- QE tapering is still a ways off

- Senate votes to bring infrastructure bill to the floor

- U.S. GDP expected to peak in Q2 at +8.5%

- Initial claims expected to reverse part of last week’s surge

- 7-year T-note auction to yield near 0.99%

QE tapering is still a ways off — Fed Chair Powell yesterday successfully kept the markets calm even as the Fed took a further step towards QE tapering. Mr. Powell said that the FOMC, at its 2-day meeting that ended Wednesday, took its “first deep dive” into exactly how QE tapering could be handled.

However, Mr. Powell said, “We’re not there. And we see ourselves as having some ground to cover to get there.” He added, “We’re making progress. We expect further progress and if things go well we will reach that goal.”

The FOMC outcome did not appear to change the market’s previous forecast for the QE tapering schedule. A recent survey by Bloomberg taken on July 16-21 found that 74% of respondents expect the Fed to provide an early warning of QE tapering at its August 26-28 Jackson Hole conference or at the next FOMC meeting on September 21-22.

The survey found that 36% of the respondents expect the Fed to formally announce its QE program somewhere between September and November, while the largest plurality of 47% expect that announcement in December.

Regarding the actual implementation date, a hefty 71% of respondents expect the tapering to begin in Q1-2022. The remaining respondents were roughly split about whether the tapering will be either before or after Q1.

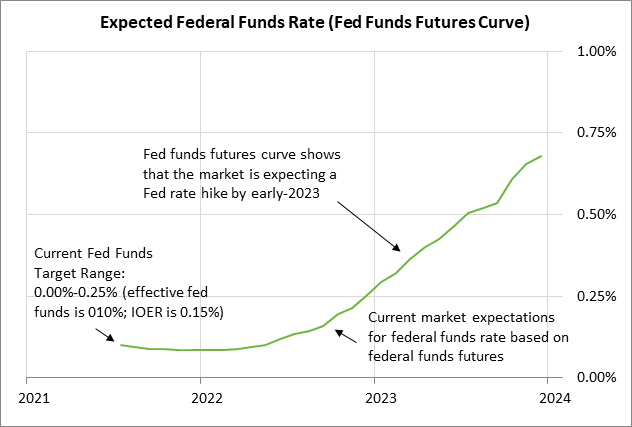

The Dec 2023 federal funds futures contract on Wednesday showed a slightly hawkish reaction to the FOMC meeting outcome by rising +3.5 bp to 0.68%. The market is still not fully expecting a +25 bp rate hike until early 2023, and is then expecting a second rate hike later in 2023.

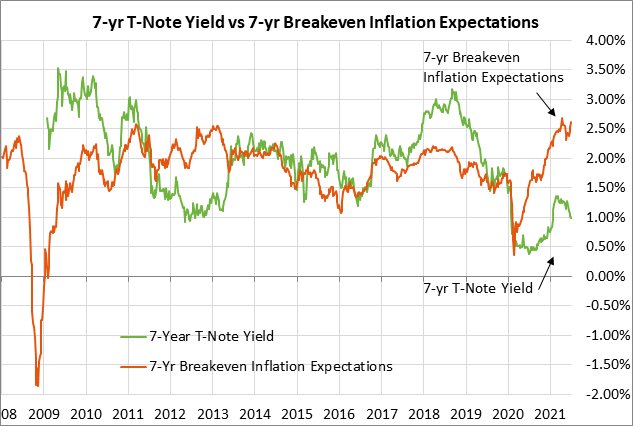

Regarding inflation, the FOMC reiterated that the current inflation surge is “largely reflecting transitory factors.” The markets continue to hope that the Fed is right and that inflation will fall back to more normal levels by early next year as fiscal stimulus and reopening pressures fade. The 10-year breakeven inflation expectations rate has risen by 20 bp since last week to 2.41%, but remains well below the 8-1/4 year high of 2.59% posted in May.

Senate votes to bring infrastructure bill to the floor — The bipartisan group of Senators on Wednesday reached an agreement on a $550 billion infrastructure bill. Senate Majority Leader Schumer quickly called a cloture vote to bring the bill to the floor, which easily passed by a margin of 67-32, surpassing the filibuster minimum of 60 votes. All of the Democratic Senators voted in favor of the bill, and 17 Republicans also voted in favor. The wrangling will now begin on the Senate floor on the final content of the bill. Mr. Schumer is hoping to get the bill passed on the floor before the Senate is due to recess next Friday (Aug 6).

Now that the bipartisan infrastructure bill has made it to the Senate floor, Democrats need to finalize the terms of their $3.5 trillion budget resolution. Mr. Schumer also wants to get that bill passed before leaving for recess next Friday, which would set the stage for the Senate to consider the $3.5 trillion reconciliation bill this autumn. House Speaker Pelosi says the House will not consider the Senate’s infrastructure bill until the Senate also passes the $3.5 trillion spending bill.

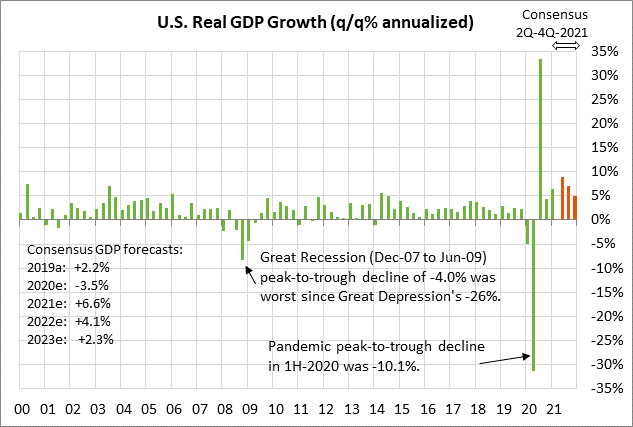

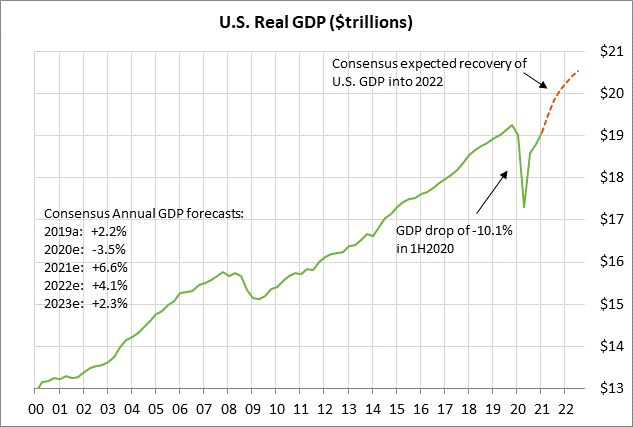

U.S. GDP expected to peak in Q2 at +8.5% — The consensus is for today’s Q2 GDP to surge by +8.5% (q/q annualized), strengthening from +6.4% in Q1. Q2 personal consumption is expected to ease a bit to +10.5% from Q1’s +11.4% as the impact fades from stimulus checks.

After peaking in Q2, GDP growth is then expected to decelerate to +7.1% in Q3 and +5.0% in Q4. On a calendar year basis, GDP growth is expected to surge to +6.6% in 2021, which would be the strongest annual growth rate in 37 years (i.e., since 1984). Looking ahead, GDP growth is expected to show another strong increase of +4.1% in 2022, but then fade to normal levels by 2023 of +2.3%.

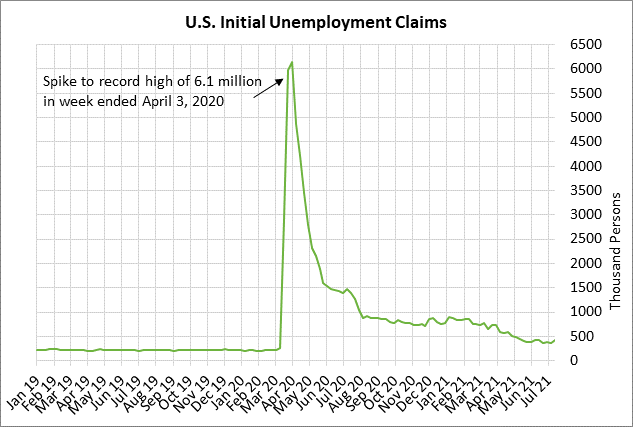

Initial claims expected to reverse part of last week’s surge — The consensus is for today’s weekly initial unemployment claims report to show a decline of -34,000 to 385,000, reversing most of last week’s +51,000 increase to 419,000. Last week’s increase in initial claims was mostly due to technical factors, but there may have also been an increase in layoffs as some businesses cut back due to the recent surge in Covid infections. Initial claims are currently +203,000 above the pre-pandemic level seen at the end of February 2020.

Meanwhile, today’s continuing claims report is expected to show a decline of -50,000 to 3.186 million, adding to last wee’s decline of -29,000 to a 16-month low of 3.236 million. Continuing claims are still +1.5 million above the pre-pandemic level.

7-year T-note auction to yield near 0.99% — The Treasury today will sell $62 billion of 7-year T-notes, concluding this week’s $211 billion T-note auction package. The 7-year T-note yield yesterday closed at 0.99%, which is only 9 bp above the mid-July 5-1/2 month low of 0.90%.

The 12-auction averages for the 7-year are as follows: 2.33 bid cover ratio, $14 million in non-competitive bids, 5.7 bp tail to the median yield, 50.2 bp tail to the low yield, and 45% taken at the high yield. The 7-year is mildly below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 59.8% of the last twelve 7-year T-note auctions, which is mildly below the median of 61.2% for all recent Treasury coupon auctions.