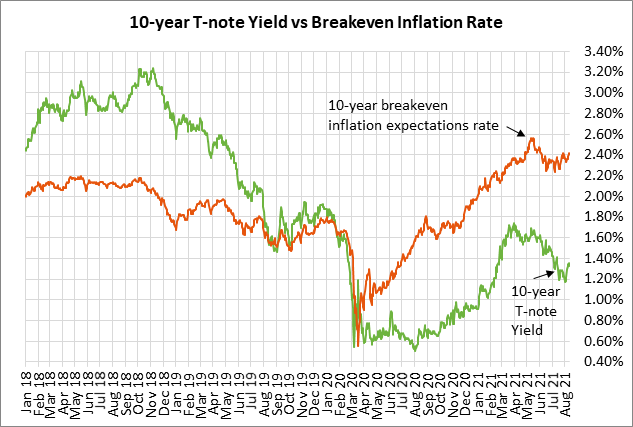

- U.S. inflation expectations rise to 2-1/4 month high

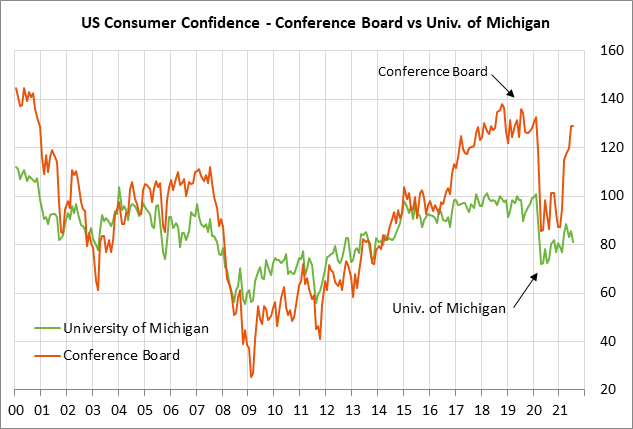

- U.S. consumer sentiment index expected to stabilize after recent declines

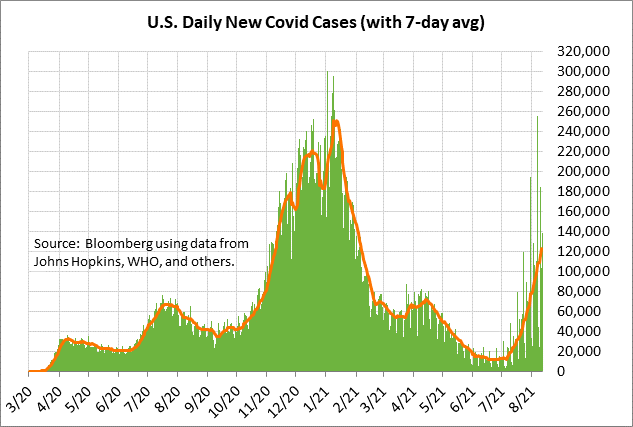

- Surge in U.S. Covid infections is now halfway to all-time highÂ

U.S. inflation expectations rise to 2-1/4 month high — The 10-year breakeven inflation expectations rate on Thursday edged to a new 2-1/4 month high of 2.44% and closed the day up +2 bp at 2.42%.

U.S. inflation expectations pushed higher on Thursday due to the much stronger than expected PPI report, which suggested that there is still a strong dose of inflation in the producer pipeline. The July final-demand PPI rose by +1.0% m/m and +7.8% y/y, which was much stronger than expectations of +0.6% m/m and +7.2%. The July core PPI rose by +1.0% m/m and +6.2% y/y, which was also much stronger than expectations of +0.5% m/m and +5.6% y/y.

The PPI report was an unwelcome development after Wednesday’s CPI report at least showed some easing on a 3-month basis. On a 3-month annualized basis, the July CPI eased to +8.4% from June’s peak of +9.7%, and the July core CPI eased to +8.1% from June’s peak of +10.6%.

Despite the alarming inflation statistics seen recently, the markets continue to concur with the Fed that the current inflation surge is transitory. The Fed makes the case that much of the strength in the inflation statistics is in sectors linked to pandemic reopenings. The Fed expects inflation to cool next year. The FOMC’s consensus forecast is that the core PCE deflator will ease to +2.1% by the end of 2022, down from the expected +3.0% level seen at the end of this year.

U.S. consumer sentiment index expected to stabilize after recent declines — The consensus is for today’s preliminary-Aug University of Michigan U.S. consumer sentiment index to be unchanged at 81.2, stabilizing after July’s -4.3 point decline to 81.2.

The consumer sentiment index peaked in April at a 16-month high of 88.3, and has since fallen by -7.1 points to July’s 5-month low of 81.2. The index remains far below the pre-pandemic level of 99.3 seen in December 2019.

Consumer sentiment initially surged this spring after vaccines became widely available and the Covid infection rate plunged in February and March. However, the delta variant has caused a new surge in the pandemic that has caused new worries among many consumers.

In addition, the labor market is far from healthy with the U.S. economy still down by 5.7 million jobs from the pre-pandemic level. Hiring rose sharply in June and July but may fade again as businesses wait to see how bad the Covid resurgence will be and whether there will be new economic shutdowns.

Consumers are also being hit by high gasoline prices, which are taking a bite out of their pocketbooks. Regular gasoline prices are currently at a national average of $3.19 per gallon, according to AAA, which is a 6-1/4 year high. The Biden administration earlier this week called on OPEC+ to boost production to ease oil and gasoline prices, but the call fell on deaf ears at the cartel.

Surge in U.S. Covid infections is now halfway to all-time high — The 7-day average of new U.S. Covid infections continues to rise sharply and posted a new 6-1/4 month high on Wednesday of 122,649. In just the past six weeks, infections have risen by more than ten times from the 16-month low of 11,351 posted on June 23. The surge in Covid infections is now about halfway to the record high of 250,464 posted earlier this year in mid-January.

The fact that the pandemic has surged to half its previous peak, even with about half of the U.S. population being vaccinated, illustrates the game-changing transmissibility of the delta variant. The number of infections continues to rise quickly since little is being done from the standpoint of masks, social distancing, or economic shut-downs to slow the revived pandemic.

Most of the U.S. populace seems to fed up with masks and economic shutdowns, which means the pandemic may simply have to burn itself out over a number of months or even years by infecting most of those that aren’t vaccinated to give them some immunity, thus allowing the U.S. to reach some semblance of herd immunity.

The markets do not seem to be overly concerned about the resurgence of the pandemic. The markets seem to believe that U.S. businesses have largely learned to live with the pandemic and will be able to keep the corporate earnings machine going. However, there are still big risks in sectors of the economy that may yet see new shutdowns such as restaurants, travel, and entertainment.

The risks to economic growth are even higher in China due to its zero-tolerance approach to Covid. China on Thursday partially shut down about 25% of the world’s third busiest port because a single worker tested positive for Covid. Chinese authorities shut down the Meishan terminal at the Ningbo-Zhoushan port.

There will be some fall-out for global shipping from the Chinese port shutdown. Other ports around the world will see shipping volumes drop, there could be additional upward pressure on already-high shipping rates, and there will be new supply chain disruptions for some global companies.

In response to the delta variant, China has already taken a series of draconian steps to try to stamp out the variant before it gets a foothold. For example, China has halted flights in and out of Beijing. Data from aviation specialist OAG showed the number of seats being offered by Chinese carriers plunged -32% in one week and sent global carrier capacity down -6.5%.