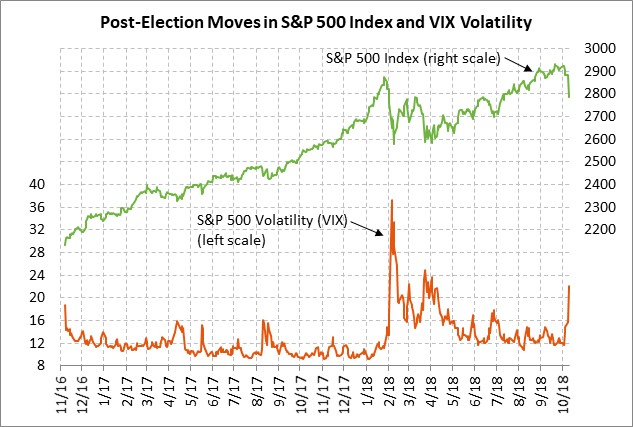

- VIX shoots up to 22.96% due to the sharp stock market sell-off

- Treasury auctions 30-year bonds with the yield near the recent 4-1/4 year high

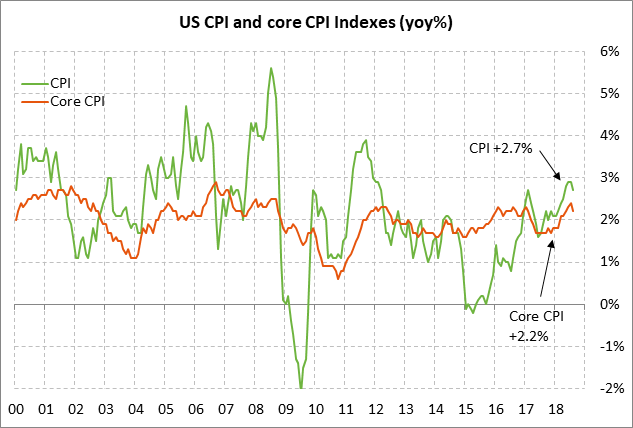

- U.S. core CPI expected near July’s 10-year high

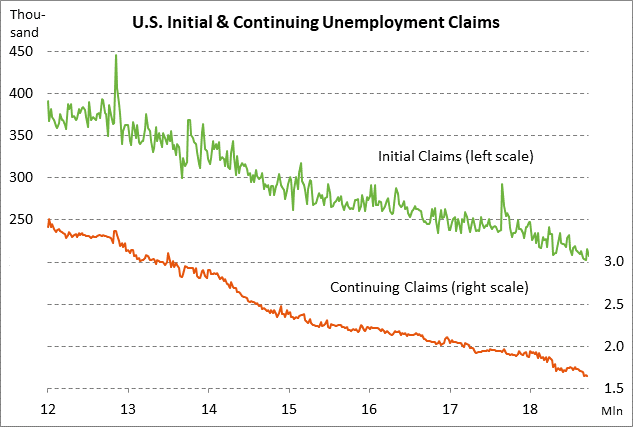

- U.S. unemployment claims remain in very favorable shape

- EIA report

VIX shoots up to 22.96% due to the sharp stock market sell-off — The VIX index on Wednesday rose sharply to a 6-1/4 month high of 22.96% as the stock market plunged. The VIX is now sharply above the average 13% level that prevailed during most of the summer. However, the VIX remains well below the 50% peak seen last February when the stock market plunged on trade tariffs and when the upward spike in the VIX raised questions about the viability of VIX ETFs.

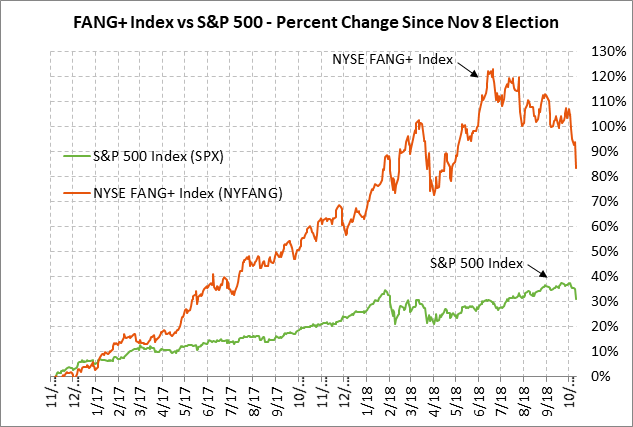

Wednesday’s risk-off hit tech stocks particularly hard. The Nymex FANG+ index plunged by -5.60% and the Nasdaq 100 fell by -4.44%. The S&P 500 index on Wednesday plunged by -3.29%, falling to a 3-month low and returning to levels last seen in July.

Bearish factors for stocks include (1) worries about rising long-term yields as the 10-year T-note yield on Tuesday rose to a 7-1/2 year high of 3.26%, (2) hawkish comments by Fed officials in the past several weeks and increased expectations for Fed rate-hikes through 2019, (3) US/Chinese trade tensions with the Treasury’s currency manipulation report due next week and with a possible announcement at any time by President Trump of more Chinese tariffs, (4) worries that Q3 earnings season may not live up to the market’s lofty expectations, particularly if tariffs raise input costs for some businesses, and (5) the blackout period for corporate buy-backs during Q3 earnings season.

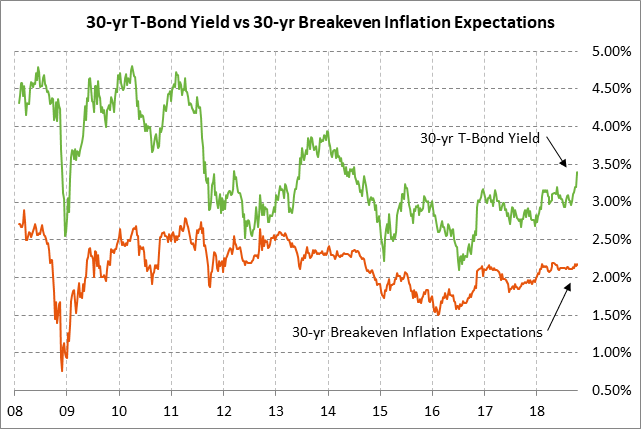

Treasury auctions 30-year bonds with the yield near the recent 4-1/4 year high — The Treasury today will sell $15 billion of 30-year T-bonds in the second and final reopening of August’s 2-7/8% bond of Aug 2028. The $15 billion size of today’s reopening is up by $1 billion from the June-July reopenings and is up by $3 billion from the $12 billion size that prevailed during most of 2016/17.

Yesterday’s 3-year and 10-year T-note auctions were a bit disappointing since the bid cover ratios were below average, indicating weak bidding. The tepid auctions suggested that investors are not impressed by current yield levels. The bid cover ratio for the 3-year of 2.56 was below the 12-auction average of 2.82 and the ratio for the 10-year of 2.39 was below the average of 2.51.

The benchmark 30-year bond late yesterday closed at 3.35%, which was 10 bp below Tuesday’s 4-1/4 year high of 3.45%. The 30-year T-bond yield has risen sharply by about 40 bp since the beginning on September and by 19 bp since early last week. The 30-year yield has risen on (1) increased expectations for Fed rate hikes and recent hawkish Fed comments, (2) strong U.S. economic data including the drop in the unemployment rate to a 49-year low of 3.7%, and (3) higher inflation expectations.

The 12-auction averages for the 30-year are as follows: 2.40 bid cover ratio, $6 million in non-competitive bids to mostly retail investors, 4.3 bp tail to the median yield, 40.3 bp tail to the low yield, and 39% taken at the high yield. The 30-year is a little below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.4% of the last twelve 30-year bond auctions, which is mildly below the median of 63.1% for all recent Treasury coupon auctions.

U.S. core CPI expected near July’s 10-year high — The market consensus is for today’s Sep CPI to ease to +2.4% y/y from Aug’s +2.7%, but for the Sep core CPI to edge higher to +2.3% from Aug’s +2.2%. The expected headline CPI report of +2.4% would be down by 0.5 points from the June/July 6-3/4 year high of 2.9%. The expected core CPI would be just 0.1 point below July’s 10-year high of +2.4% y/y.

The markets are waiting to see whether inflation will remain stable, as it did in August, or whether inflation will move higher due to the strong economy and higher input cost pressures from tariffs and wages. The good news was that the Fed’s preferred inflation measure, the PCE deflator, in August fell to 13-month low of +1.4% on a 3-month annualized basis and the core PCE deflator fell to a 15-month low of +1.3%. However, that weakness could quickly be reversed in coming months.

The market remains nervous about inflation as seen by the fact that the 10-year breakeven inflation expectations rate late last week rose to a 4-3/4 month high of 2.18%, above the Fed’s 2.0% inflation target. However, the breakeven rate yesterday eased to 2.15% due to the stock market rout.

U.S. unemployment claims remain in very favorable shape — The unemployment claims data remains in very favorable shape, indicating that layoffs are near the lowest levels in near five decades. Initial claims are only +5,000 above the mid-Sep 49-year low of 202,000 while continuing claims are only 5,000 above the early-Sep 45-year low of 1.645 million.

The claims data is just getting past the distortions from Hurricane Florence but will now be hit in next few reports by Hurricane Michael. The consensus is for today’s initial claims report to show a +2,000 increase to 209,000 and for continuing claims to show a +10,000 increase to 1.660 million.

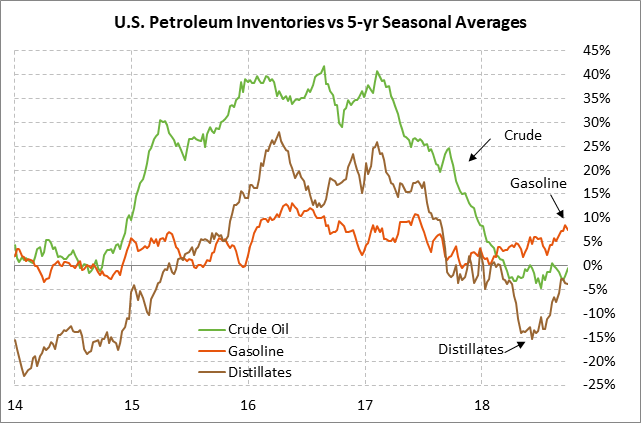

EIA report — The market consensus is for today’s weekly EIA report to show a +2.5 mln bbl rise in U.S. crude oil inventories, a -1.0 mln bbl decline in gasoline inventories, a -2.0 mln bbl decline in distillate inventories, and a -0.5 point decline in the refinery utilization rate to 89.9%. U.S. crude oil inventories are -0.5% below the 5-year seasonal average. Product inventories are mixed with gasoline inventories +7.4% above average but with distillate inventories -3.8% below average. U.S. oil production in last week’s report remained at a record high of 11.1 million bpd.