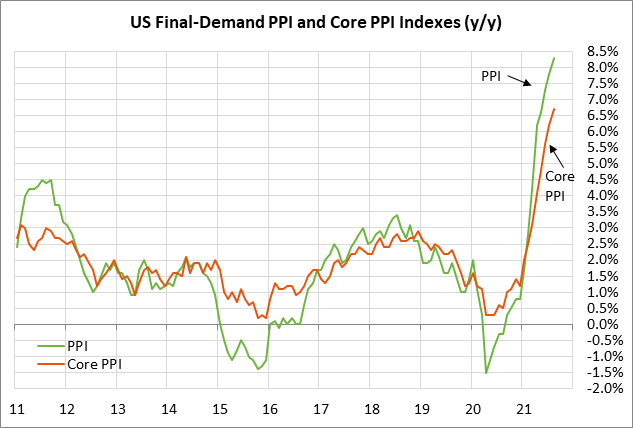

- Sep U.S. PPI report expected to confirm strength in CPI report

- FOMC minutes seem to confirm QE tapering at upcoming Nov 2-3 meeting

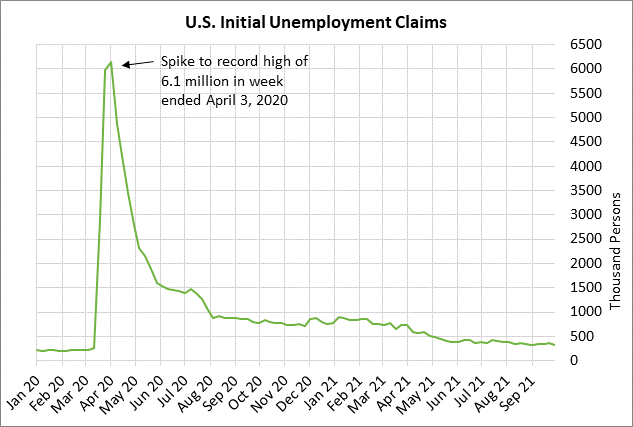

- Weekly unemployment claims expected to show continued slow labor market improvement

Sep U.S. PPI report expected to confirm strength in CPI report — Yesterday’s CPI report was slightly stronger than expected, which means the markets will be watching today’s PPI report to see if it is also stronger than expected. The consensus is for today’s Sep final-demand PPI to show another sharp increase of 0.6% m/m and +8.7% y/y, following August’s report of +0.7% and +8.3%, respectively. The consensus is for today’s Sep core PPI to also show a strong increase of +0.5% m/m and +7.1% y/y, following August’s report of +0.6% and +6.7%, respectively.

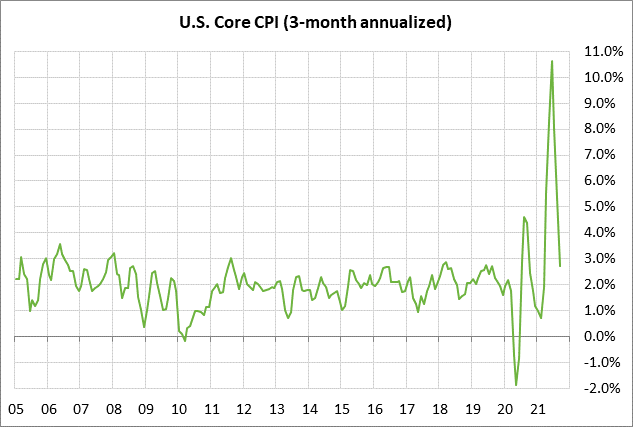

Yesterday’s Sep CPI report of +0.4% m/m and +5.4% y/y was slightly stronger than expectations of +0.3% and +5.3%, respectively. However, the core CPI report of +0.2% m/m and +4.0% y/y was in line with market expectations.

Still, there was some good news on the inflation front in yesterday’s CPI report since the headline CPI, on a 3-month annualized basis, dropped to 4.7% from August’s +6.8% and June’s peak of +9.7%. The Sep core CPI (3-month annualized) fell to a comfortable +2.7% from +5.4% in August and June’s peak of +10.6%.

Even though yesterday’s CPI figures eased on a 3-month basis, the markets and the Fed remain concerned that the current inflation surge could last longer than previously thought and could turn into something more structural. Yesterday’s minutes from the Sep 21-22 FOMC meeting indicated that Fed officials are becoming more concerned about inflation. The minutes said, “Most participants saw inflation risks as weighted to the upside because of concerns that supply disruptions and labor shortages might last longer and might have larger or more persistent effects on prices and wages than they currently assumed.”

Atlanta Fed President Bostic on Tuesday already said he thought inflation pressures have lasted too long to still be considered “transitory.” He said, “I believe evidence is mounting that price pressures have broadened beyond the handful of items most directly connected to supply-chain issues or the reopening of the services sector.”

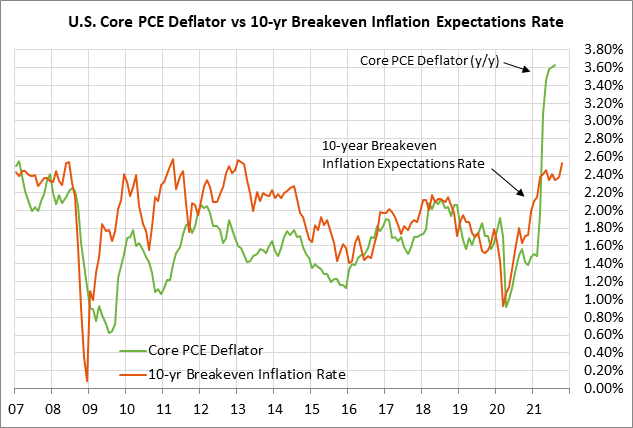

The markets have sharply boosted their inflation expectations over the past several weeks as oil and natural gas prices surge and as supply chain disruptions boost prices across the board for many different types of products. The 10-year breakeven inflation expectations rate on Wednesday rose to a new 4-3/4 month high of 2.53%, which is more than one-half percentage point above the Fed’s +2.0% inflation target.

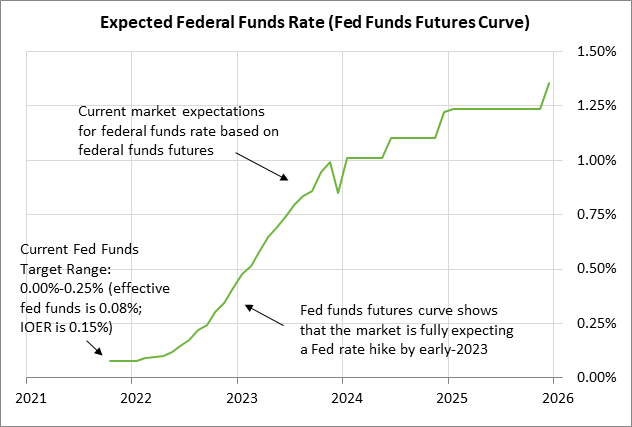

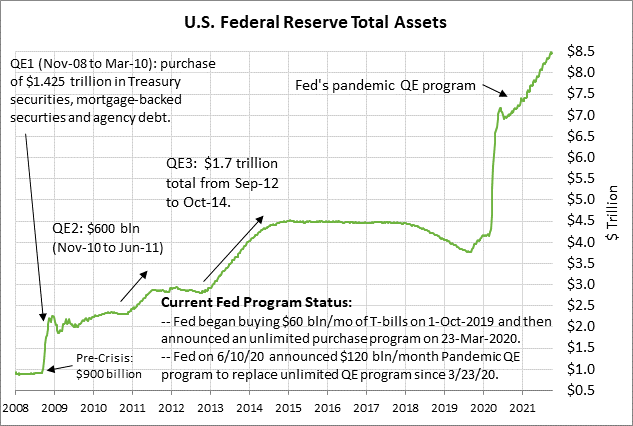

FOMC minutes seem to confirm QE tapering at upcoming Nov 2-3 meeting — Yesterday’s release of the minutes from the Sep 21-22 FOMC meeting seemed to confirm that the Fed is planning to announce QE tapering at its next meeting on Nov 2-3. The minutes said, “Participants noted that if a decision to begin tapering purchases occurred at the next meeting, the process of tapering could commence with the monthly purchase calendars beginning in either mid-November or mid-December. The minutes added, “Participants generally assessed that, provided that the economic recovery remained broadly on track, a gradual tapering process that concluded around the middle of next year would likely be appropriate.”

The FOMC even went so far as to lay out an illustrative tapering path, saying, “The path featured monthly reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities.

Weekly unemployment claims expected to show continued slow labor market improvement — Today’s unemployment claims report is expected to show a continued slow improvement in the U.S. labor market. The consensus is for today’s initial unemployment claims report to fall by -6,000 to 320,000, adding to last week’s decline of -38,000 to 326,000. Meanwhile, today’s continuing claims report is expected to fall by -44,000 to 2.670 million, adding to last week’s -97,000 decline to 2.714 million.

The initial and continuing claims series are not far above their recent lows. Initial claims are +14,000 above the 19-month low of 312,000 posted in the week ended Sep 3, while continuing claims are just 1,000 above the 19-month low of 2.714 million posted in the week ended Sep 3. Relative to the pre-pandemic levels, initial claims are elevated by +110,000, and continuing claims are elevated by 1.006 million.

There has been some disappointing news on the labor front in the past week. Tuesday’s Aug JOLTS job openings report fell sharply by an unexpected -659,000 to 10.439 million, falling back from July’s record high of 11.098 million. The decline in job openings suggested that businesses in August pulled back on their hiring plans as the pandemic surged due to the delta variant.

In fact, the Sep payroll report turned out to be surprisingly weak at +194,000, much weaker than expectations of +500,000. On the stronger side, however, the Sep unemployment rate fell to a new 1-1/2 year low of 4.8%, creeping closer to the pre-pandemic record low of 3.5%.

While the recent labor market data has been a bit weak, the labor market should strengthen in the coming months due to the sharp drop in the Covid infection figures seen since mid-September. Businesses are likely to boost their hiring in October and November on relief that the pandemic’s resurgence appears to be over, making it safer to boost their employee levels and prepare for a continued strong economy. There should be particular optimism in pandemic-sensitive industries such as restaurants, travel, and entertainment.