- Markets suspect the Fed is in the process of making a policy mistake

- U.S. unemployment claims expected to show small increases

- 5-year TIPS auction to yield near 1.10%

- Washington punts government shutdown until February

- Bank of England waits for Brexit developments

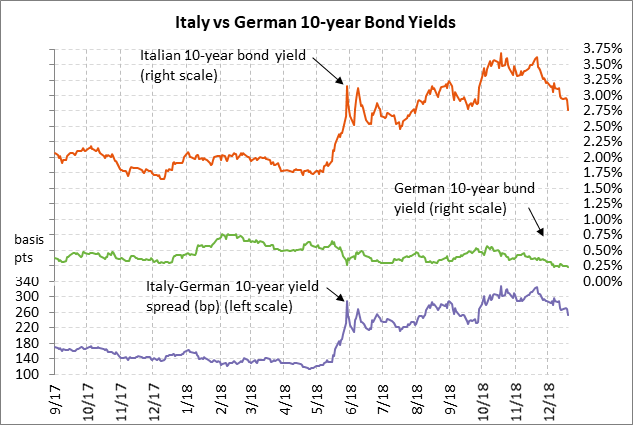

- EU-Italy budget compromise drives Italian bond yields to 4-3/4 month low

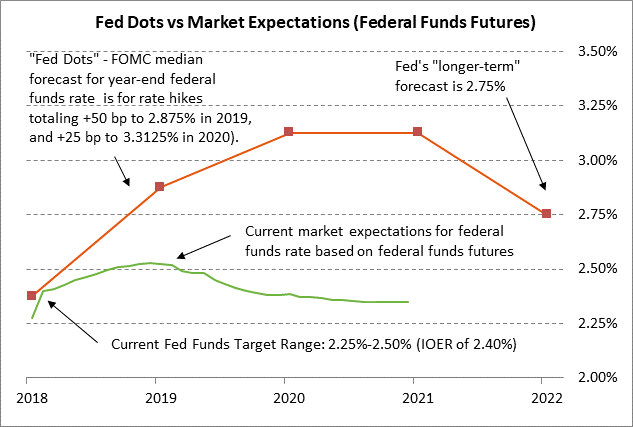

Markets suspect the Fed is in the process of making a policy mistake — The stock market on Wednesday fell sharply after the FOMC did not soften up the outlook for rate hikes by as much as the stock investors had hoped. The FOMC cut its Fed-dot forecasts by about one rate-hike but left two rate hikes in place for 2019. The Fed was also bullish on the economy, saying that the “labor market has continued to strengthen” and that “economic activity has been rising at a strong rate.” Fed Chair Powell brushed off the weakness in stocks as only one factor to consider in tighter financial conditions. The markets were also disappointed that Mr. Powell said that softening up on the Fed’s balance sheet reduction program is not an option at this time, meaning the Fed’s permanent reserve drain will continue at the maximum rate of $50 billion per month.

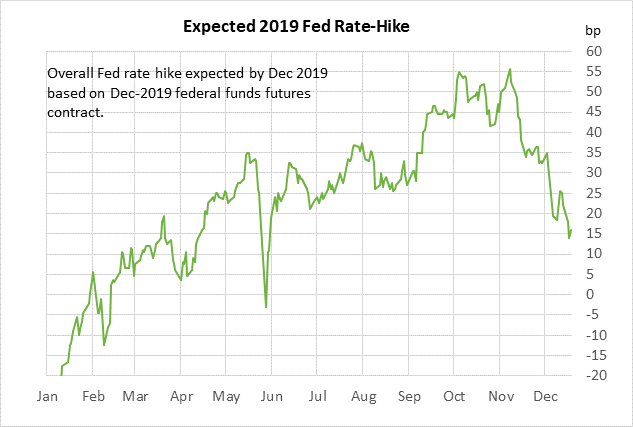

While the stock market took the hawkish FOMC outcome seriously, the federal funds futures curve showed little movement and suggested that (1) the FOMC meeting outcome was in line with expectations, and (2) the market still believes that the Fed is way off base and will not be able to raise rates by anywhere close to what the FOMC is anticipating. The federal funds futures market is expecting only 16 bp of rate hikes in 2019 (or about a 60% chance of one +25 bp hike), which is much more dovish than the median Fed-dot forecast for two rate hikes in 2019 and then another rate hike in 2020.

The federal funds futures curve on Wednesday turned slightly more hawkish by 1-3 bp for the 2019 contracts but actually turned more dovish by 1.5 bp for the late-2020 contracts. That showed that the market thinks the Fed will tighten too far in 2019, resulting in a small chance for a rate cut in 2020. The fact that 10-year T-note yield on Wednesday fell by -6 bp to 2.75% also suggests that the market believes that the Fed is in the process of making a policy mistake by driving the economy into a recession, resulting in lower inflation and lower long-term yields.

As expected, the FOMC on Wednesday raised its IOER rate (interest on excess reserves) rate by only +20 bp to 2.40% (less than the +25 bp funds rate hike to 2.25%/2.50%). That was a technical move designed to force the funds rate to trade closer to the new funds rate target midpoint of 2.375%.

On the more dovish side of Wednesday’s FOMC meeting, the Fed did soften up its interest rate guidance by saying that it now sees “some further gradual increases” in rates versus its previous guidance for “further gradual increases” in rates. In addition, the median Fed-dot forecast for the long-term neutral funds rate fell to 2.75% from 3.00%, which is only 37 bp above the current funds rate target midpoint of 2.38%.

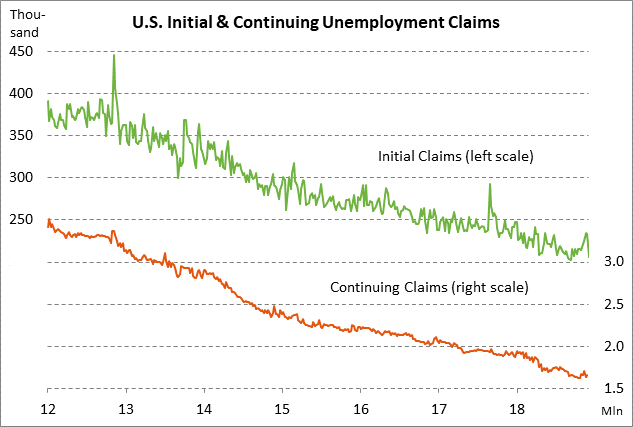

U.S. unemployment claims expected to show small increases — The consensus is for today’s weekly initial unemployment claims to show a +9,000 increase to 215,000 (reversing part of last week’s -27,000 to 206,000) and for continuing claims to rise by +2,000 to 1.663 million (adding to last week’s +25,000 to 1.661 million). The claims data remains in very favorable shape with initial claims only 4,000 above Sep’s 49-year low of 202,000 and continuing claims only 31,000 above October’s 45-year low of 1.630 million.

5-year TIPS auction to yield near 1.10% — The Treasury today will sell $14 billion of 5-year TIPS in the third and final reopening of April’s 5/8% 5-year TIPS of April 2023. The current 5-year TIPS yield of 1.10% is just mildly below November’s 9-year high of 1.17%. The 12-auction averages for the 5-year TIPS are as follows: 2.51 bid cover ratio, $44 million in non-competitive bids, 5.6 bp tail to the median yield, 15.9 bp tail to the low yield, 37% taken at the high yield. The 5-year TIPS is the third most popular security among foreign investors and central banks behind the 30-year and 10-year TIPS. Indirect bidders, a proxy for foreign buyers, have taken an average of 67.4% of the last twelve 5-year TIPS auctions, which is well above the median of 63.0% for all recent Treasury coupon auctions.

Washington punts government shutdown until February — Congress is in the process of passing a continuing resolution until February 5, thus eliminating the possibility of a partial U.S. government shutdown when the current CR expires Friday at midnight. With the stock market already in a bad mood from Wednesday’s FOMC meeting, the markets at least won’t have to worry about a government shutdown until February. In February, however, the standoff over President Trump’s border wall may be even more intractable since the Democrats will be in charge of the House.

Bank of England waits for Brexit developments — The unanimous view is that the Bank of England at its policy meeting today will leave the base rate unchanged at 0.75%. The BOE is firmly on hold until it sees whether the UK crashes out of the EU in March 2019. If Brexit goes smoothly, then the BOE may look at a rate hike for mid to late 2019.

EU-Italy budget compromise drives Italian bond yields to 4-3/4 month low — The EU and Italy on Wednesday reached a compromise on Italy’s budget and the EU will not begin the excessive deficit procedure. Yet, the EU will be closely monitoring Italy’s budget progress and could intervene again if Italy starts getting out of line. The 10-year Italian bond yield on Wednesday fell by -17 bp to a new 4-3/4 month low of 2.77%, which is down sharply from Oct’s 4-3/4 year high of 3.69% but still far above the 1.75% level seen before the Italian populist government took power and started talking about sharply higher spending and a blow-out of the government’s budget deficit.