- Global market weekly focus

- European focus is on Italian election, ECB meeting, and trade

- Asian focus is on Chinese Congress, trade tensions, and BOJ meeting

- Trade tensions will continue to dominate market attention

- U.S. stock market remains wounded by interest rates and trade tensions

Global market weekly focus — The U.S. markets this week will focus on (1) trade concerns as the Trump administration this week is expected to release the details of its steel and aluminum tariffs and as U.S. trade partners may announce retaliatory measures, (2) Fed policy after Fed Chair Powell’s hawkish commentary last week and with a busy schedule of Fed speakers this week, (3) Friday’s U.S. Feb unemployment report where the markets will be carefully assessing the tightness of the labor market and wage pressures, (4) whether the U.S. stock market can regain its balance after last week’s sharp sell-off on hawkish Powell testimony and Trump tariffs, and (5) oil prices, which fell last week on the hawkish Powell testimony and the weakness in stocks, along with the rise in U.S. crude oil inventories.

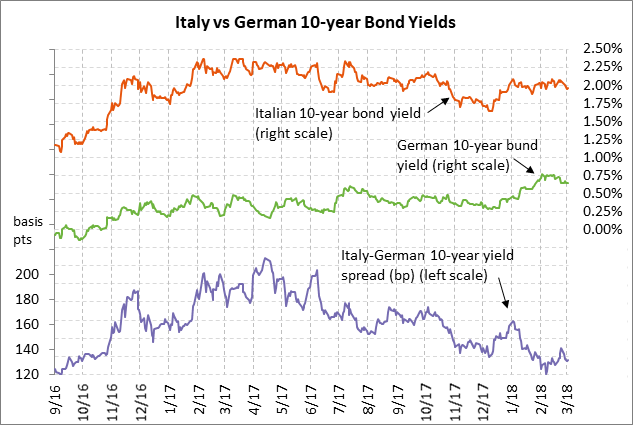

European focus is on Italian election, ECB meeting, and trade — The European markets this week will focus on (1) the outcome of Sunday’s Italian general election and the prospects for a stable, generally pro-EU coalition government (2) relief that Germany should now have a stable government for at least the next few years after Social Democrats voted in favor of continuing the grand coalition with Chancellor Merkel’s CDU bloc, and (3) the ECB meeting on Thursday, which could produce a tweak on guidance although the markets are not expecting any major news on the QE program that is currently announced through September, (4) any European trade retaliation that may be announced in response to U.S. steel and aluminum tariffs, and (5) the European stock market, which was even weaker than the U.S. stock market with the Euro Stoxx 50 index last week falling by -3.39% and nearly challenging the early-Feb 1-year low.

Early indications for Sunday’s Italian election were for a hung parliament, as expected. EUR/USD was slightly higher on Sunday night as results were coming in. Based on exit polls, Berlusconi’s center-right bloc was seen winning 225-265 seats in the lower house, Five Star winning 195-235 seats, and the center-left winning 115-155 seats. If the center-right bloc wins the election over Five Star, they will get the first shot at forming a government, although they will have to gain support from other parties to overcome a hung parliament.

Asian focus is on Chinese Congress, trade tensions, and BOJ meeting — In Asia, the focus will mainly be on China where the National People’s Congress meets for the next two weeks to ratify government decisions. The Chinese government on Sunday night announced a 2018 growth target of around 6.5%, which was in line with market expectations and the 2017 target. The markets are waiting to see if there will be an announcement of a new head of the Chinese central bank. There is key Chinese economic data coming out this week, which includes Wednesday’s Chinese Feb trade report (exports expected +10.0% y/y), Thursday’s Feb CPI report (expected +2.4% y/y vs Jan’s +1.5%), and Friday’s China loan data.

In Japan, the markets are not expecting any significant change in monetary policy on Friday at the BOJ meeting. However, perceptions of BOJ policy tightened up after BOJ Governor Kuroda last Friday said that the BOJ will start thinking about how to exit from its massive stimulus program around the next fiscal year starting in April 2019.

Trade tensions will continue to dominate market attention — Trade tensions will continue to dominate market attention this week as the Trump administration may formally announce the details of the tariffs of 25% on steel imports and 10% on aluminum imports that President Trump announced on an impromptu basis last week. The markets are hoping that the administration might water down the tariffs somewhat by giving exemptions, possibly to Canada since the U.S. and Canada have a large amount of 2-way trade on steel. However, White House trade advisor Peter Navarro on Sunday said that there would be no exemptions for any country.

President Trump over the weekend upped the ante by threatening to retaliate with a tariff on European car exports if Europe makes good on threats to retaliate to U.S. steel and aluminum tariffs with tariffs on U.S. motorcycles, jeans and bourbon. Meanwhile, China took a more measured response as Vice Foreign Minister Zhang Yesui on Sunday announced that China will host U.S. officials for a new round of dialogue on trade issues. In addition, China announced early Monday they plan to cut tariffs on autos and some consumer goods, reducing the threat of a trade war.

U.S. trade partners are under pressure to retaliate in some way to Mr. Trump’s steel and aluminum tariffs to raise the price to Mr. Trump and discourage him from implementing new tariffs or protectionist measures. However, we expect U.S. trade partners to take only measured steps that are not large enough to prompt Mr. Trump to launch a new round of protectionist measures that could spiral into a real trade war.

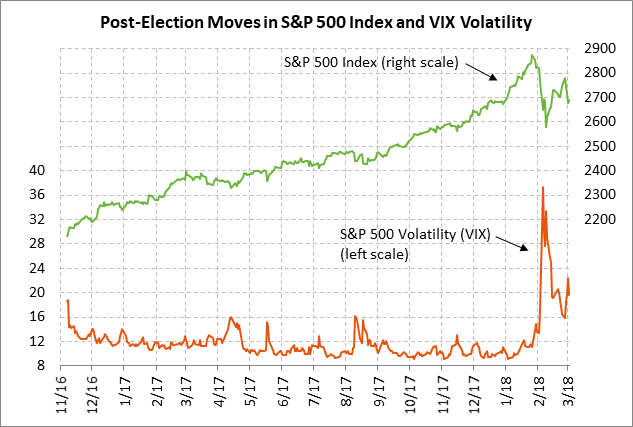

U.S. stock market remains wounded by interest rates and trade tensions — The U.S. stock and bond markets will remain on edge this week due to trade tensions and a heavy schedule of Fed speakers that could turn the markets more hawkish on Fed policy. The S&P 500 index last week sold off sharply by a total of -5.1% from last Tuesday’s 1-month high and closed the week down -2.05%. Stocks took a hit on hawkish testimony from Fed Chair Powell and on President Trump’s announcement on Thursday of across-the-board tariffs on steel and aluminum.

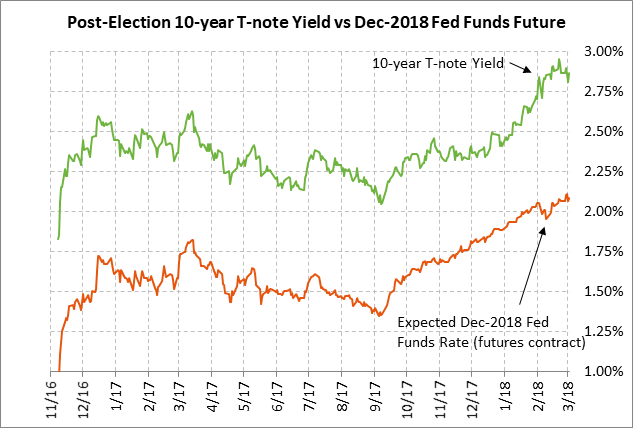

The only good news for the stock market last week was that the 10-year T-note yield backed off slightly and closed the week down -2 bp at 2.86%. T-note prices received a boost from the tariff news due to safe-haven demand and the risk of slower global economic growth if a trade war breaks out.