- 10-year T-note yield reaches new 1-year highÂ

- House set to approve $1.9 trillion pandemic aid package on Friday

- Q4 GDP expected to be revised slightly higher

- U.S. unemployment claims expected to show continued improvement in the labor market

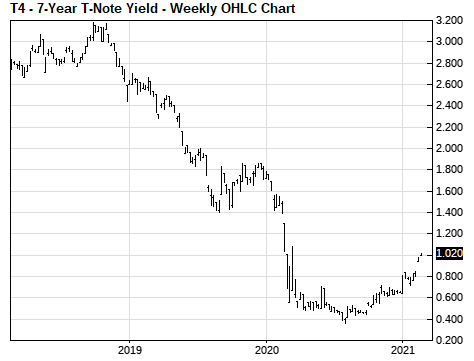

- 7-year T-note auction to yield near 1.00%

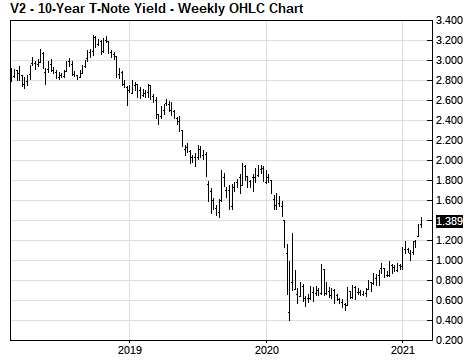

10-year T-note yield reaches new 1-year high — The 10-year T-note yield on Wednesday reached a new 1-year high of 1.43% and closed the day up +3 bp at 1.38%.

The 10-year T-note yield rose after Fed Chair Powell on Tuesday showed no real concern about the rise in longer-term Treasury yields. He said, “In a way, it’s a statement of confidence on the part of markets that we will have a robust and ultimately complete recovery.”

As recently as late last year, the markets were debating whether the Fed might step in to cap any rise in the 10-year T-note yield above 1.00%. Now, the 10-year yield has surged to a 1-year high of 1.43%, and the Fed hasn’t even issued any verbal opposition.

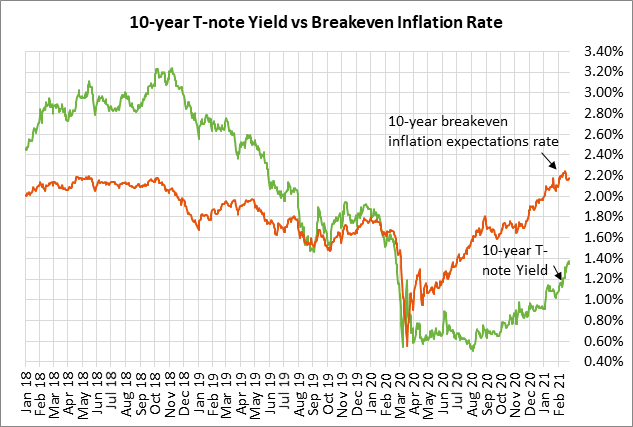

The 10-year T-note yield has risen sharply by a total of +52 bp, just since the end of 2020. That rise has been due to (1) the emergence of effective Covid vaccines that could end the pandemic by the end of 2021, (2) the massive amount of stimulus passed by Congress, with more on the way, and (3) the sharp rise in inflation expectations.

Congress is expected to pass the new $1.9 trillion pandemic aid bill by mid-March. After that, Democrats plan to pass a large infrastructure and clean-energy spending bill.

That massive amount of fiscal stimulus, combined with the Fed’s extraordinarily easy monetary policy, has pushed inflation expectations sharply higher. The sharp rise in crude oil prices seen in recent months has sharply increased inflation expectations.

The 10-year breakeven inflation expectations rate is currently at 2.17%, which is just 9 bp below the mid-Feb 6-1/2 year high of 2.26%. The breakeven rate has more than recovered from the spring-2020 pandemic plunge and is actually +38 bp higher than the pre-pandemic level of 1.79%.

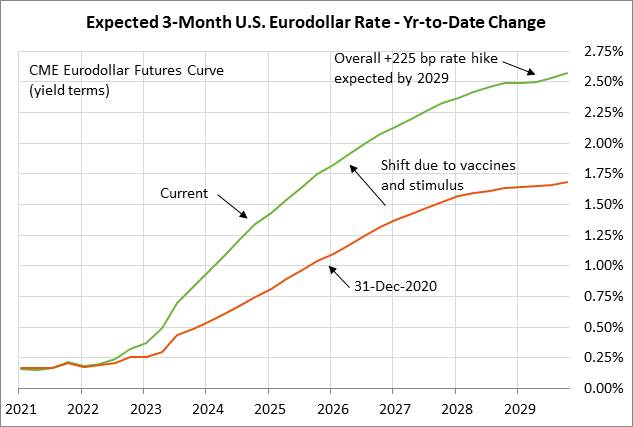

The Eurodollar futures curve on Wednesday was little changed after Fed Chair Powell finished his second day of semi-annual testimony to Congress. Mr. Powell said nothing new and reiterated his recent themes.

The markets are currently expecting the Fed’s first +25 bp rate hike by early-2023 and are expecting an overall +225 bp rate hike by early 2029, according to the Eurodollar futures curve.

House set to approve $1.9 trillion pandemic aid package on Friday — The House is expected to approve President Biden’s $1.9 trillion pandemic aid bill on Friday. The Senate will then consider the bill, and will likely make some changes that would require the House to pass the revised version. Democratic leaders have promised to get the bill passed before unemployment benefits start running out on March 14.

The pandemic aid bill still needs some adjustment because it currently exceeds $1.9 trillion, in violation of the Senate’s budget reconciliation rules. In addition, the Senate parliamentarian, or a Democratic Senator, may strip out the minimum wage hike to $15 per hour. In the end, however, the bill is likely to be near $1.9 trillion and will provide substantial additional stimulus to the economy in the coming months.

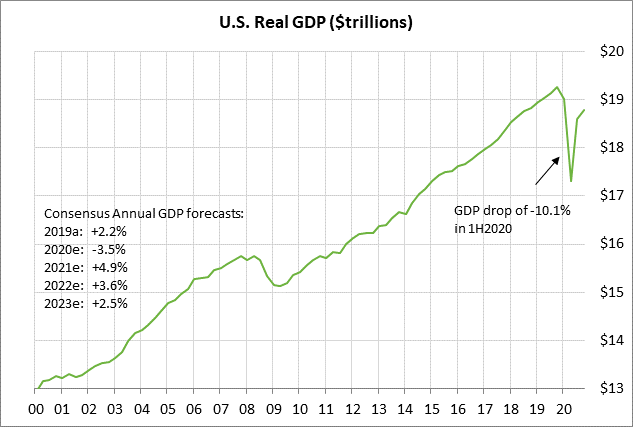

Q4 GDP expected to be revised slightly higher — The consensus is for today’s Q4 GDP report to be revised slightly higher to +4.2% (q/q annualized) from the last report of +4.0%. GDP has so far recovered about three-quarters of the -10.1% plunge seen in Q2-Q3 2020 due to the pandemic shutdowns. Based on current forecasts, the U.S. economy will not fully recover to its pre-pandemic GDP peak until the third quarter of 2021.

The good news is that GDP forecasts for 2021 have been boosted due to the new $1.9 trillion round of pandemic aid that is expected to be approved by Congress by mid-March. The consensus is for a strong GDP rise of +4.9% in 2021, which would overcome the -3.5% drop in 2020. GDP is then expected to ease to more normal levels of +3.6% in 2022 and +2.5% in 2023.

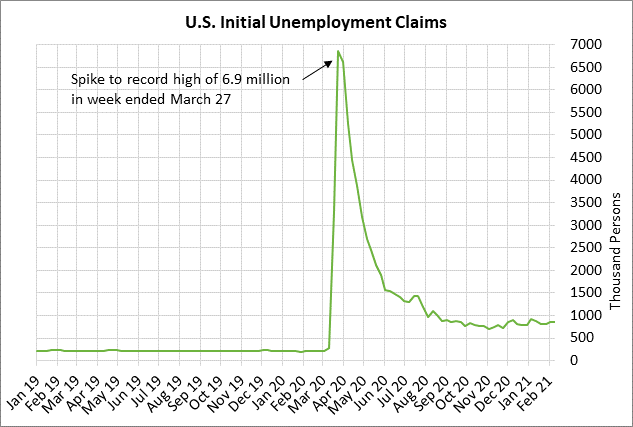

U.S. unemployment claims expected to show continued improvement in the labor market — The market is expecting today’s unemployment report to show some continued slow improvement in the U.S. labor market. That improvement could accelerate over the new few months as restrictions are lifted due to the sharp drop in new Covid infections.

The consensus is for today’s weekly initial unemployment claims report to show a decline of -36,000 to 825,000, more than reversing last week’s +13,000 rise to 861,000. Today’s continuing claims report is expected to show a decline of -34,000 to 4.460 million, adding to last week’s decline of -64,000 to 4.494 million. From the pre-pandemic levels seen in late-February, initial claims are still up by +644,000 and continuing claims are up by 2.795 million.

7-year T-note auction to yield near 1.00% — The Treasury today will sell $62 billion of 7-year T-notes, concluding this week’s $209 billion T-note package. The 7-year T-note yield on Wednesday rose to a new 1-year high of 1.05% and closed the day +4 bp at 1.00%. The 7-year T-note yield this year has risen sharply by +41 bp from the 0.64% level seen at the end of 2020.

The 12-auction averages for the 7-year are: 2.45 bid cover ratio, $5 million in non-competitive bids, 5.2 bp tail to the median yield, 37.7 bp tail to the low yield, 45% at the high yield, and 63.6% taken by indirect bidders (matching the 63.6% median for all recent coupon auctions).