- Bipartisan infrastructure bill may get another vote next week

- CBO says Treasury’s debt-limit X-date isn’t until October or November

- ECB meeting expected to produce revised guidance

- U.S. existing home sales expected to snap 4-month losing streak

- U.S. LEI expected to show another strong increase

- U.S. unemployment claims expected to show labor market improvement

- 10-year TIPS auction to yield near -1.02%

Bipartisan infrastructure bill may get another vote next week — As expected, the Senate yesterday failed to pass the cloture motion to advance the bipartisan infrastructure bill to the Senate floor for debate. However, the good news for Senate Majority Schumer was that all of his Democratic Senators voted in favor of the bill, except for Mr. Schumer himself because of a technical maneuver to allow the cloture vote to be brought up again in the future.

Despite the cloture vote, moderate Republicans said that they will keep working on the bipartisan bill with their Democratic counterparts and that they will vote in favor of cloture early next week if the group can reach an agreement. Mr. Schumer told moderate Democratic Senators he will hold another cloture vote if the bipartisan group can produce the 60 votes necessary to advance the legislation. Thus, another cloture vote is possible next week.

Meanwhile, Senate Budget Committee Chairman Bernie Sanders is burning up time trying to get all 50 Democratic Senators on board with a $3.5 trillion spending bill. Mr. Sanders said yesterday that a vote on the budget resolution may not come until early August, just before the recess. The budget resolution must be passed to set the stage for a $3.5 trillion reconciliation bill that will be considered by the Senate this autumn.

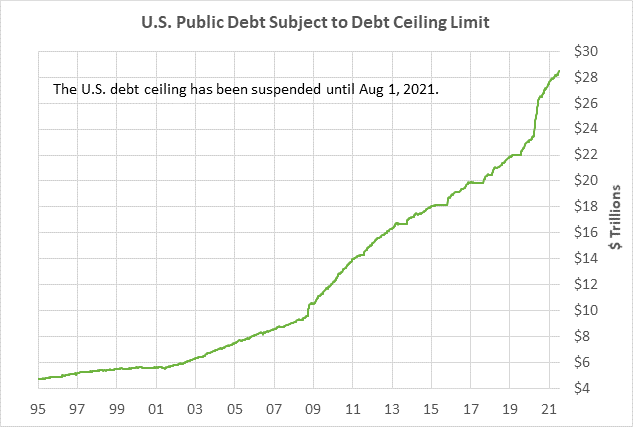

CBO says Treasury’s debt-limit X-date isn’t until October or November — The non-partisan Congressional Budget Office (CBO) yesterday said that it estimates that the Treasury’s X-date will come sometime in Q4, likely in October or November. The debt limit will be reinstated on August 1 and the Treasury will then be forced to use emergency procedures to conserve its cash. On the X-date, the Treasury will run out of cash and will start defaulting on its financial obligations, possibly including the payment of interest and principal on Treasury securities.

The Democrats have a serious problem on their hands about how to raise the debt ceiling. They could include a debt ceiling hike in the $3.5 trillion reconciliation bill, but passage of that bill might not come in time for the Treasury’s X-date. Otherwise, the Democrats would need the help of at least 10 Republicans in the Senate to pass the legislation. Senate Republicans yesterday made it clear they will not support a debt ceiling hike unless Democrats meet a laundry list of demands.

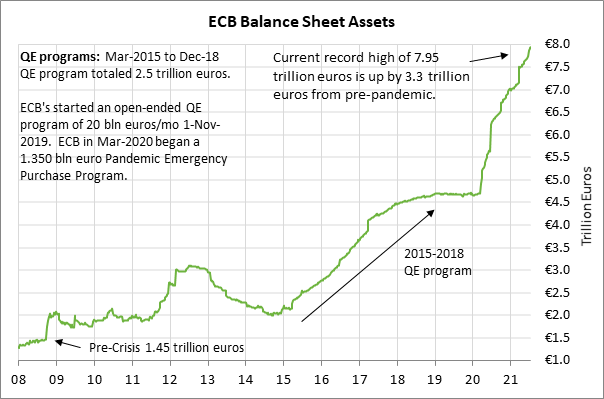

ECB meeting expected to produce revised guidance — The ECB today will announce the outcome of its policy meeting where it must decide how to translate its new inflation target into short-term policy action and guidance. After a long policy review, the ECB earlier this month announced that it raised its inflation target to 2% (from just under 2%) and said it would be “forceful or persistent” in reaching that target.

While the ECB will need to change some of its language today, the ECB is not expected to change its interest rate or QE policies. The ECB’s deposit rate is currently at -0.50%. Regarding QE programs, the ECB has its Asset Purchase Program (APP) of 20 bln euros/mo and a Pandemic Emergency Purchase Program (PEPP) of 1.85 trillion euros lasting through March 2022.

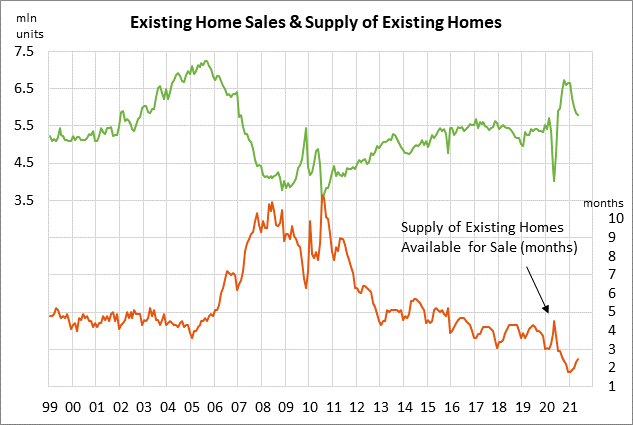

U.S. existing home sales expected to snap 4-month losing streak — The consensus is for today’s June existing home sales report to show an increase of +1.7% m/m to 5.90 million, more than reversing May’s -0.9% decline to 5.80 million. Existing home sales have fallen for four straight months due to the small supply of homes on the market and resistance by potential buyers to the sharp increase in home prices seen during the pandemic. The median price of an existing home rose to $350,300 in May, which is up by +32% from the $266,300 level seen in January 2020 before the pandemic emerged.

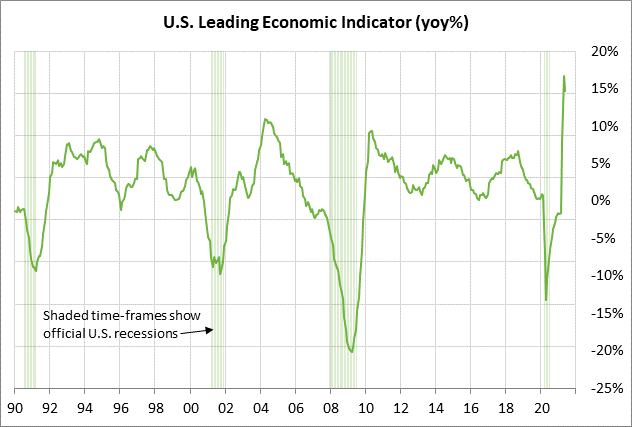

U.S. LEI expected to show another strong increase — The consensus is for today’s June leading indicators report to show another strong increase of +0.9% m/m, adding to May’s increase of +1.3%. The LEI has not shown a decline in the past 13 months and was up sharply by +14.7% y/y in May. The consensus is that U.S. GDP growth in Q2 soared by +9.0% (q/q annualized). The market is expecting GDP growth to remain strong at +7.1% in Q3 and +5.1% in Q4. The consensus is for calendar-year 2021 GDP growth of 6.6%, which would more than overcome the -3.5% decline seen in 2020.

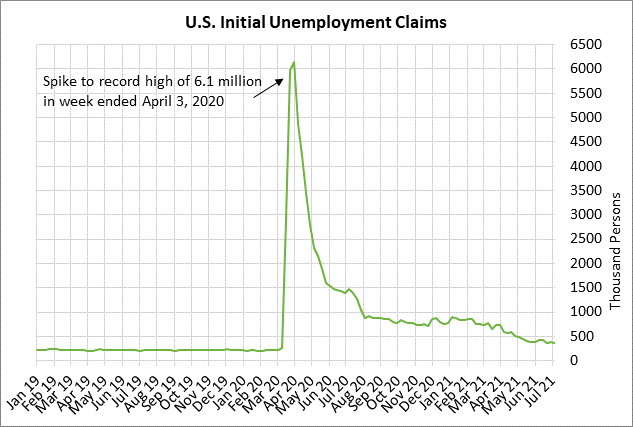

U.S. unemployment claims expected to show labor market improvement — Today’s unemployment claims report is expected to show a continued improvement in the labor market with initial claims showing a -10,000 decline to 350,000 and continuing claims showing a -141,000 decline to 3.110 million. Initial claims are now up by only +144,000 from the pre-pandemic level. However, continuing claims are still up by 1.533 million from the pre-pandemic level.

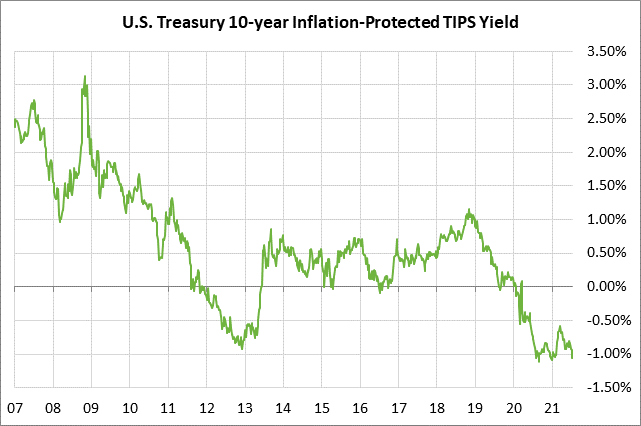

10-year TIPS auction to yield near -1.02% — The Treasury today will sell $16 bln of 10-year TIPS. The benchmark 10-year TIPS yield yesterday closed at -1.02%, which was +10 bp above Monday’s 6-1/2 month low of -1.12%.

The 12-auction averages for the 10-year TIPS are: 2.44 bid cover ratio, $24 million in non-competitive bids, 7.0 bp tail to the median yield, 25.8 bp tail to the low yield, and 56% taken at the high yield. The 10-year TIPS is the third most popular security among foreign investors and central banks, behind the 30-year TIPS and 5-year TIPS. Indirect bidders, a proxy for foreign buyers, have taken an average of 67.0% of the last twelve 10-year TIPS auctions, well above the median of 61.2% for all recent Treasury coupon auctions.