- Fed Chair Powell seems content with recent T-note yield surge

- Senate parliamentarian may rule today on minimum wage hike and other contentious issues in pandemic aid bill

- U.S. new home sales expected to show a modest riseÂ

- 5-year T-note auction to yield near 0.57%

Fed Chair Powell seems content with recent T-note yield surge — Anyone who hoped that Fed Chair Powell yesterday might voice disapproval of the recent surge in long-term Treasury yields was disappointed. Instead, Mr. Powell, commenting on the rise in bond yields, said, “In a way, it’s a statement of confidence on the part of markets that we will have a robust and ultimately complete recovery.”

However, Mr. Powell on Tuesday did soothe the T-note market by reiterating that the Fed is not even thinking about trimming its QE program. As long as the QE program is safe, and the market is assured the Fed will not raise interest rates for at least a year, then the T-note market doesn’t have much reason to push yields much higher except for inflation concerns.

Even on the inflation front, the markets do not have any huge worries due to the large amount of slack in the economy and the big hole in the labor market, which is still down by 10 million jobs from the pre-pandemic high.

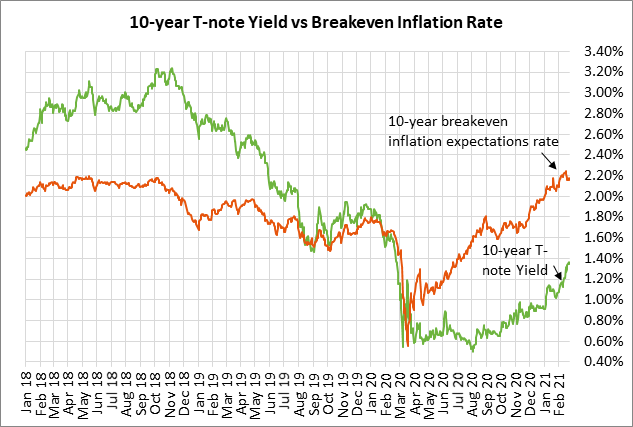

The 10-year breakeven inflation expectations rate has risen sharply to the current level of 2.17%, which is mildly above the Fed’s 2.0% inflation target. The breakeven rate has risen above 2% mainly because of the sharp rise in oil prices and fears that the economy may start running hot by 2022 due to massive fiscal stimulus efforts. However, there is no guarantee that inflation will show the expected surge. Indeed, Fed Chair Powell yesterday said, “I really don’t expect that we’ll be in a situation where inflation rises to troubling levels.”

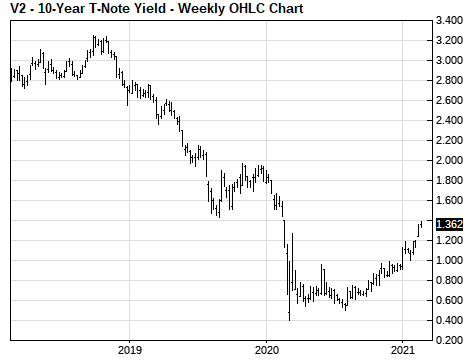

The 10-year T-note yield has risen sharply by +43 bp so far this year to 1.34%, closing just below Monday’s 1-year high of 1.39%. While that 43 bp rise is a big move, the 10-year T-note yield is still 58 bp below the pre-pandemic level of 1.92% seen at the end of 2019.

The sharp rise in the 10-year T-note yield seen from the mid-2020 low of 0.50% has mainly been due to the massive fiscal stimulus passed by Congress and the advent of effective vaccines that hold the potential to end the pandemic within a matter of months. The sharp rise in inflation expectations has also been behind the rise in T-note yields.

Mr. Powell today will appear before the House Financial Services Committee to present the same written testimony that he gave yesterday to the Senate Banking Committee. However, Mr. Powell will answer different questions today, which means he could say something new that moves the markets.

The stock market yesterday was pleased with Mr. Powell’s reassurance that there will be no near-term end to the Fed’s near-zero funds rate target or the Fed’s $120 billion QE program. The S&P 500 index was down sharply by -1.8% on its early low, but then recovered after Mr. Powell’s comments and closed the day slightly higher by +0.13%.

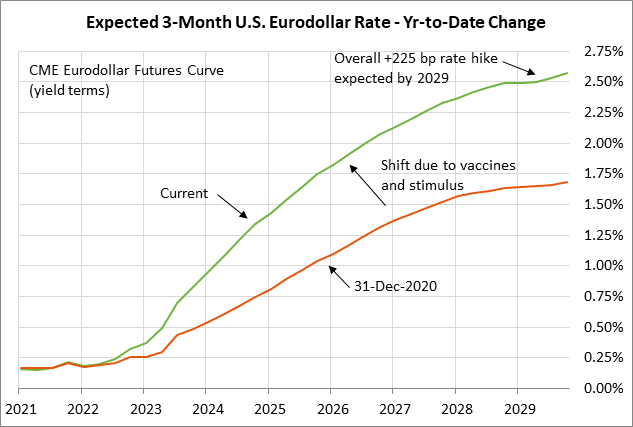

The Eurodollar futures curve on a yield basis on Tuesday turned slightly more dovish by 2-3 bp following Mr. Powell’s remarks. The markets are currently expecting the Fed’s first +25 bp rate hike by early-2023 and are expecting an overall +225 bp rate hike by early 2029, according to the Eurodollar futures curve.

Senate parliamentarian may rule today on minimum wage hike and other contentious issues in pandemic aid bill — Chair of the Senate Budget Committee Bernie Sanders said yesterday that the Senate parliamentarian may rule as soon as today on whether the Senate can include the minimum wage hike in the pandemic aid bill under the budget reconciliation rules. The Senate can override that ruling by a majority vote, but that seems unlikely since Democratic Senator Manchin has said he won’t vote to overrule any rulings by the Senate parliamentarian.

A ruling against the minimum wage hike might be disappointing to some on a policy basis, but it may be favorable for the markets since (1) corporations won’t be saddled with higher labor costs, and (2) it could make passage of the pandemic bill easier since it would avoid a fight with the one or two Democratic Senators who oppose a hike in the minimum wage to as high as $15 per hour.

The House is expected to pass the $1.9 trillion pandemic aid bill on Friday. The Senate will then consider the bill, and might make some changes that would require the House to pass the revised version. Democratic leaders have promised to get the bill passed before unemployment benefits start running out on March 14.

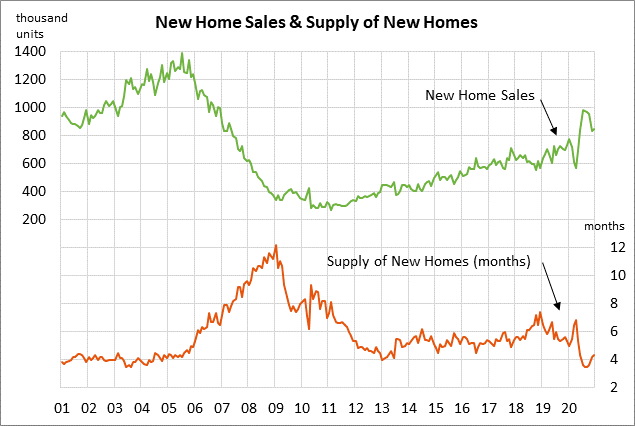

U.S. new home sales expected to show a modest rise — The consensus is for today’s Jan new home sales report to show an increase of +1.5% to 855,000, adding to Dec’s +1.6% increase to 842,000. New home sales have fallen off in recent months and are now down by -14% from the July-2020 14-year high of 979,000 units.

5-year T-note auction to yield near 0.57% — The Treasury today will sell $61 billion of 5-year T-notes and $26 billion of 2-year floating-rate notes. The Treasury will then conclude this week’s $209 billion T-note package by selling $62 billion of 7-year T-notes on Thursday. The 5-year T-note yield yesterday closed at 0.566%, just mildly below Monday’s 1-year high of 0.615%.

The 12-auction averages for the 5-year are: 2.34 bid cover ratio, $19 million in non-competitive bids, 4.6 bp tail to the median yield, 22.2 bp tail to the low yield, 36% at the high yield, and 59.7% taken by indirect bidders (well below the 63.6% median for all recent coupon auctions).