- Powell downplays inflation worries

- Schumer-Pelosi to meet today with White House officials on infrastructure

- U.S. new home sales expected to show a small gain

- Markit U.S. PMIs expected to fade slightly

- Q1 current account deficit expected to widen sharply

- 5-year T-note auction

Powell downplays inflation worries — The markets were pleased by Fed Chair Powell’s comments yesterday in which he insisted that the current inflation surge is transitory and that the Fed will not raise interest rates preemptively. At the same time, Mr. Powell said the Fed would not let inflation get out of control.

Mr. Powell said, “A pretty substantial part, or perhaps all of the overshoot in inflation comes from categories that are directly affected by the re-opening of the economy such as used cars and trucks.” Those are things that we would look to stop going up and ultimately start to decline.” He added, “We will not raise interest rates preemptively because we think employment is too high, because we feared the possible onset of inflation. We will wait for evidence of actual inflation or other imbalances.”

However, Mr. Powell also said, “I will say that these [inflation] effects have been larger than we expected and they may turn out to be more persistent than we expected.” He also mentioned that a 5% inflation environment wouldn’t be acceptable.

Schumer-Pelosi to meet today with White House officials on infrastructure — House Speaker Pelosi and Senate Majority Leader Schumer will meet today with White House officials on the infrastructure agenda. Mr. Schumer says he is still on the two-track process of seeing how bipartisan talks pan out while also seeking to approve the budget resolution necessary to kick-start the process of passing a Democratic-only infrastructure bill with budget reconciliation.

Meanwhile, White House officials yesterday met with some members of the 21-member bipartisan group of Senators that are pursuing a infrastructure bill. However, there were no reports of any progress from that meeting. The seemingly impossible hurdle continues to be pay-fors.

Time is running out for the bipartisan infrastructure talks since the Senate is scheduled to leave this Thursday for its 2-week Fourth of July recess. After their July 4th recess, the Senate will be in session for only four weeks (July 12 to Aug 6) before leaving for their month-long August recess (Aug 7 to Sep 10). The House has a similarly light legislative schedule through September.

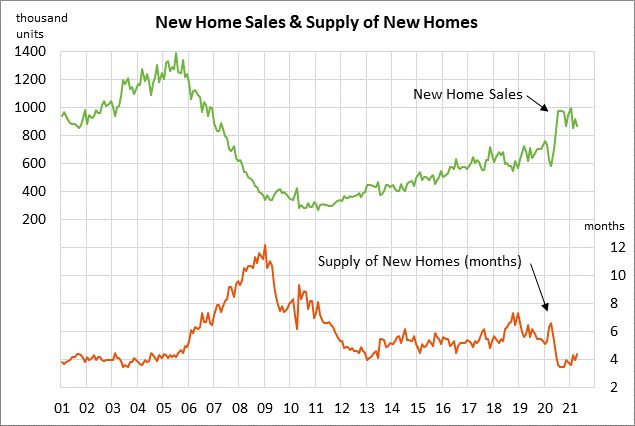

U.S. new home sales expected to show a small gain — The consensus is for today’s May new home sales report to show an increase of +0.4% m/m to 867,000, recovering a bit after April’s sharp -5.9% drop to 863,000.

New home sales rose to a 14-year high of 993,000 in January on strong pandemic-related demand. However, new home sales have since fallen by a net -13% to 863,000 in April due to the small number of homes on the market and the surge in new home prices. The median price of a new home in April was $372,400, which was just slightly below January’s record high of $373,200 and was up +20% year-on-year.

Markit U.S. PMIs expected to fade slightly — The consensus is for today’s June Markit U.S. manufacturing PMI to fall by -0.6 points to 61.5, reversing May’s +0.6 increase to 62.1. Meanwhile, today’s June Markit U.S. services PMI is expected to fall slightly by -0.4 points to 70.0, giving back a little of May’s +5.7 point surge to 70.4.

The PMIs are both at high levels that indicate strong business optimism as the pandemic fades and the economy surges. However, business optimism is being tempered by supply-chain constraints, high input prices, sporadic labor shortages in some industries, and the knowledge that higher interest rates are coming down the road.

Q1 current account deficit expected to widen sharply — The consensus is for today’s Q1 current account deficit to widen to -$206.20 billion from -$188.48 billion in Q4. The deficit was already at a 10-year high in Q4 and is expected to widen further to -$206 billion, although that would remain below the record high of -$218 billion posted in Q3-2006. The deficit has widening mainly because imports have recovered much faster than exports because of the surge in the U.S. economy tied to the massive amount of fiscal stimulus. Meanwhile, exports have been held back by comparatively slower economic growth overseas.

5-year T-note auction — The Treasury today will sell $61 billion of 5-year T-notes and $26 billion of 2-year floating-rate notes. The Treasury will then conclude this week’s $209 billion T-note package by selling $62 billion of 7-year T-notes on Thursday.

The 5-year T-note yield yesterday closed at 0.86%, near the middle of the narrow range seen since March. The 5-year yield is up by 8 bp from the 0.78% level seen last week before Wednesday’s hawkish outcome of the FOMC meeting.

The 12-auction averages for the 5-year are as follows: 2.42 bid cover ratio, $24 million of non-competitive bids, 4.7 bp tail to the median yield, 21.7 bp tail to the low yield, and 47% taken at the high yield. The 5-year is mildly below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buying, have taken an average of 60.2% of the last twelve 5-year T-note auctions, mildly below the median of 61.2% for all recent Treasury coupon auctions.