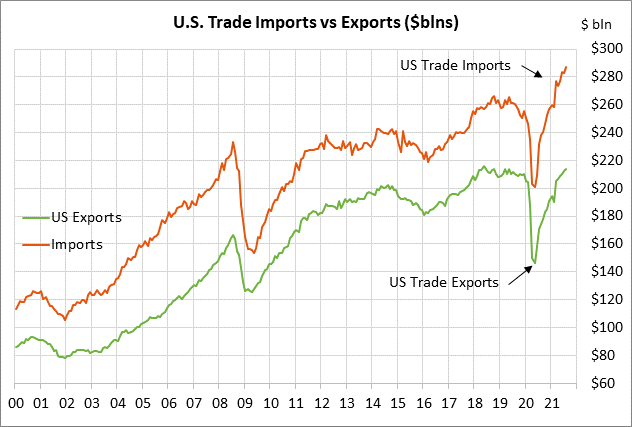

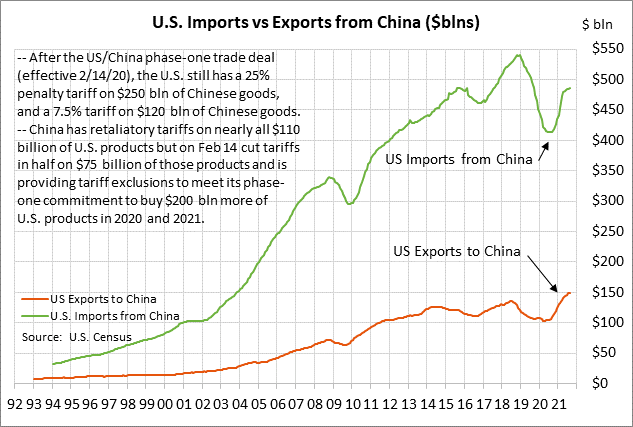

U.S. Sep trade deficit expected to widen to a new record — Today’s U.S. trade deficit is expected to widen to a new record -$80.2 billion from August’s record high of -$73.3 billion.

The U.S. trade deficit has soared since the pandemic began in early 2020 because exports have been hurt by weak overseas growth, while imports have been boosted by the massive amount of federal stimulus and the soaring U.S. economy. From the pre-pandemic levels seen in February 2020, imports rose by +16.4% through August 2021, while exports rose by only +4.4% over that same time frame. However, this situation will likely start to reverse in 2022 as the U.S. economy cools, causing the U.S. trade deficit to narrow somewhat in 2022.

The markets continue to carefully watch U.S. trade relations with China. The Biden administration has yet to take action to ease any of the aggressive trade moves made by the Trump administration. There continue to be penalty tariffs on virtually all U.S. trade with China.

After the U.S. and China reached their phase-one trade deal, which took effect in February 2020, the U.S. kept in place a 25% penalty tariff on about $250 billion of Chinese goods. Meanwhile, China left in place retaliatory tariffs on most of the products that it imports from the U.S.

As part of the Trump administration’s phase-one trade deal, China agreed to buy $200 billion more of U.S. products in 2020 and 2021. China has met only about one-half of that purchase target. The Biden administration has said that it expects China to finish living up to its purchase obligations. However, the Biden administration has not threatened to impose any punishment on China for not meeting those purchase targets.

The Biden administration continues to take a relatively hard line towards China and has made no serious moves to begin negotiations on the ongoing trade issues between the two countries. In the meantime, penalty tariffs continue on most of the two-way trade between the U.S. and China.

U.S. trade flows with China have been severely disrupted since early 2020 by the pandemic, making it difficult to isolate the impact of the penalty tariffs and China’s $200 billion purchase obligation. The good news is that U.S. exports to China in the past year have increased to a record high. At the same time, however, U.S. imports from China

have also risen sharply, preventing any major decline in the U.S. trade deficit with China.

The annualized U.S. trade deficit with China on a 12-month trailing basis was at -$337 billion in August, narrower than the record high deficit of -$419 billion seen in December 2018. However, the current deficit is just mildly narrower than the deficit of -$367 billion seen when the Trump administration came into office in January 2016 and vowed to do away with the U.S. trade deficit with China.