- Weekly market focus

- Markets take in stride Fed Chair Powell’s warning that QE tapering is coming this year

- Covid infections last Friday post record 1-day high

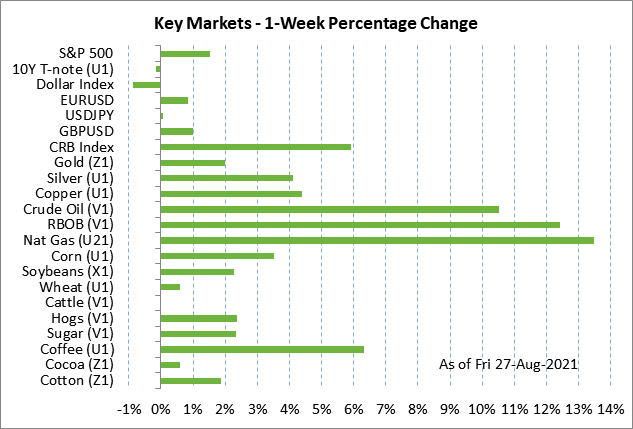

Weekly market focus — The U.S. markets this week will focus on (1) whether the U.S. Covid infection levels continue to worsen, (2) Friday’s payroll report (expected +750,000), (3) further analysis of the timing of the Fed’s QE tapering, (4) oil and gasoline prices as Hurricane Ida on Sunday hit the Louisiana coast with winds stronger than Katrina, and (5) anticipation of the return of Congress later in September when they will need to work on the continuing resolution, debt ceiling hike, $550 billion bipartisan infrastructure bill, and Democrat’s $3.5 trillion spending bill.

China, on Monday night ET time, will release its national Aug manufacturing PMI (expected -0.3 to 50.1 after July’s -0.5 to 50.4) and non-manufacturing PMI (expected -1.3 to 52.0 after July’s -0.2 to 53.3).

Markets take in stride Fed Chair Powell’s warning that QE tapering is coming this year — The markets were generally pleased by Fed Chair Powell’s comments last Friday at the Fed’s Jackson Hole conference. The S&P 500 index closed the day up +0.88%, and the Sep 10-year T-note closed up by 9.5 ticks.

Mr. Powell made clear that QE tapering is most likely coming this year, but he didn’t say anything more hawkish than the markets were expecting. He said that at the last FOMC meeting in late July, “I was of the view, as were most participants, that if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year.”

Mr. Powell indicated that the runway is effectively clear for QE tapering since the Fed believes that the economy has now met the test of “substantial further progress” toward the Fed’s inflation objective and that the labor market has also made “good progress.”

That comment suggested that the QE tapering announcement could come as soon as the next FOMC meeting on Sep 21-22, although the Fed might wait until one of the following meetings on Nov 2-3 or Dec 14-15, depending on how the economy reacts to the pandemic’s resurgence.

Based on last Friday’s market response, the markets now seems to have fully discounted QE tapering this year, and apparently will not react negatively when the actual announcement is made.

The markets were mainly pleased by Mr. Powell’s reassurance last Friday that the Fed’s first rate hike will not come any sooner because QE tapering has started. He said, “The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test.”

He added, “We have said that we will continue to hold the target range for the federal funds rate at its current level until the economy reaches conditions consistent with maximum employment, and inflation has reached 2% and is on track to moderately exceed 2% for some time. We have much ground to cover to reach maximum employment, and time will tell whether we have reached 2% inflation on a sustained basis.”

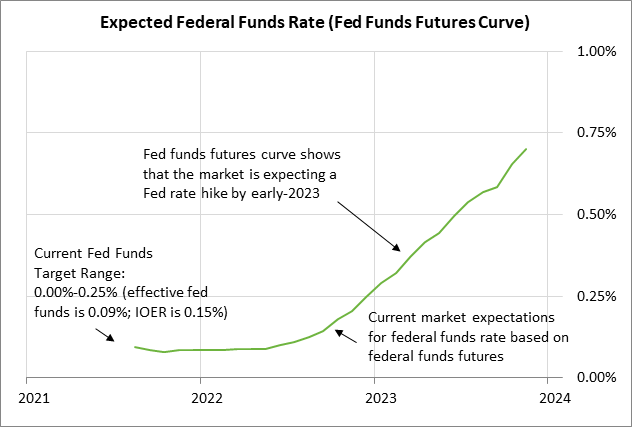

In fact, the federal funds futures curve last Friday turned slightly more dovish on Mr. Powell’s comments by 0.0-0.5 bp for the futures contracts out to mid-2022 and by 1.0-2.5 bp for the futures contracts from mid-2022 to mid-2023.

On inflation, Mr. Powell reiterated his positive market comments by saying that the Fed believes that the current inflation surge is transitory. He said, “The spike in inflation is so far largely the product of a relatively narrow group of goods and services that have been directly affected by the pandemic and the reopening of the economy.”

The markets over the next 3-1/2 weeks leading up to the next FOMC meeting will be listening to how vociferously Fed officials talk about QE tapering to gauge whether the Fed’s official QE tapering announcement is likely at the September 21-22 meeting. If Fed officials continue to step up their QE tapering talk, as they have since the July FOMC meeting, then a tapering announcement could come in just 3-1/2 weeks.

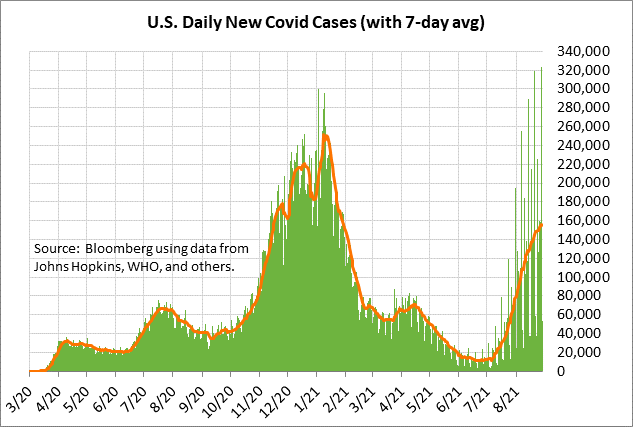

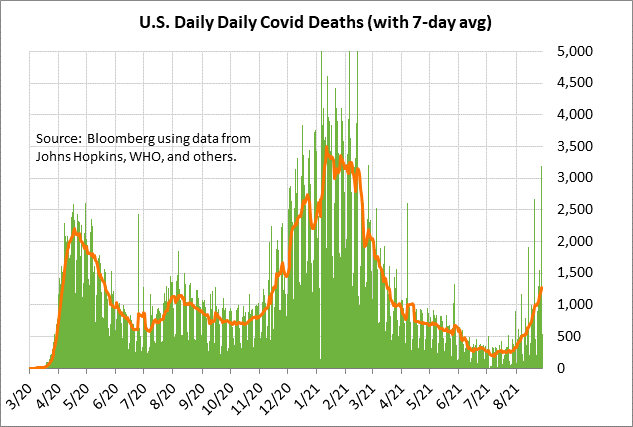

Covid infections last Friday post record 1-day high — The pandemic in the U.S. continues to rage. However, the markets are taking that resurgence in stride, apparently because they believe that most U.S. business sectors have learned to live with the pandemic and will be able to keep their earnings machines humming.

The U.S. last Friday hit a record one-day figure for new Covid infections of 323,403. The 7-day average of new U.S. pandemic statistics reached a new 7-month high of 155,705 last Friday. The 7-day average of Covid deaths last Friday rose to a new 5-month high of 1,265, up from the 16-month low of 185 deaths seen as recently as early July.

There are reports in various parts of the U.S. of a shortage of ICU beds and oxygen. Some areas are starting to reinstitute restrictions, which should help to curb the resurgence.

Also, vaccination levels continue to rise steadily. Bloomberg reports that an average of 886,314 vaccine doses were given the past week, which is much better than the pre-delta level in the 500,000 area. The CDC reports that 52.1% of the total U.S. population has now been vaccinated, and that 61.4% of the U.S. population has received at least one dose.