- FOMC minutes might hint at QE guidance shift for December meeting

- U.S. Q3 GDP expected to be unrevised

- U.S. deflator expected to ease and remain comfortably below Fed’s inflation target

- U.S. personal income and spending expected to fade

- Final-Nov U.S. consumer sentiment expected to be revised slightly lower

- U.S. new home sales expected to remain strong near 14-month high

- U.S. weekly unemployment claims expected to improve

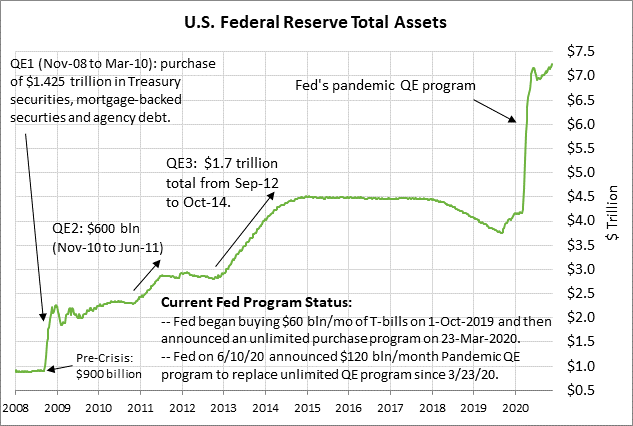

FOMC minutes might hint at QE guidance shift for December meeting — The FOMC today will release the minutes from its last meeting on Nov 4-5. The results of that meeting had little market impact since the FOMC left its key policy variables unchanged and did not shift its guidance. However, Fed Chair Powell in his post-meeting press conference said that FOMC members extensively discussed options for its QE program. That boosted market expectations that the FOMC at its next meeting on Dec 15-16 might at least issue more detailed guidance on its QE program.

There is also speculation that the FOMC might shift some of its Treasury security purchases to the longer-end of the curve to try to keep longer-term Treasury yields low. The market is not currently expecting the FOMC to increase the size of its $120 billion per month QE program, although that is possible if the economy falls into a double-dip recession due to the pandemic surge.

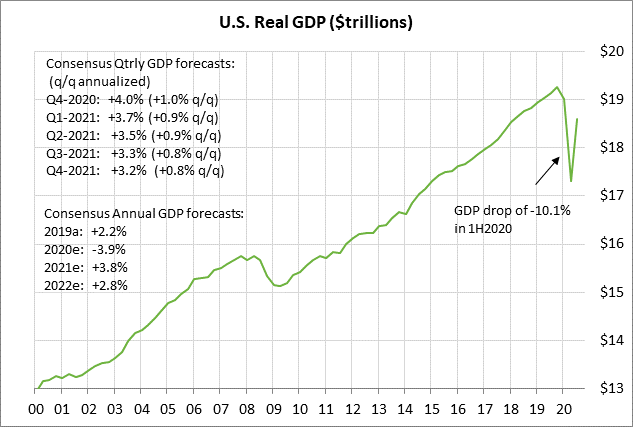

U.S. Q3 GDP expected to be unrevised — The consensus is for today’s Q3 GDP to be left unrevised from the last report of +33.1% (q/q annualized). While the annualized Q3 GDP figure of +33.1% looks impressive, it represents only a partial +7.4% q/q recovery of the -10.1% plunge in the first half of 2020.

The consensus is for modest GDP growth in coming quarters, particularly given the renewed pandemic restrictions that will hurt GDP growth in Q4 and early 2021. The consensus is for GDP growth of only about +1.0% q/q (+4.0% q/q annualized) in Q4 and about +0.8% q/q (+3.2% q/q annualized) in 2021. At that rate, U.S. GDP will not fully regain in 1H2020 loss until either Q3 or Q4 of 2021.

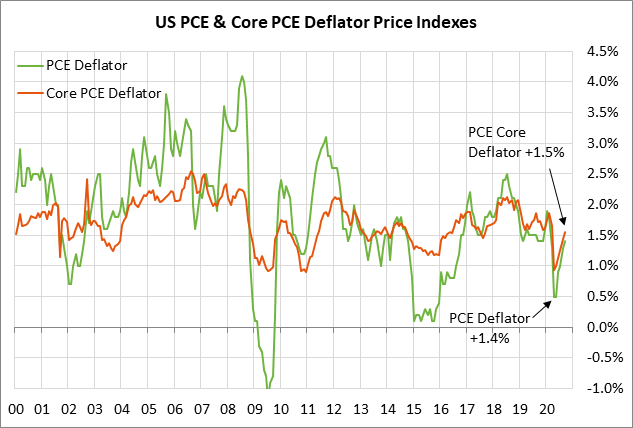

U.S. deflator expected to ease and remain comfortably below Fed’s inflation target — The consensus is for today’s PCE deflator report to show slight declines, illustrating that inflation remains weak and that the Fed’s extraordinary pandemic stimulus policy will continue. The PCE deflator, which is the Fed’s preferred inflation measure, remains comfortably below the Fed’s +2.0% inflation target. The consensus is for today’s Oct PCE deflator to ease to +1.2% y/y from Sep’s +1.4%, and for the core deflator to ease to +1.4% y/y from Sep’s +1.5%.

U.S. personal income and spending expected to fade — The consensus is for today’s Oct personal income and spending reports to weaken from previous levels due to the expiration of stimulus programs and consumer caution due to the pandemic surge. The consensus is for today’s Oct personal income report to show a decline of -0.1% m/m, falling back after Sep’s strong report of +0.9%. The consensus is for today’s Oct personal spending report to show an increase of +0.4%, weaker than Sep’s strong report of +1.4% m/m.

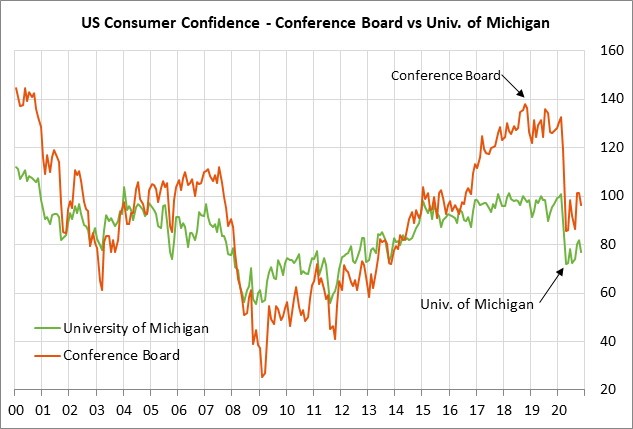

Final-Nov U.S. consumer sentiment expected to be revised slightly lower — The consensus is for today’s final-Nov University of Michigan U.S. Nov consumer sentiment index to be revised slightly lower by -0.2 to 76.8, which would leave the index down by -5.0 points from October rather than the preliminary report of a -4.8 point decline.

U.S. consumer sentiment rose during the 3-month period of Aug-Oct as the economy recovered and as stocks hit new highs. However, consumer sentiment in November started sliding due to the pandemic surge, which has caused states and cities to impose new restrictions and has threatened to cause renewed weakness for the U.S. economy and labor market.

On the brighter side, political uncertainty should soon start to recede as the election results are finalized and the new Congress and president take office in January. Also, positive Covid vaccine news suggests that vaccines will be able to start curbing the pandemic by the latter half of December when vaccinations start to kick into gear.

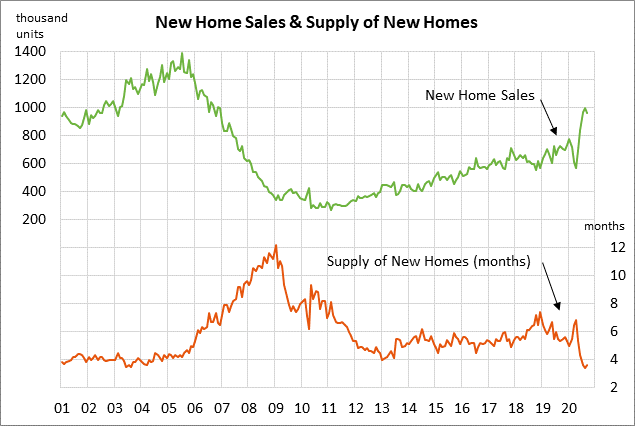

U.S. new home sales expected to remain strong near 14-month high — The consensus is for today’s Oct new home sales report to show a +1.7% increase to 975,000, regaining some ground after Sep’s -3.5% decline to 959,000. New home sales in August surged to a 14-year high of 994,000 units before falling modestly in September. New home sales are stalling because there are so few homes on the market available to buy. The supply of new homes on the market in August fell to a record low of 3.4 months (data since 1963) and recovered just slightly to 3.6 months in September.

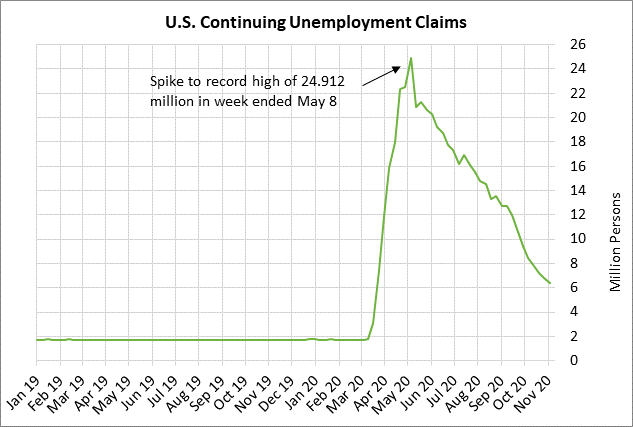

U.S. weekly unemployment claims expected to improve — The consensus is for today’s weekly initial unemployment claims report to show a -14,000 decline to 728,000 following last week’s +31,000 increase to 742,000. Last week’s +31,000 increase was a surprise and was a potential sign of renewed weakness in the U.S. labor market due to increased pandemic restrictions in many parts of the country. Continuing claims today are expected to fall -375,000 to 5.997 million, adding to last week’s -429,000 decline to 6.372 million. Despite the improvement seen in recent months, initial claims are still +525,000 above February’s pre-pandemic level and continuing claims are 4.673 million above their pre-pandemic level.

U.S. durable goods orders expected to show further improvement — The consensus is for today’s Oct durable goods orders report to show an increase of +0.9% and +0.4% ex-transportation, adding to September’s increases of +1.9% m/m and +0.9% m/m ex-transportation. On a year-on-year basis, durable goods orders in September improved to a 7-month high of -1.8% y/y and durable goods orders ex-transportation improved to a 1-1/2 year high of +1.9% y/y.