- Fed Chair Powell expected to reiterate recent themes

- House expected to approve pandemic aid bill by week’s end

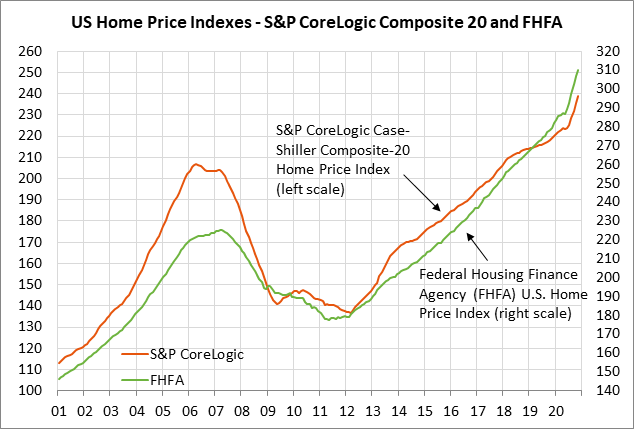

- U.S. home prices expected to show another sharp increase

- U.S. consumer confidence expected to edge higher

- 2-year T-note auction to yield near 0.11%

Fed Chair Powell expected to reiterate recent themes — Fed Chair Powell today, in his semi-annual testimony to the Senate Banking Committee, is expected to largely reiterate the Fed’s recent themes. Mr. Powell will repeat his written testimony tomorrow before the House Financial Services Committee, although he will answer different questions.

Mr. Powell today is likely to reiterate the Fed’s recent theme that it is too early to even talk about tapering the QE program. Mr. Powell is instead expected to stress that the labor market has a long way to go before returning to normal.

Mr. Powell might also be called upon to address the recent surge in longer-term Treasury yields. The 10-year T-note yield yesterday rose to a new 1-year high of 1.39%. The Fed might be worried that longer-term Treasury yields are rising too quickly and might present a threat to the recovery. In fact, ECB President Lagarde yesterday said that the ECB is “closely monitoring” bond yields, implying that the ECB might be willing to take some action to cap bond yields if the rise continues.

Mr. Powell will be called upon to say whether he believes the U.S. economy needs another $1.9 trillion of fiscal stimulus. In the past, Mr. Powell has been supportive of fiscal stimulus to spark a recovery and provide aid where the Fed cannot. However, with the end of the pandemic possibly in sight, Mr. Powell may be less enthusiastic about more stimulus.

Mr. Powell may also be asked again if he would like to stay on as Fed Chair when his term expires in February 2022. Mr. Powell recently implicitly addressed that issue by saying that he loves his job. A recent survey by Bloomberg found that almost three-quarters of the respondents expect President Biden to reappoint Mr. Powell to a new term as Fed Chair. Separately, President Biden currently has one Fed Governor seat to fill after the Senate refused to confirm Trump-nominee Judy Shelton during its last term.

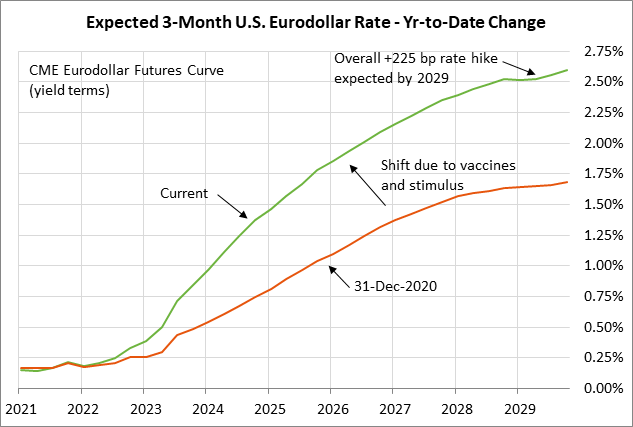

The markets have accelerated expectations for when the Fed will implement its first rate hike. The market is now expecting the Fed’s first +25 bp rate hike by early-2023, sooner than expectations of late-2023 that were seen at the end of 2020, according to the Eurodollar futures market. Also, the market is now expecting an overall +225 bp rate hike by early 2029, which is 75 bp more than the 150 bp rate hike that was expected as of the end of 2020.

House expected to approve pandemic aid bill by week’s end — The House Budget Committee yesterday approved the $1.9 trillion pandemic aid bill and passed it along to the House Rules Committee for consideration today. The bill will then go to the House floor for a vote, possibly by Friday or this weekend.

The Senate will then consider the bill, which could be trimmed somewhat due to opposition to some items by at least one Democratic Senator. The Senate Parliamentarian will also have to rule on whether everything in the bill qualifies for consideration under the special budget reconciliation rules. There are some doubts about whether the Senate Parliamentarian will approve the proposed minimum wage hike to $15 per hour.

The Senate is likely to make some minor changes to the bill, which means it would then have to go back to the House for its approval of the Senate’s changes. Democratic leaders have promised to get the bill passed before unemployment benefits start running out on March 14.

U.S. home prices expected to show another sharp increase — The consensus is that U.S. home prices increased sharply again in December due to the combination of strong demand and tight supply. U.S. existing home sales are up +24% from pre-pandemic levels and are just mildly below last November’s 15-year high. Meanwhile, the supply of homes on the market is at a record low of 1.8 months.

The consensus is for today’s Dec FHFA index to rise +1.0% m/m (after Nov’s +1.0%) and Dec S&P CoreLogic composite-20 index to rise 1.2% m/m (after Nov’s +1.4%). The composite-20 index was up sharply by +9.1% y/y in November.

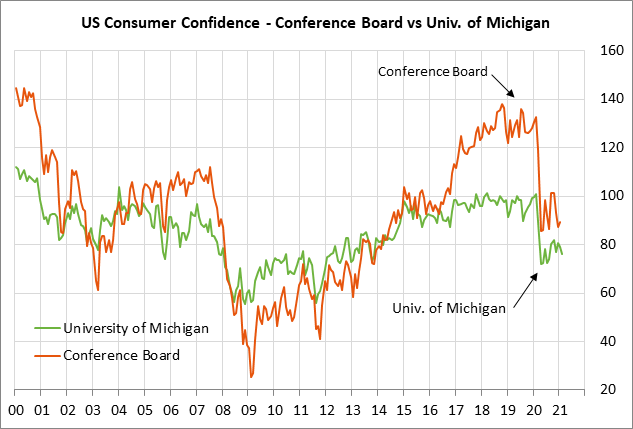

U.S. consumer confidence expected to edge higher — The consensus is for today’s Feb Conference Board U.S. consumer confidence index to show a small increase of +0.7 to 90.0, adding to January’s +2.2 point increase to 89.3. However, in a bad omen for today’s report, the University of Michigan has already reported that its consumer sentiment index in early February fell by -2.8 points to 76.2.

However, consumer confidence should start improving in March due to the sharp drop in new Covid infections and the easing of public restrictions. Indeed, there was some good news last week when Jan retail sales soared by +5.3% m/m, more than overcoming the overall -2.4% drop seen in the previous three months (Oct-Dec).

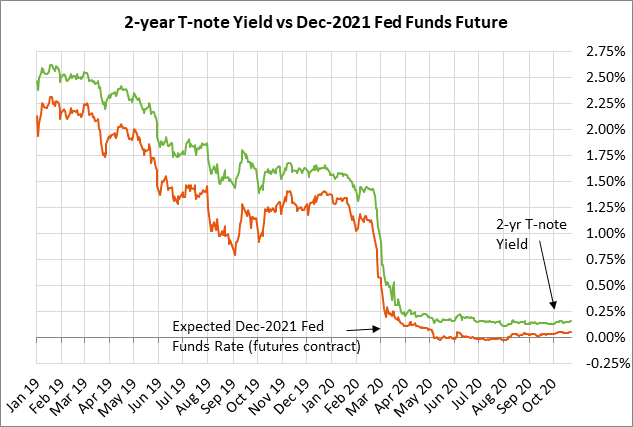

2-year T-note auction to yield near 0.11% — The Treasury today will sell $60 billion of 2-year T-notes, kicking off this week’s $209 billion T-note package. The benchmark 2-year T-note yield yesterday closed at 0.111%, not far above last week’s record low of 0.097%. The 2-year yield remains very low due to the Fed’s peg of the funds rate near zero and plentiful liquidity in the money markets.

The 12-auction averages for the 2-year are: 2.57 bid cover ratio, $126 million in non-competitive bids, 3.4 bp tail to the median yield, 14.1 bp tail to the low yield, 50% at the high yield, and 51.9% taken by indirect bidders (well below the 63.6% median for all recent coupon auctions).