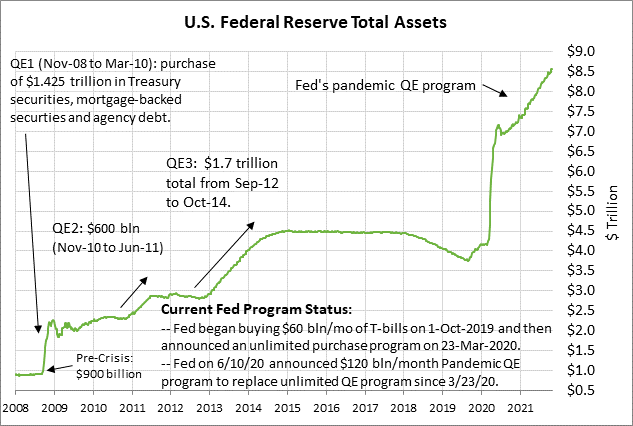

- Markets expect QE tapering to be announced at 2-day FOMC meeting that ends today

- U.S. ADP employment expected to show moderate increase

- U.S. Oct ISM services index expected to remain strong

- U.S. factory orders

Markets expect QE tapering to be announced at 2-day FOMC meeting that ends today — The markets are unanimously expecting the FOMC at its 2-day meeting that ends today to announce QE tapering. The Fed has clearly telegraphed that a QE tapering announcement is likely at this week’s meeting.

Fed Chair Powell, in comments delivered on October 22, said, “We are on track to begin a taper of our asset purchases, that, if the economy evolves broadly as expected, will be completed by the middle of next year.” He added, “I do think it is time to taper and I don’t think it is time to raise rates.”

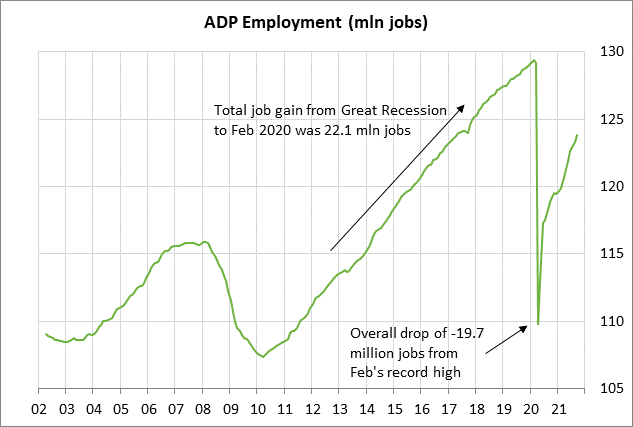

U.S. ADP employment expected to show moderate increase — The consensus is for today’s Oct ADP employment report to show an increase of +4000,000, falling back after September’s strong report of +568,000.

ADP job growth was weak in July (+322,000) and August (+340,000), but then improved to +568,000 in September. ADP jobs still need to recover by another 5.5 million to match the pre-pandemic record high.

On the labor front, the markets are mainly looking ahead to Friday’s Oct unemployment report. Friday’s Oct payroll report is expected to show a moderate gain of +450,000. The markets will be looking for a substantial improvement from the disappointing Sep payroll report of +194,000, which was much weaker than expectations at the time of about +500,000. Payrolls still need to rise by another +5.0 million to reach the pre-pandemic record high.

Payroll growth was very strong in June (+964,000) and July (+1.091 million) as businesses started rehiring when the pandemic infection figures fell sharply through July. However, the delta variant then caused a resurgence in the pandemic figures in August and early September.

The pandemic’s resurgence in August and early September caused businesses to cut back on hiring as they waited to see how long the resurgence might last. The pandemic’s resurgence also reduced the pool of workers willing to take a job because they were concerned about their safety or had to stay at home to take care of children.

Job growth is now expected to improve in October since the pandemic’s resurgence peaked in mid-September and fell steadily through October. However, the job hiring process can take at least a month, and the improved job figures might not fully emerge until November.

The job hiring figures continue to be undercut by labor shortages in a variety of industries. There are a large number of job openings available, but some businesses are having trouble filling those positions because there is a shortage of qualified and willing job applicants. The official U.S. job level is also being undercut by the larger number of people who are quitting their jobs because they found a more desirable or higher paying job, or because they think they will find a better job and want to quit and start looking.

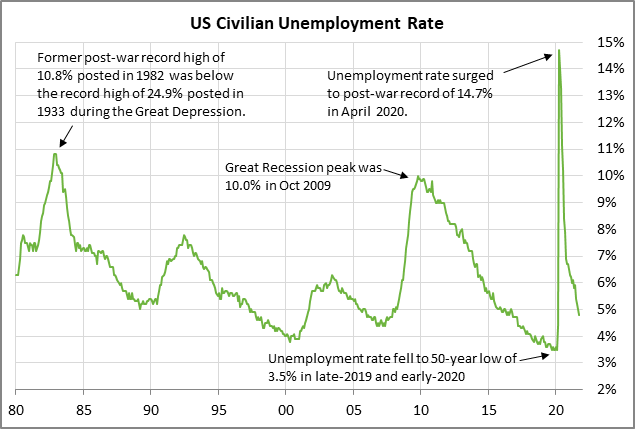

The consensus is for Friday’s Oct unemployment rate to fall by -0.1 point to 4.7%. The unemployment rate in September fell sharply by -0.4 points to a 1-1/2 year low of 4.8%. The unemployment rate in September was only 1.3 percentage points above the 50-year low of 3.5% seen before the pandemic.

However, the low unemployment rate is artificially low and is signaling better labor market conditions than actually exist. In fact, the size of the U.S. labor force has contracted considerably due to pandemic factors, resulting in fewer people who are in the job market and who are being counted in the unemployment statistics. The size of the U.S. labor force has contracted because of a high level of retirements during the pandemic and because there are still many people who are not working because of safety concerns or because they need to stay home to take care of children.

The smaller labor force size can be seen by the fact that the U.S. labor force participation rate is only at 61.6%, which is well below the pre-pandemic level of 63.3% seen in December 2019. However, as more people are drawn back into the labor market as the pandemic fades and as wages rise, the size of the workforce will increase as more people start looking for a job and are once again counted in the unemployment statistics. That means that further declines in the unemployment rate are likely to become more difficult.

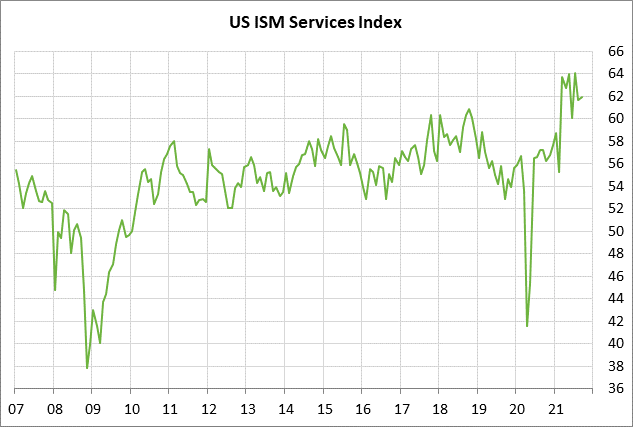

U.S. Oct ISM services index expected to remain strong — The consensus is for today’s Oct ISM services index to show a +0.1 point increase to 62.0, adding to September’s small +0.2 point rise to 61.9.

The ISM services index has backed off from July’s record high of 61.4, but is still at a high level that indicates strong confidence in the service sectors of the U.S. economy. September’s index level of 61.9 was well above the pre-pandemic level of 55.6 seen in December 2019.

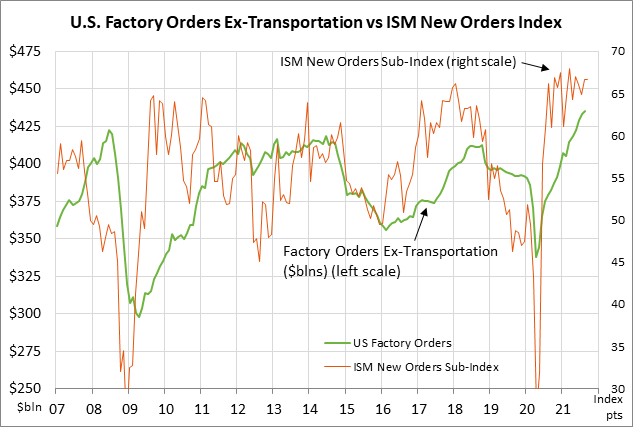

U.S. factory orders — The consensus is for today’s Sep factory orders report is +0.1% m/m and unch ex-transportation, following August’s report of +1.2% m/m and +0.5% ex-transportation.

U.S. factory orders showed strong increases during May-August as the pandemic faded through July and led to a burst of orders. In August, factory orders were up by +10.1% on a year-to-date basis. Factories are busy trying to fulfill all the orders they are getting, but are being hampered to some degree by the supply-chain disruptions and high fuel and shipping costs.