- Cold snap wreaks havoc with energy markets

- House may vote on pandemic aid bill next Friday

- FOMC minutes may add some color on QE tapering debate

- Jan U.S. PPI expected little changed

- U.S. retail sales expected to improve

- 20-year T-bond auction

Cold snap wreaks havoc with energy markets — The cold snap that extended south into Texas wreaked havoc with the energy markets on Tuesday. As of early Tuesday evening, there were still 3.2 million customers in Texas without power, down by 1 million from the peak. There were also smaller power outages reported in Oklahoma, Louisiana, and Mississippi. Problems with ice also caused power outages in Kentucky, West Virginia, and Virginia.

There were rolling electricity blackouts throughout Texas as power plants of all types were knocked offline. Some natural gas power plants were shut down as natural gas fuel supplies were disrupted. Even coal and nuclear power plants were negatively impacted. Some wind power operations saw curtailment due to ice on the turbine blades. Texas electricity operators do not expect to get back to normal for at least several days.

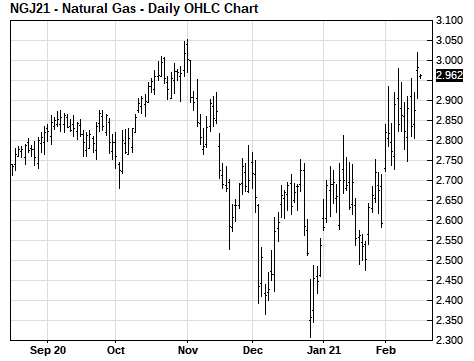

March nat-gas on Tuesday soared by +7.45% due to massive heating demand, combined with supply disruptions due to the cold weather.

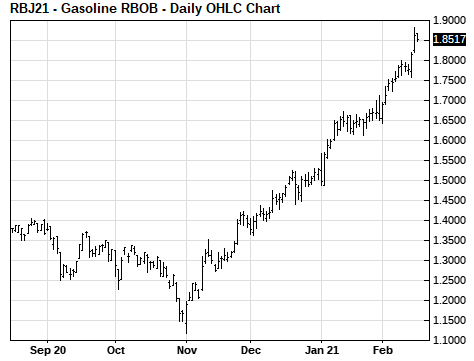

Meanwhile, March WTI crude oil prices on Tuesday rallied by +0.98% as total U.S. oil production fell by a third due to power outages and freeze-ups caused by the cold weather, according to Bloomberg. March gasoline prices soared by +4.75% as some Texas refineries were knocked offline by power outages.

House may vote on pandemic aid bill next Friday — The full House is aiming to vote on the $1.9 trillion pandemic aid bill next Friday (Feb 26), according to reporting by Bloomberg. Bloomberg said that timing was laid out Tuesday by House Majority Leader Steny Hoyer in a Democratic conference call.

The full House and Senate are on recess this week for the Presidents Day holiday, although some Committees will be conducting business.

After the House passes the bill, it will be forwarded to the Senate where it may be slightly revised due to opposition to some elements by one or two Democratic Senators. In that case, it would have to go back to the House for its approval of the Senate’s bill. Democrats are aiming to pass the bill by March 14 when extended unemployment benefits expire.

FOMC minutes may add some color on QE tapering debate — The FOMC today will release the minutes from its Jan 26-27 meeting. The results of that meeting were fully in line with market expectations, and the markets showed little net change on the results.

The T-note market was satisfied with Fed Chair Powell’s attempt at that meeting to assuage the previous concern about QE tapering. He said it would take “some time” to achieve the threshold for considering a tapering of its QE program, suggesting that any such consideration was months away. He also said, “The whole focus on [QE] exit is premature.”

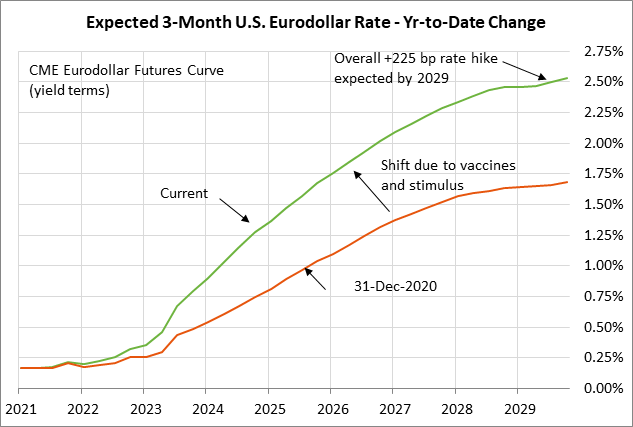

The Eurodollar futures curve on a yield basis has moved sharply higher since the end of 2020 due to (1) expectations for the pandemic to end by year-end thanks to vaccinations, and (2) the massive fiscal stimulus plans by Democrats. The Eurodollar futures curve is now showing expectations for an overall 225 bp Fed rate hike by 2029, which is 75 bp more than expectations as of the end of 2020 for a 150 bp rate hike by 2029.

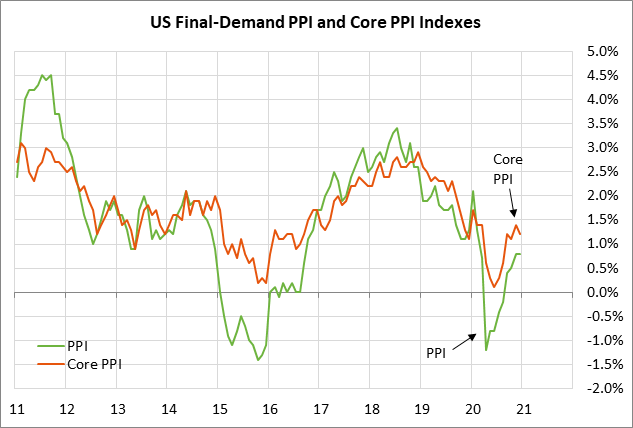

Jan U.S. PPI expected little changed — The consensus is for today’s Jan final-demand PPI to rise slightly to +0.9% y/y from December’s +0.8%. Meanwhile, the Jan core PPI is expected to ease slightly to +1.1% y/y from December’s +1.2%. The current U.S. inflation statistics are sharply below market expectations for inflation. The 10-year breakeven inflation expectations rate on Tuesday climbed to a new 6-1/2 year high of 2.26% and finished the day up +2 bp at 2.25%.

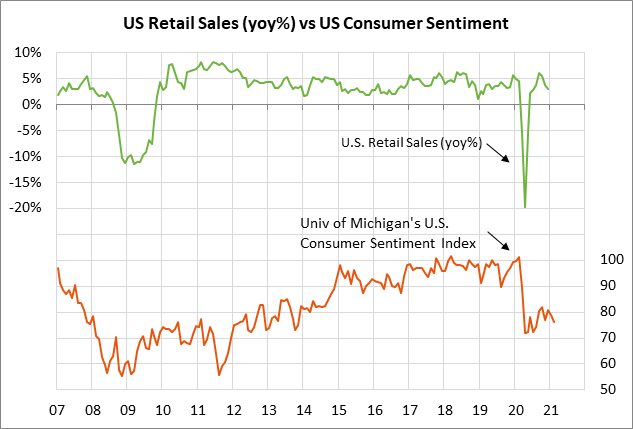

U.S. retail sales expected to improve — Today’s Jan retail sales report is expected to show a solid increase of +1.1% m/m, more than reversing December’s weak report of -0.7% m/m. Consumer sentiment remained poor in January as consumers hunkered down after the holidays. However, consumer sentiment and spending should improve considerably by March due to the declining pandemic infection rates seen since mid-January.

U.S. manufacturing production expected to show another solid rise — The consensus is for today’s Jan manufacturing production report to show an increase of +0.7% m/m, adding to December’s increase of +0.9% m/m. U.S. manufacturing production has risen on a month-on-month basis for eight consecutive months, but is still down -2.8% y/y. Meanwhile, today’ s broader Jan industrial production report is expected to rise +0.5% m/m, adding to December’s increase of +1.6% m/m.

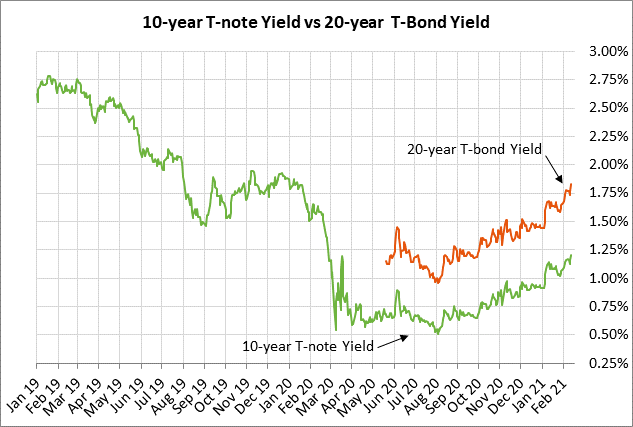

20-year T-bond auction — The Treasury today will auction $27 billion of new 20-year T-bonds. The Treasury just started selling 20-year T-bonds again in May 2020 for the first time since 1986. The 20-year bond yield on Tuesday closed the day sharply higher by +9 bp at a new cyclical high of 1.92%.

The 9-auction averages for the 20-year are as follows: 2.40 bid cover ratio, $2 million in non-competitive bids, 5.8 bp tail to the median yield, 31.8 bp tail to the low yield, and 61.4% taken at the high yield. The 20-year is moderately below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 61.4% of the last nine 20-year auctions, moderately below the median of 63.6% for all recent Treasury coupon auctions.