- Powell has a chance to fine-tune his Congressional testimony

- Fed’s favorite inflation measure is expected to be steady

- U.S. ISM manufacturing index expected to show a decline but remain strong

- Markets remain sanguine about Sunday’s Italian election and German coalition news

- China’s stock market winds down to Sunday’s Congress meeting

Powell has a chance to fine-tune his Congressional testimony — Fed Chair Powell today will appear before the Senate Banking Committee in the second edition of his semi-annual testimony on monetary policy. If he is so inclined, Mr. Powell today will have the opportunity to either dial back, or reiterate, his hawkishly-received comments on Tuesday before the House committee.

The markets on Tuesday interpreted Mr. Powell’s comments as net-hawkish since he said he believes that the economy has strengthened and the inflation prospects have increased since the FOMC’s meeting in December when the last set of Fed dots were released. His comments suggested that FOMC members at their next meeting in three weeks on March 20-21 may revise higher their Fed-dot projections for the federal funds rate.

The S&P 500 index fell sharply on Tuesday by -1.27% after the Powell testimony, and then fell by another -1.11% on Wednesday on uncertainty about Mr. Powell’s testimony today. In addition to the interest-rate implications of his comments, stock investors were a little perturbed on Tuesday when Mr. Powell indicated no real concern about the early-Feb plunge in stocks. The markets took that as at least a small hint that Mr. Powell will feel no real obligation to ease monetary policy if there is a real crash in stocks. Some investors are concerned that if the Fed doesn’t have the stock market’s back, then perhaps stocks should be trading at more conservative valuation levels.

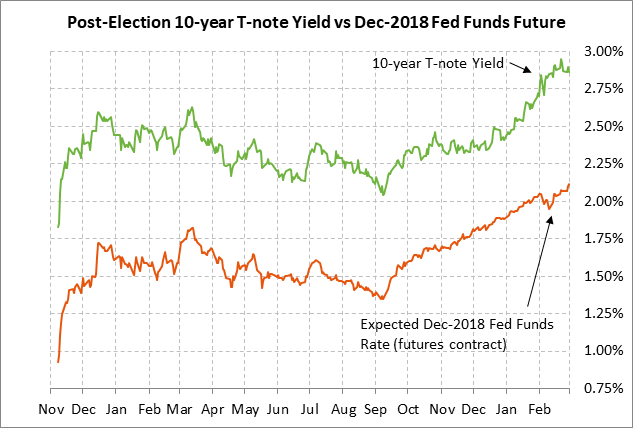

The market’s expectation for 2018 rate hikes rose by another 1.5 bp on Wednesday to a new high of 74.0 bp, nearly reaching the full 75 bp (3.0 rate hikes) that FOMC members are forecasting in the Fed dots. In some good news for the stock market, however, the 10-year T-note yield on Wednesday fell by -3 bp to 2.86% and is now -9 bp below last Wednesday’s 4-year high of 2.95%.

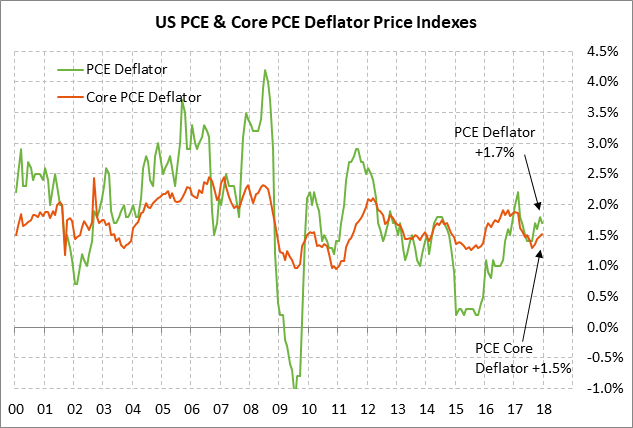

Fed’s favorite inflation measure is expected to be steady — The markets will be closely watching today’s PCE deflator report to gauge whether inflation is rising and whether the Fed may have to accelerate its rate hike regime. The markets have become more concerned about inflation as seen by the fact that the 10-year breakeven inflation expectations rate is currently at 2.12%, up by 22 bp from the 1.90% level seen in mid-December before Congress passed the tax cut bill.

Moreover, the Jan CPI report released two weeks ago contained some alarming data. On a year-on-year basis, the Jan CPI looked tame by remaining unchanged from Dec’s +2.1% y/y and with the core CPI remaining unchanged from Dec’s +1.8% y/y. However, the CPI in the past three months has accelerated to a 5-1/4 year high of +4.4% (annualized) and the core CPI accelerated to a 6-1/2 year high of +2.9% (annualized).

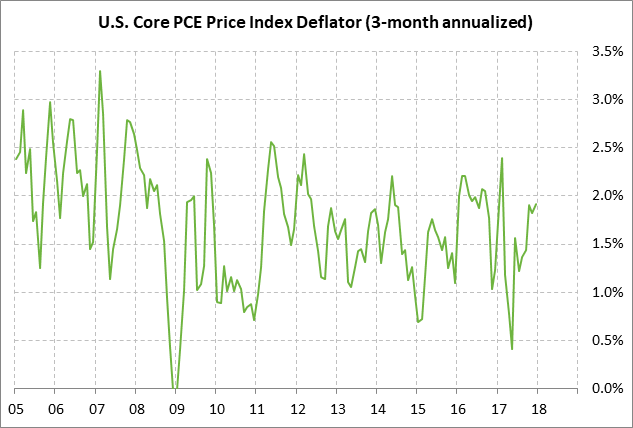

Inflation tensions should ease a bit if today’s PCE deflator is in line with market expectations. The consensus is for today’s Jan PCE deflator to be unchanged from Dec’s +1.6% y/y and for the core deflator to be unchanged at +1.5% y/y. However, the markets will also be watching the 3-month figures in today’s deflator report considering the bloated Jan CPI figures. In December, the PCE deflator on a 3-month basis was up by +2.0% and the core deflator was up by +2.1%, which were higher than the year-on-year figures but not in significant violation of the Fed’s 2.0% inflation target.

U.S. ISM manufacturing index expected to show a decline but remain strong — The market consensus is for today’s ISM manufacturing index to show a -0.5 point decline to 58.6, adding to Jan’s -0.2 point decline to 59.1. Despite the possible back-to-back decline, the expected report of 58.6 would still be a strong level that is just mildly below the 13-1/2 year high of 60.2 posted in Sep 2017. Moreover, the new orders sub-index was in even stronger shape than the headline index in January at 65.4, showing strong confidence about manufacturing order flows.

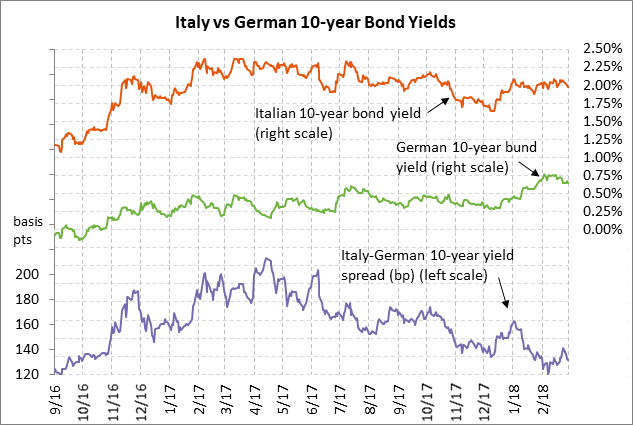

Markets remain sanguine about Sunday’s Italian election and German coalition news — The markets remain largely unworried about this Sunday’s key European political events when Italy holds a national election and the Germany’s Social Democrats announce whether members voted to approve a coalition government with Chancellor Merkel’s CDU bloc. Social Democrats are expected to approve the coalition, but if there is a surprise rejection, the euro is likely to fall since Ms. Merkel will have little choice but to call new elections.

In Italy, no single party or coalition is expected to win a working majority, possibly resulting in a hung parliament and new elections. However, the markets seem to be counting on either a center-right coalition or a grand coalition between Berlusconi’s Forza Italia party and Renzi’s Democratic Party. Concern about the anti-EU Five Star Movement has eased a bit since they are expected to be frozen out of any coalition government and in any case have toned down their anti-EU rhetoric somewhat. The Italian 10-year government bond yield on Wednesday closed at a tame spread of 131.7 bp above Germany, which is only +11.5 above the 2-1/2 year low of 120.2 bp posted in early-Feb.

China’s stock market winds down to Sunday’s Congress meeting — Funds have been instructed by government regulators not to engage in any major selling of stocks after the National People’s Congress begins this Sunday, according to Bloomberg. The meeting is expected to last about two weeks. Chinese officials are trying to avoid any embarrassing stock market sell-offs while legislators convene to decide a variety of issues. Bloomberg reported that some of this week’s weakness in Chinese stocks may have been due to investors getting their selling out of the way before next week.