- European stocks on Monday are undercut by downbeat IMF report

- Weekly global market focus

- Senate will try to move ahead with President Trump’s proposal for an end to the shutdown

- UK Parliament tries to coalesce around a Brexit solution although a delay of the deadline seems most likely

European stocks on Monday are undercut by downbeat IMF report — Asian stocks on Monday closed mostly higher on carry-over support from last Friday’s reports of progress on US/Chinese trade talks. Bloomberg reported that China is offering a path to eliminate the US/Chinese trade deficit by 2024 by buying some $1 trillion of U.S. products over those six years. The Shanghai Composite index on Monday closed +0.56% in the Nikkei index closed up +0.26%.

However, European stocks and U.S. stock index futures fell back later on Monday, undercut by the IMF’s downgrade in its 2019 global GDP forecast to a 3-year low of +3.5% from October’s +3.7% forecast due to slower growth in Europe and China. The IMF reduced the 2019 German GDP forecast by 0.6 points to +1.3% and the Eurozone GDP forecast by 0.3 points to +1.6%. The IMF left its forecast for 2019 Chinese GDP growth unchanged at +6.2%, which would be down from +6.6% in 2018.

In other negative news on Monday, China’s Q4 GDP fell to 6.4% y/y (matching the low seen in 2009), although that was in line with market expectations. The Chinese GDP decline was offset to some extent by the slightly stronger-than-expected Chinese Dec retail sales report of +8.2% y/y (vs expectations of +8.1%) and Dec industrial production report of +5.7% y/y (vs expectations of +5.3%). The retail sales and industrial production reports suggested that the Chinese economy at least closed out Q4 on at a slightly stronger-than-expected pace.

Weekly global market focus — The U.S. markets during this holiday-shortened week will focus on (1) any prospect for ending the month-long U.S. government shutdown, (2) any developments on US/Chinese trade tensions ahead of next week’s (Jan 30-31) high-level trade talks among Chinese Vice Premier Liu (President Xi’s top economic advisor), USTR Lighthizer, and U.S. Treasury Secretary Mnuchin, (3) Q4 earnings season which heats up with 60 of the S&P 500 companies scheduled to report this week, and (4) any news out of this week’s Davos conference.

In Europe, the focus is on Brexit and Thursday’s ECB meeting where the ECB may take a more dovish tone due to weaker Eurozone economic growth. The market has deferred expectations for the ECB’s first rate hike until December or early 2020 from previous expectations of September.

Senate will try to move ahead with President Trump’s proposal for an end to the shutdown — Democrats quickly rejected President Trump’s proposal on Saturday to allow a 3-year protection provision for DACA dreamers in return for Democrats agreeing to his demand for $5.7 billion for a wall. Democrats appear to be willing to trade only a permanent DACA fix for increased border security money or possibly part of a wall, not a temporary DACA fix.

Despite Speaker Pelosi’s quick rejection of the deal, Senate Majority Leader McConnell today is expected to put President Trump’s proposal up for a vote. If Democrats stick together, the bill will not get the 60 votes needed for cloture and the bill will be dead. However, Senate Majority Leader McConnell will at least be able to say that he is trying to move some legislation to get the government reopened.

The prospects for a deal to reopen the U.S. government remain slim, although the two sides are at least thinking about what they would trade for a deal. The shutdown today reached its 32nd day and federal employees will miss their second paycheck this Friday. White House economist Hassett recently revised his estimate higher for the negative impact of the shutdown on the U.S. economy to a -0.13 percentage point reduction in GDP for every week that the shutdown goes on, which currently adds up so far to a -0.52 point hit to U.S. GDP.

UK Parliament tries to coalesce around a Brexit solution although a delay of the deadline seems most likely — Prime Minister May on Monday presented her Plan B, which was really just Plan A with a promise to try to renegotiate the Irish backstop. However, the EU’s chief Brexit negotiator quickly rejected the idea of renegotiating the backstop and said the focus should instead be on more closely defining the eventual UK-EU trade relationship.

Ms. May continues to refuse to rule out a “no deal” Brexit and says there is no support in Commons for a second referendum. She also continues to reject the idea of the UK joining the EU customs union, which is favored by some in the opposition parties and could conceivably get a majority vote in Parliament but would be viscerally opposed by the hard-Brexit wing of her party.

Parliament is currently due to vote next Tuesday (Jan 29) on Ms. May’s Plan B along with any amendments. Until then, Parliament will be debating and considering amendments in an effort to find some path for moving forward. The March 29 Brexit date is now only two months away. EU officials and national leaders are busy discussing the length of any delay they would be willing to provide for the Brexit March 29 deadline.

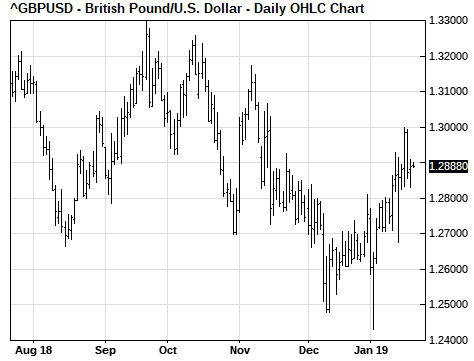

The current odds of the UK leaving the EU by April 1 without a Brexit deal are only 5/2 (i.e., a probability of 29%), according to www.oddschecker.com. We suspect that the chances of the UK crashing out of the EU on March 29 are probably lower than those betting odds since Parliament would rather take control of the Brexit process away from Ms. May and ask for a Brexit delay, than allow Ms. May to crash the UK out of the EU on March 29. The low odds for a no-deal Brexit explain why sterling continues to trade on a relatively strong note near last week’s 2-1/4 month high.