- Oct U.S. CPI expected to remain strong

- Unemployment claims expected to show continued labor market strength

- 30-year T-bond auction

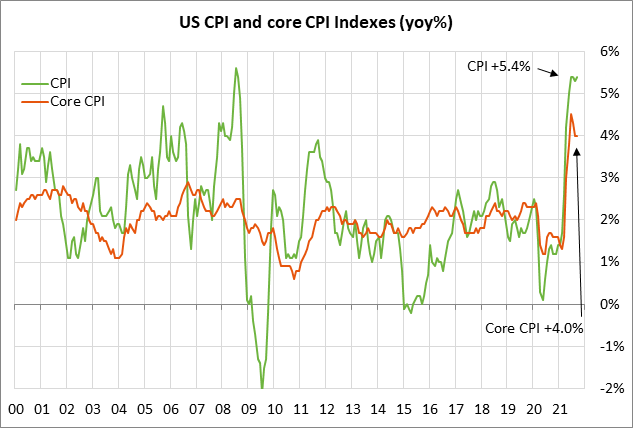

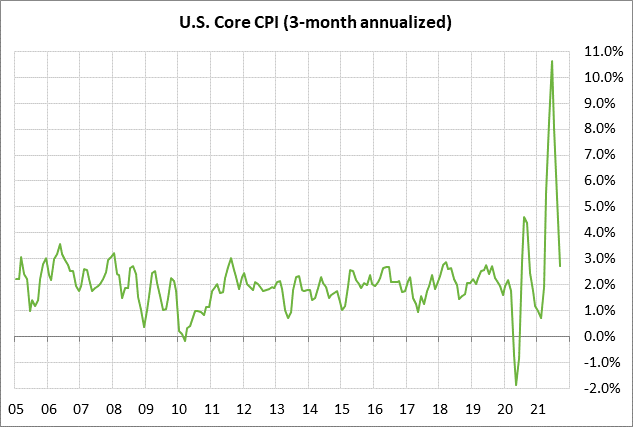

Oct U.S. CPI expected to remain strong — The consensus is for today’s Oct CPI report to show an increase of +0.6% m/m and +5.9% y/y, following Sep’s report of +0.4% m/m and +5.4% y/y. Meanwhile, today’s Oct core CPI is expected to show an increase of +0.4% m/m and +4.3% y/y, following Sep’s report of +0.2% m/m and +4.0% y/y.

U.S. inflation expectations have been rising, but the markets still do not believe that run-away inflation is likely. Fed Chair Powell recently said that supply-chain constraints that have led to elevated inflation “are likely to last longer than previously expected, likely well into next year.” However, he added that “it is still the most likely case” that as those constraints ease, as they eventually will — and as job gains move up — inflation will move back down closer to our 2% goal.”

The markets also expect inflation to ease next year as the economy cools and supply-constraints ease. The general thinking is that the global economy remains in a long-term deflationary trend that will only be temporarily disrupted by pandemic effects. Once the pandemic effects are over, the long-term trend towards modest inflation is likely to re-emerge.

Yet, there is still some uncertainty about whether the current inflation surge might turn into something more persistent and dangerous. Once inflation expectations take root, it is difficult for the Fed to reverse the psychology. The Fed therefore has to be very careful to reassure the markets that it will quickly take action if it appears that inflation expectations become unanchored.

There is a non-zero level of risk that inflation could gain traction and start to get out of control. The Fed has pumped a massive amount of stimulus into the economy over the past 14 years, starting with the global financial crisis in 2007. The global economy did not even have a chance to fully return to normal before the pandemic emerged in early 2020, causing the second massive crisis in just 14 years.

In both the 2007 financial crisis and the pandemic crisis, the Fed responded with zero interest rates and massive amounts of quantitative easing, techniques that had never been tested in modern times by a developed economy. With the quantitative easing process, the Fed buys securities and permanently injects new money into the economy. If that money sits unused, then it doesn’t cause an inflation threat. However, that money is unused rocket fuel that has the potential to explode if it is used to create credit.

The Fed’s QE moves also created a massive amount of liquidity that has boosted asset prices in the securities and real estate markets. QE therefore also creates the threat of asset bubbles, which might eventually burst and cause a new crisis as stock and real estate prices plunge.

The Fed is aware of the risks involved with the massive amount of fiscal and monetary stimulus programs that has been pumped into the U.S. economy in the past 1-1/2 years. The Fed clearly does not want to get into another situation such as the 1970s when the U.S. economy was plagued by high inflation and low economic growth. That high-inflation episode finally required then-Fed Chair Paul Volcker to raise the federal funds rate target as high as 20% in March 1980 as a means to stamp out inflation once and for all.

The Fed knows that the key to preventing another inflation disaster is to act early and keep inflation expectations under control. The Fed is currently reassuring the markets that it is not planning to raise interest rates any time soon. However, the Fed will quickly change its tune and start raising interest rates if it appears that inflation is beginning to reach escape velocity.

Indeed, the markets as of this past summer were not expecting the Fed’s first rate hike until early 2023. However, the markets are now discounting a strong chance of two rate hikes by the end of 2022. The markets will continue to watch the incoming inflation statistics very carefully to see if they start to raise red flags for the Fed.

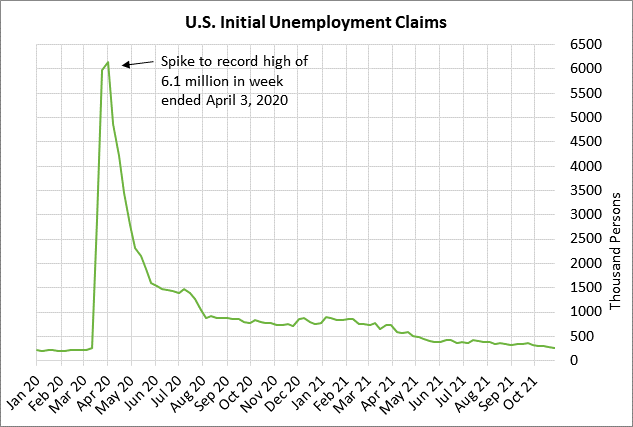

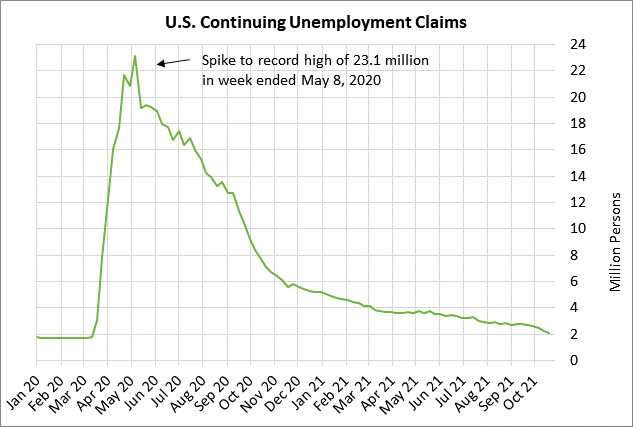

Unemployment claims expected to show continued labor market strength — The consensus is for today’s weekly initial unemployment claims report to show a -9,000 decline to 260,000, adding to last week’s decline of -14,000 to 269,000. Initial claims last week fell to a 19-month low.

Today’s continuing claims report is expected to show a -55,000 decline to 2.050 million, adding to last week’s -134,000 decline to 2.105 million. Continuing claims are in strong shape as the series last week fell to a 19-month low.

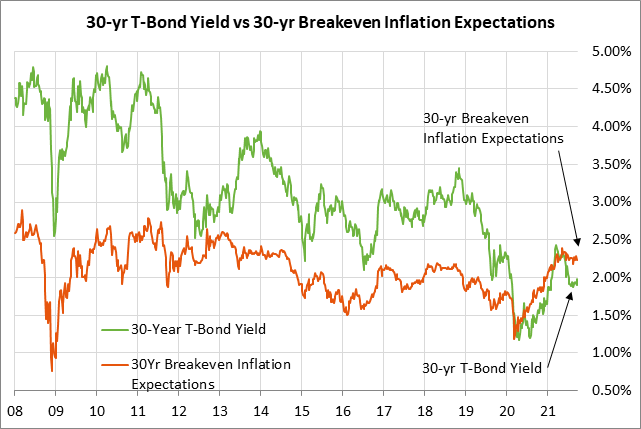

30-year T-bond auction — The Treasury today will sell $25 billion of new 30-year T-bonds, concluding this week’s quarterly refunding operation. The benchmark 30-year T-bond yield yesterday closed at 1.831%.

The 12-auction averages for the 30-year are as follows: 2.33 bid cover ratio, $6 million in non-competitive bids, 6.5 bp tail to the median yield, 79.8 bp tail to the low yield, and 54% taken at