- Weekly market focusÂ

- Markets look ahead to faster QE tapering and rate hikes in 2022

- Senate Democrats will likely need to revise Build Back Better bill after Manchin says he is a “no”

- Nov LEI expected to show strength

- Earnings surge expected to start abating in Q4

- U.S. Covid infection rises to 2-3/4 month high as omicron hits

Weekly market focus — The markets this week will focus on (1) the pandemic situation as the omicron variant spreads globally, (2) further analysis of how quickly the Fed might raise interest rates in 2022, (3) this week’s busy economic calendar before Friday’s Christmas holiday, and (4) the prospects for the Build Back Better bill after Senator Manchin on Sunday said he is a “no” on the bill.

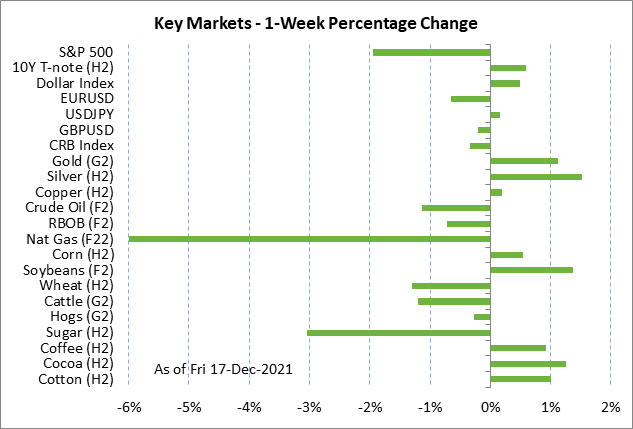

Markets look ahead to faster QE tapering and rate hikes in 2022 — The markets last week were forced to adjust to a more hawkish Fed stance as the Fed reacts to the inflation surge. The FOMC last Wednesday announced that it will double the speed of its QE tapering, thus ending its QE program by March 2022, three months earlier than originally announced. That would give the Fed the option to start raising interest rates as soon Q2-2022.

Also, FOMC members, in their dot-plot, forecasted three rate hikes for 2022, three more rate hikes in 2023, and two more rate hikes in 2024. That path would leave the funds rate at 2.1% by the end of 2024, up by two full percentage points from the current level.

The markets on Friday took note of hawkish comments from Fed Governor Waller, who provided his interpretation of last week’s FOMC meeting. He said, “The whole point of accelerating the tapering was to end it much faster in March so that the March meeting could be a live meeting. That was the intent.†He added, “My outlook is that it’s a very likely outcome that it could happen in March. It would take something like severe disruption from omicron to delay labor market improvement or keep unemployment from falling, to keep March from being a key date to think of for liftoff.†Mr. Waller also said he favors starting to shrink the Fed’s balance sheet by early summer.

Senate Democrats will likely need to revise Build Back Better bill after Manchin says he is a “no” — The Senate will be on holiday recess this week but will continue to discuss the Build Back Better bill. Democratic Senator Manchin on Sunday said he is a “no” on the bill. His main complaint seems to be that the child tax credit is not being scored for 10 years. It remains to be seen whether Mr. Manchin’s stance is a hardball negotiating tactic, or whether he will refuse to vote in favor of anything like the BBB bill.

Aside from Mr. Manchin’s stance, the BBB bill has been bogged down by scrubbing by the Senate parliamentarian to see if all the measures in the bill qualify for the budget reconciliation process.

The markets are getting out of 2021 with some good news from Washington after Congress in the past month has managed to avoid a government shutdown and a Treasury default. Congress late Tuesday approved a debt ceiling hike that will last until early 2023. Congress earlier this month approved a continuing resolution that will keep the U.S. government operating until February 18.

Nov LEI expected to show strength — The consensus is for today’s Nov leading indicators report to show a solid increase of +0.9% m/m, matching Oct’s +0.9% increase. On a year-on-year basis, the LEI remained very strong in October at +9.3% y/y, although that is down from the peak of +16.8% posted this past April.

The consensus is for U.S. GDP growth to decelerate in coming quarters. U.S. GDP growth slumped to +2.1% (q/q annualized) in Q3 due to the pandemic’s resurgence and economic obstacles such as supply chain disruptions and labor market shortages.

GDP growth is expected to recover to +6.0% in Q4, but then decelerate to +4.0% in Q1-2022, +3.6% in Q2, +3.2% in Q3, and +2.6% in Q4. On a calendar year basis, U.S. GDP growth is expected to show very strong growth of +5.6% in 2021, but is then expected to decelerate to +3.9% in 2022 and +2.5% in 2023.

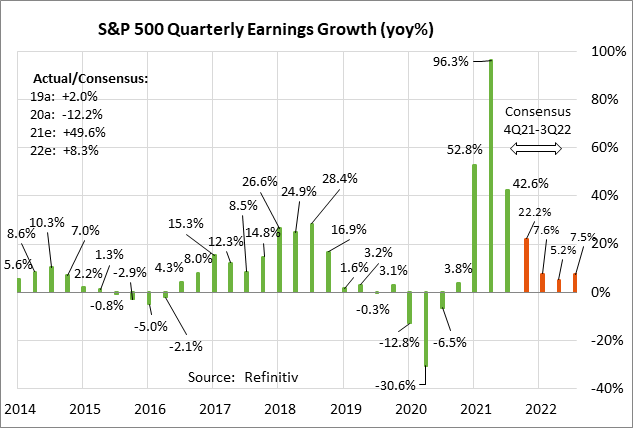

Earnings surge expected to start abating in Q4 — Q4 earnings season is on the horizon in early January. There are 7 of the S&P 500 companies that report earnings this week. Notable reports this week include Nike and Carnival today; General Mills on Tuesday; and Cintas, Carmax, and Paychex on Wednesday.

The consensus is for earnings growth for the S&P 500 companies to decelerate to +22.2% y/y in Q4 from +42.6% in Q3, according to Refinitiv. Earnings growth is then expected to decelerate further to +7.6% y/y in Q1, +5.2% in Q2, and +7.5% in Q3. On a calendar year basis, SPX earnings growth is expected to decelerate to +8.3% in 2022 from +49.6% in 2021.

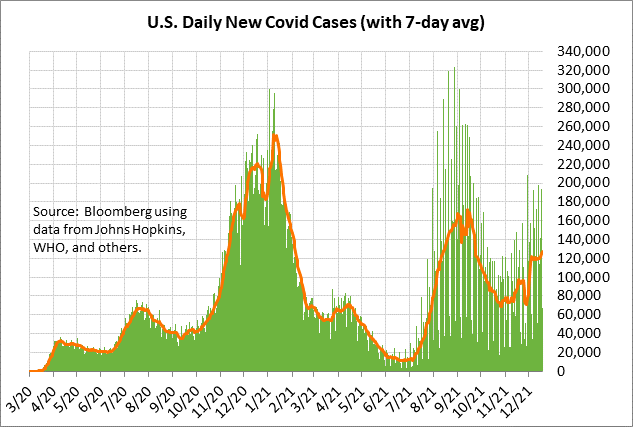

U.S. Covid infection rises to 2-3/4 month high as omicron hits — The 7-day average of new U.S. Covid infections on Saturday rose to a 2-3/4 month high of 127,005. The Covid infection rate is on the upswing as the more-contagious omicron variant spreads in the U.S.

The omicron variant is spreading in Europe and restrictions are being imposed in some areas. The Netherlands on Saturday announced a new lockdown. The UK is also considering new restrictions.

In the U.S., Dr. Fauci on Sunday said, “I don’t foresee the kind of lockdowns that we’ve seen before but I certainly see the potential for stress on our hospital system.”

In some good news, the U.S. vaccination rate continues to climb slowly. Bloomberg reports that 61.4% of the total U.S. population has now been fully vaccinated, and 17.8% have received a booster shot. In the past week, the U.S. has administered a daily average of 1.6 million doses.