- Weekly global market focus

- Markets brace for possible QE tapering talks at FOMC meeting in two weeks

- Time is running out for bipartisan talks on Biden job and family proposal

- Q1 earnings season trickles to a close

- U.S. ISM manufacturing index expected to remain strong

Weekly global market focus — The U.S. markets this week will focus on (1) whether the FOMC at its meeting in two weeks (June 15-16) will begin talks on QE tapering, (2) any progress this week on President Biden’s $4 trillion jobs and family plan, (3) the fading pandemic statistics, (4) any news out this Friday’s in-person G-7 meeting in London among finance ministers and central bank chiefs, and (5) whether this Friday’s May payroll report shows the expected improvement after April’s disappointing report of +266,000.

In Europe, the markets will focus on comments by ECB officials ahead of the next Thursday’s (June 10) ECB meeting. The markets will be watching today’s May Eurozone CPI to see there is an uptick due to global supply chain issues.

Markets brace for possible QE tapering talks at FOMC meeting in two weeks — The markets were surprised to hear from the April 27-28 FOMC meeting minutes, released on May 19, that “a number” of FOMC members suggested that discussions might have to begin at some point on QE tapering. The minutes suggested that the talks about QE tapering could begin as soon as the next FOMC meeting in two weeks (June 15-16) or by the following meeting on July 27-28.

Even if the FOMC starts talking about QE tapering, however, that does not mean an announcement would be imminent. Indeed, the FOMC is likely to signal its QE tapering decision well in advance as the Fed tries to avoid another “taper tantrum” such as the one seen in 2013 when Treasury yields spiked higher on then-Fed Chair Bernanke’s surprise mention of QE tapering.

A survey taken by Bloomberg several weeks ago found that 14% of the analysts surveyed expect the Fed to start tapering its QE program in Q3, and 45% of the analysts expect tapering to begin in Q4. That means that 41% of the respondents do not expect the Fed to start tapering until 2022.

Opportunities for the Fed to announce the tapering could come at the July or September FOMC meetings or at the Fed’s late-August Jackson Hole conference.

The markets are still not expecting the Fed’s first rate hike until early 2023, according to the federal funds futures market and the 3-month Eurodollar futures market.

Time is running out for bipartisan talks on Biden job and family proposal — The bipartisan talks on President Biden’s infrastructure/jobs proposal have not made much progress in the past several weeks and the two sides seem impossibly far apart. The program sizes remain far apart but more importantly Republicans have drawn a red line against any increase in corporate taxes. By contrast, President Biden plans to pay for his infrastructure/jobs program with a hike in the corporate tax rate and a minimum global corporate tax rate.

President Biden’s informal deadline of Memorial Day for bipartisan negotiations to show progress has now passed. Mr. Biden may soon sideline the bipartisan talks and allow House Speaker Pelosi to move ahead with House legislation. Ms. Pelosi needs to move quickly if she expects to meet her goal of getting the House to pass the infrastructure/jobs bill by the 4th of July. Senate Majority Leader Schumer last week said he expects the Senate to work on the infrastructure bill in July.

Q1 earnings season trickles to a close — Q1 earnings season is trickling to a close, with only 9 of the S&P companies reporting this week. Notable reports this week include Constellation Brands and HP Enterprise today; Advance Auto Parts and NetApp on Wednesday; and Cooper Cos and Broadcom on Thursday.

The consensus is for S&P 500 earnings in Q1 to show a very strong gain of +52.8% y/y, according to Refinitiv. Q1 earnings have been much stronger than expected. The current Q1 earnings estimate of +52.8% is far better than expectations of +24.2% that were seen as recently as April 1.

Looking ahead, the consensus is for even stronger S&P 500 earnings growth in Q2 of +62.2%, then easing to +23.7% in Q3 and +16.4% in Q4. On a calendar year basis, the consensus is for strong +35.6% earnings growth in 2021, overcoming the -12.2% decline seen in 2020.

U.S. ISM manufacturing index expected to remain strong — The consensus is for today’s May ISM manufacturing index to show a +0.1 increase to 60.8, regaining a little ground after April’s sharp drop of -4.0 to 60.7.

April’s ISM level of 60.7 was still high and indicated that U.S. manufacturing executives remain very optimistic about the prospects for the U.S. manufacturing sector as the pandemic fades.

However, manufacturing confidence fell back in April as executives recognized that the pandemic is not over and will continue to cause disruptions, particularly overseas where vaccinations have not progressed as far as in the U.S. In addition, the manufacturing sector is grappling with a host of bottleneck and supply chain disruptions, the worst of which is the chip shortage. Those disruptions have forced cutbacks in production for some industries despite strong demand.

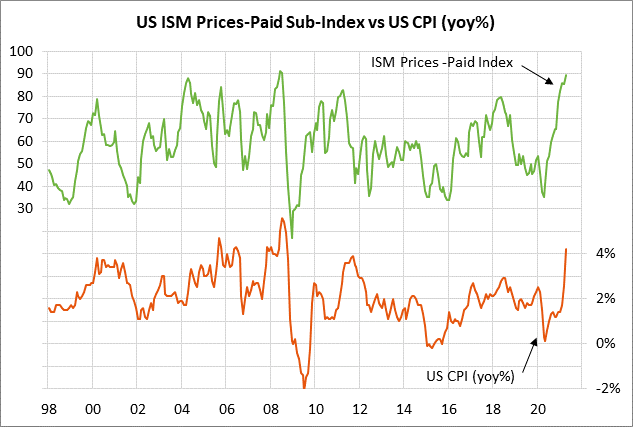

The markets will be carefully watching today’s May ISM prices-paid sub-index for a reading on the price surge being caused by strong demand and supply chain disruptions. The ISM prices-paid sub-index in May surged by +4.0 points to a 13-year high of 89.6.