- U.S. stocks recover on some glimmers of hope for BBB stimulus and tech-stock strength

- Q3 GDP expected unrevised ahead of Q4 surge

- U.S. consumer confidence expected to remain weak

- U.S. existing home sales expected to remain strong

- 5-year TIPS auction

U.S. stocks recover on some glimmers of hope for BBB stimulus and tech-stock strength — The S&P 500 index on Tuesday rallied by +1.78%, more than overcoming Monday’s sharp -1.14% sell-off. The rally was driven in part by strength in tech stocks. The Nasdaq 100 rallied by +2.29% and easily overcame Monday’s loss of -1.10%.

The markets were encouraged by news that President Biden talked with Senator Manchin on the phone on Sunday night after Mr. Manchin rejected the BBB program at his appearance Sunday morning on Fox News. The fact that Biden-Manchin are still talking was a sign that at least some of the BBB program might still be salvaged.

On Monday, the stock market was undercut by worries about slower economic growth if there is no fiscal stimulus from the BBB program in 2022. Goldman Sachs on Monday reduced its Q1-2022 GDP forecast to +2.0% from +3.0% because of its removal of the assumption that the BBB bill would be passed.

Yet, there would be a very long way to go before Mr. Manchin might agree to a new and revised BBB bill, particularly since he has said that he wants the bill to go through the normal committee process. There are also doubts about whether progressives would go along with Mr. Manchin’s demands or whether Arizona Senator Sinema would agree to Mr. Manchin’s desire for corporate tax hikes.

The markets today will be reacting to any news out of last night’s Democratic Senate caucus meeting and whether Mr. Manchin starts to show any flexibility. Senate Majority Leader Schumer has said he will try to put the $1.75 trillion BBB bill on the floor in early 2022 and keep forcing votes on it until something passes.

The stock market also remains very worried about the Covid situation as the omicron variant sweeps the nation and seems likely to cause a massive spike in Covid infections over the next few weeks.

The 7-day average of new U.S. Covid infections on Monday rose to a 3-month high of 140,194, up +17% wk/wk and up +63% just since December 1. The number of new cases on Monday was 253,954, the highest single-day figure since September. Dr. Fauci yesterday said that the omicron variant has extraordinary transmissibility and is doubling every 2-3 days.

Q3 GDP expected unrevised ahead of Q4 surge — The consensus is for today’s Q3 GDP to be unrevised at +2.1% (q/q annualized). Q3 personal consumption is expected to unrevised at its weak level of +1.7%. GDP growth slumped to the weak growth rate of +2.1% in Q3 due to the pandemic’s resurgence and economic obstacles such as supply chain disruptions and labor market shortages.

Looking ahead, GDP in Q4 is expected to surge to +6.0% (q/q annualized). However, GDP growth is then expected to decelerate to +4.0% in Q1-2022, +3.6% in Q2, +3.2% in Q3, and +2.6% in Q4. On a calendar year basis, U.S. GDP growth is expected to show very strong growth of +5.6% in 2021, but is then expected to decelerate to +3.9% in 2022 and +2.5% in 2023.

U.S. consumer confidence expected to remain weak — Today’s Dec Conference Board U.S. consumer confidence index is expected to show a small +1.5 point increase to 111.0, recovering part of November’s -2.1 decline to a 9-month low of 109.5.

U.S. consumers remain in a bad mood despite the strong economy and tight labor market. Consumers are fed up with the pandemic, which is nearly two years old. Consumers are also unhappy about high gasoline prices and the worst inflation in 30 years.

Despite their bad mood, however, consumers are freely spending money and are supporting the economy. Retail sales in November rose by another +0.3% m/m to a record high of $639.8 billion, adding to October’s sharp increase of +1.6%. Even though consumers are in a bad mood, they are still spending a lot of money, which is the important thing for the economy.

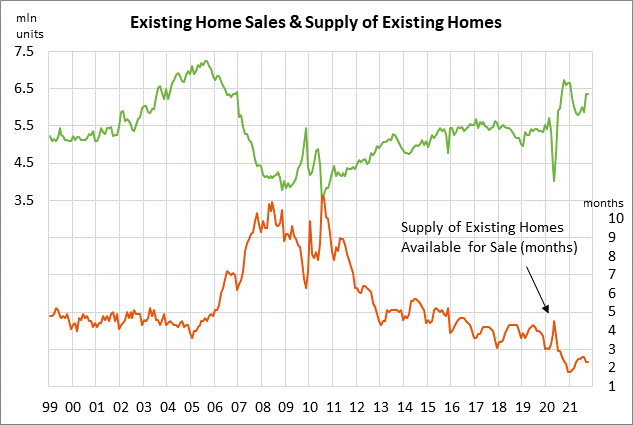

U.S. existing home sales expected to remain strong — The consensus is for today’s Nov existing home sales report to show an increase of +3.0% m/m to 6.53 million, adding to October’s +0.8% increase to 6.34 million. U.S. home sales have backed off from the upward spike seen in late-2020 but remain well above pre-pandemic levels. Demand for homes is still strong due to the pandemic trends of moving into larger homes and moving away from multi-family units. Also, mortgage rates remain extremely low, thus making homes more affordable.

On the negative side, however, the surge in home prices has priced many potential buyers out of the market. The FHFA home price index in September was up +17.7% y/y and was up by +27% from the pre-pandemic level.

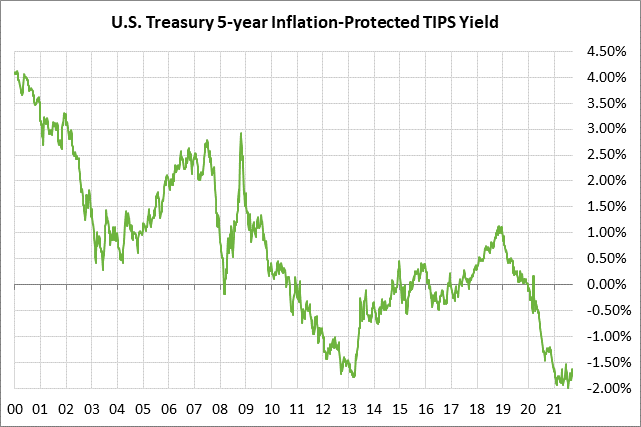

5-year TIPS auction — The Treasury today will sell $17 billion of 5-year TIPS in the second and final reopening of the 1/8% 5-year TIPS of October 2026 that the Treasury first sold in October. The benchmark 5-year TIPS yield yesterday closed at -1.53%. The 12-auction averages for the 5-year TIPS are as follows: 2.66 bid cover ratio, $45 million in non-competitive bids, 5.0 bp tail to the median yield, 22.0 bp tail to the low yield, and 49% taken at the high yield. The 5-year TIPS is the second most popular coupon security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 72.5% of the last twelve 5-year TIPS auctions, well above the median of 63.5% for all recent Treasury coupon auctions.