PM

- Weekly global market focus

- U.S. government shutdown appears unlikely this week

- Jan Markit services PMI expected to stabilize after 2-month drop

- Rise in 10-year T-note yield to 4-year high sparks further long liquidation pressure in stocks

Weekly global market focus — The U.S. markets this week will focus on (1) whether interest rates continue to rise after the 10-year T-note yield last Friday reached a new 4-year high of 2.85%, (2) whether the stock market will extend its downside correction, which has been caused mainly by the sharp increase in interest rates, (3) Fed policy as the Powell era begins with Jerome Powell being sworn in today as the new Fed Chair, (4) crude oil prices, which remain near their recent 3-year high, (5) another busy week for Q4 earnings season with 93 of the SPX companies reporting, (6) the Treasury’s refunding operation on Tuesday through Thursday, and (7) whether there will be another U.S. government shutdown this Thursday (Feb 8) at midnight when the continuing resolution expires.

In Europe, the focus will mainly be on whether a German grand coalition government can be formed by early this week. Chancellor Merkel’s CDU bloc and the Social Democrats could not reach a final agreement by their self-imposed deadline of Sunday but extended their talks by another two days. The parties are likely to reach an agreement, but if the process should unexpectedly go off the rails, then Ms. Merkel will likely be forced to call new German elections, thus upsetting the European markets.

The European markets are also focused on Thursday’s Bank of England meeting. The BOE is expected to leave rates unchanged but could move to more hawkish language to flag the risk of a rate hike this spring.

The Asian markets are focused on Japanese monetary policy after the BOJ last Friday announced unlimited JGB purchases at 0.11% to combat market speculation that the BOJ is getting closer to normalizing monetary policy. There were no buyers at the 0.11% yield level but BOJ succeeded in reinforcing the view that it will do whatever it takes to prevent the 10-year JGB yield from rising above the 0.1% level that is viewed as the upper end of the BOJ’s target around zero for the 10-year JGB yield.

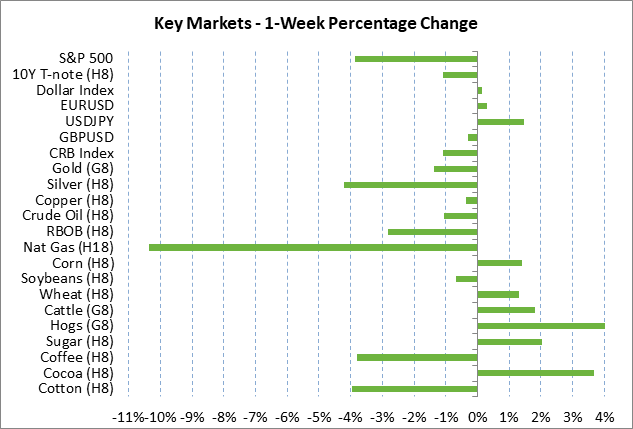

The Chinese markets face a fairly busy week with trade data on Wednesday evening, CPI-PPI data on Thursday evening, and loan data on Friday evening. The Chinese markets will also continue to watch the strength in the yuan, which reached a new 2-1/2 year high against the dollar last Friday. The strong yuan is undercutting Chinese exports, but is also boosting confidence among Chinese investors about keeping their capital at home. The Shanghai Composite index last week closed -2.70%, which was a smaller drop than the -3.85% weekly drop in the S&P 500 index.

U.S. government shutdown appears unlikely this week — There will be another U.S. government shutdown if Congress does not approve new spending authority by this Thursday (Feb 8) at midnight. However, a shutdown does not appear to be likely because Senate Democrats have already received a promise from Senate Majority Leader McConnell that he will allow a separate vote on the Senate floor on an immigration bill.

Meanwhile in the House, Speaker Ryan reportedly plans to hold a vote in the House on Tuesday for a new continuing resolution that will last until March 22 or 23. The Freedom Caucus is again threatening to vote against the CR but they are likely to relent, thus allowing the CR to pass the House without support from Democrats.

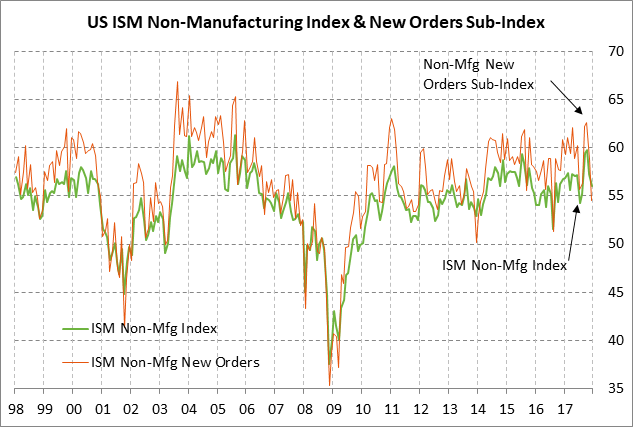

Jan Markit services PMI expected to stabilize after 2-month drop — The market consensus is for today’s Jan ISM non-manufacturing PMI to show a +0.7 point increase to 56.7, recovering about one-half of the -1.3 point decline to 56.0 seen in December. The index in Nov-Dec fell by a total of -3.8 points from the 12-1/4 year high of 59.8 posted in October. Despite that 2-month decline, the index remains in strong shape at 56.0, which indicates that service-sector executives are optimistic about the economy. Last Thursday’s ISM manufacturing index fell by -0.2 points to 59.1, giving back part of Dec’s +1.1 point increase to 59.3.

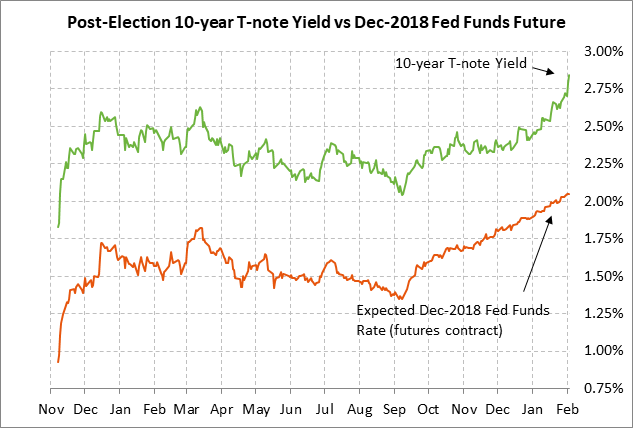

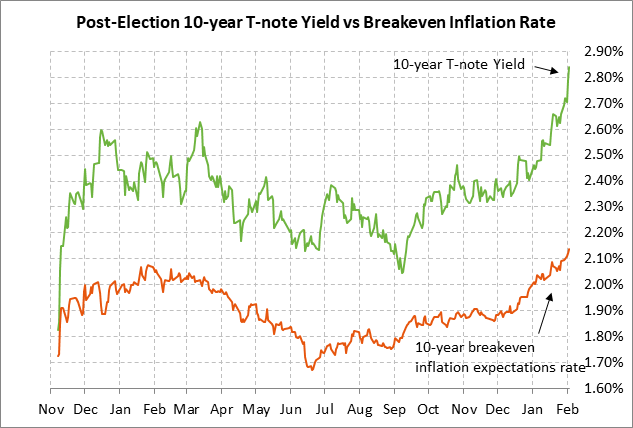

Rise in 10-year T-note yield to 4-year high sparks further long liquidation pressure in stocks — The 10-year T-note yield has risen sharply by more than 20 bp just in the past 1-1/2 weeks and posted a new 4-year high of 2.85% last Friday. The T-note yield was driven higher last Friday by the stronger-than-expected Jan payroll report of +200,000 and by continued concern about inflation pressures and Fed tightening.

The 10-year breakeven rate last Friday rose to a new 3-1/2 year high of 2.14%, illustrating that 10-year inflation expectations have now moved decisively above the Fed’s +2.0% inflation target. Meanwhile, the market is discounting +67.5 bp worth of Fed tightening in 2018, the largest amount yet and just below the Fed’s forecast for +75 bp worth of tightening in 2018 (i.e., three rate hikes).

The sharp rise in the 10-year T-note yield seen since late-December when Congress passed the tax-cut bill has finally started to take a toll on the stock market. The stock market was already vulnerable to a technical correction due to stretched valuations and the size of the rally seen after the tax-cut bill. The stock market is also displaying some concerns about Washington political strife as the market worries that President Trump might fire Deputy Attorney General Rod Rosenstein and/or Special Counsel Robert Mueller as it comes down to the wire about whether President Trump will be interviewed by the Special Counsel.

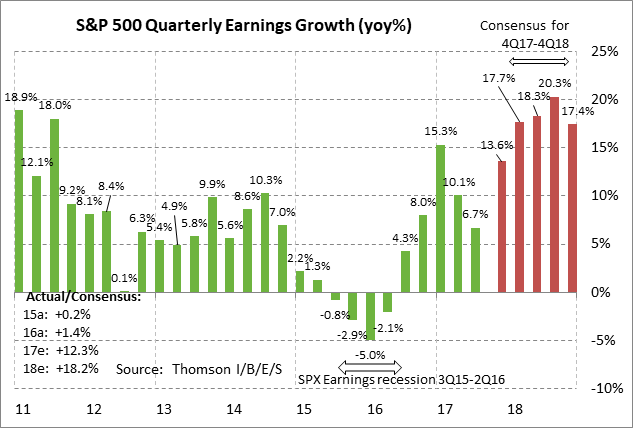

Q4 earnings season is now past its peak and is therefore waning as an upside catalyst for stocks. The consensus is for Q4 earnings growth of +13.6%, according to Thomson I/B/E/S. Of the 251 reporting SPX companies, 78% have beaten their consensus, above the long-term average of 64% and the 4-quarter average of 72%.

Weekly global market focus — The U.S. markets this week will focus on (1) whether interest rates continue to rise after the 10-year T-note yield last Friday reached a new 4-year high of 2.85%, (2) whether the stock market will extend its downside correction, which has been caused mainly by the sharp increase in interest rates, (3) Fed policy as the Powell era begins with Jerome Powell being sworn in today as the new Fed Chair, (4) crude oil prices, which remain near their recent 3-year high, (5) another busy week for Q4 earnings season with 93 of the SPX companies reporting, (6) the Treasury’s refunding operation on Tuesday through Thursday, and (7) whether there will be another U.S. government shutdown this Thursday (Feb 8) at midnight when the continuing resolution expires.

In Europe, the focus will mainly be on whether a German grand coalition government can be formed by early this week. Chancellor Merkel’s CDU bloc and the Social Democrats could not reach a final agreement by their self-imposed deadline of Sunday but extended their talks by another two days. The parties are likely to reach an agreement, but if the process should unexpectedly go off the rails, then Ms. Merkel will likely be forced to call new German elections, thus upsetting the European markets.

The European markets are also focused on Thursday’s Bank of England meeting. The BOE is expected to leave rates unchanged but could move to more hawkish language to flag the risk of a rate hike this spring.

The Asian markets are focused on Japanese monetary policy after the BOJ last Friday announced unlimited JGB purchases at 0.11% to combat market speculation that the BOJ is getting closer to normalizing monetary policy. There were no buyers at the 0.11% yield level but BOJ succeeded in reinforcing the view that it will do whatever it takes to prevent the 10-year JGB yield from rising above the 0.1% level that is viewed as the upper end of the BOJ’s target around zero for the 10-year JGB yield.

The Chinese markets face a fairly busy week with trade data on Wednesday evening, CPI-PPI data on Thursday evening, and loan data on Friday evening. The Chinese markets will also continue to watch the strength in the yuan, which reached a new 2-1/2 year high against the dollar last Friday. The strong yuan is undercutting Chinese exports, but is also boosting confidence among Chinese investors about keeping their capital at home. The Shanghai Composite index last week closed -2.70%, which was a smaller drop than the -3.85% weekly drop in the S&P 500 index.

U.S. government shutdown appears unlikely this week — There will be another U.S. government shutdown if Congress does not approve new spending authority by this Thursday (Feb 8) at midnight. However, a shutdown does not appear to be likely because Senate Democrats have already received a promise from Senate Majority Leader McConnell that he will allow a separate vote on the Senate floor on an immigration bill.

Meanwhile in the House, Speaker Ryan reportedly plans to hold a vote in the House on Tuesday for a new continuing resolution that will last until March 22 or 23. The Freedom Caucus is again threatening to vote against the CR but they are likely to relent, thus allowing the CR to pass the House without support from Democrats.

Jan Markit services PMI expected to stabilize after 2-month drop — The market consensus is for today’s Jan ISM non-manufacturing PMI to show a +0.7 point increase to 56.7, recovering about one-half of the -1.3 point decline to 56.0 seen in December. The index in Nov-Dec fell by a total of -3.8 points from the 12-1/4 year high of 59.8 posted in October. Despite that 2-month decline, the index remains in strong shape at 56.0, which indicates that service-sector executives are optimistic about the economy. Last Thursday’s ISM manufacturing index fell by -0.2 points to 59.1, giving back part of Dec’s +1.1 point increase to 59.3.

Rise in 10-year T-note yield to 4-year high sparks further long liquidation pressure in stocks — The 10-year T-note yield has risen sharply by more than 20 bp just in the past 1-1/2 weeks and posted a new 4-year high of 2.85% last Friday. The T-note yield was driven higher last Friday by the stronger-than-expected Jan payroll report of +200,000 and by continued concern about inflation pressures and Fed tightening.

The 10-year breakeven rate last Friday rose to a new 3-1/2 year high of 2.14%, illustrating that 10-year inflation expectations have now moved decisively above the Fed’s +2.0% inflation target. Meanwhile, the market is discounting +67.5 bp worth of Fed tightening in 2018, the largest amount yet and just below the Fed’s forecast for +75 bp worth of tightening in 2018 (i.e., three rate hikes).

The sharp rise in the 10-year T-note yield seen since late-December when Congress passed the tax-cut bill has finally started to take a toll on the stock market. The stock market was already vulnerable to a technical correction due to stretched valuations and the size of the rally seen after the tax-cut bill. The stock market is also displaying some concerns about Washington political strife as the market worries that President Trump might fire Deputy Attorney General Rod Rosenstein and/or Special Counsel Robert Mueller as it comes down to the wire about whether President Trump will be interviewed by the Special Counsel.

Q4 earnings season is now past its peak and is therefore waning as an upside catalyst for stocks. The consensus is for Q4 earnings growth of +13.6%, according to Thomson I/B/E/S. Of the 251 reporting SPX companies, 78% have beaten their consensus, above the long-term average of 64% and the 4-quarter average of 72%.

Weekly global market focus — The U.S. markets this week will focus on (1) whether interest rates continue to rise after the 10-year T-note yield last Friday reached a new 4-year high of 2.85%, (2) whether the stock market will extend its downside correction, which has been caused mainly by the sharp increase in interest rates, (3) Fed policy as the Powell era begins with Jerome Powell being sworn in today as the new Fed Chair, (4) crude oil prices, which remain near their recent 3-year high, (5) another busy week for Q4 earnings season with 93 of the SPX companies reporting, (6) the Treasury’s refunding operation on Tuesday through Thursday, and (7) whether there will be another U.S. government shutdown this Thursday (Feb 8) at midnight when the continuing resolution expires.

In Europe, the focus will mainly be on whether a German grand coalition government can be formed by early this week. Chancellor Merkel’s CDU bloc and the Social Democrats could not reach a final agreement by their self-imposed deadline of Sunday but extended their talks by another two days. The parties are likely to reach an agreement, but if the process should unexpectedly go off the rails, then Ms. Merkel will likely be forced to call new German elections, thus upsetting the European markets.

The European markets are also focused on Thursday’s Bank of England meeting. The BOE is expected to leave rates unchanged but could move to more hawkish language to flag the risk of a rate hike this spring.

The Asian markets are focused on Japanese monetary policy after the BOJ last Friday announced unlimited JGB purchases at 0.11% to combat market speculation that the BOJ is getting closer to normalizing monetary policy. There were no buyers at the 0.11% yield level but BOJ succeeded in reinforcing the view that it will do whatever it takes to prevent the 10-year JGB yield from rising above the 0.1% level that is viewed as the upper end of the BOJ’s target around zero for the 10-year JGB yield.

The Chinese markets face a fairly busy week with trade data on Wednesday evening, CPI-PPI data on Thursday evening, and loan data on Friday evening. The Chinese markets will also continue to watch the strength in the yuan, which reached a new 2-1/2 year high against the dollar last Friday. The strong yuan is undercutting Chinese exports, but is also boosting confidence among Chinese investors about keeping their capital at home. The Shanghai Composite index last week closed -2.70%, which was a smaller drop than the -3.85% weekly drop in the S&P 500 index.

U.S. government shutdown appears unlikely this week — There will be another U.S. government shutdown if Congress does not approve new spending authority by this Thursday (Feb 8) at midnight. However, a shutdown does not appear to be likely because Senate Democrats have already received a promise from Senate Majority Leader McConnell that he will allow a separate vote on the Senate floor on an immigration bill.

Meanwhile in the House, Speaker Ryan reportedly plans to hold a vote in the House on Tuesday for a new continuing resolution that will last until March 22 or 23. The Freedom Caucus is again threatening to vote against the CR but they are likely to relent, thus allowing the CR to pass the House without support from Democrats.

Jan Markit services PMI expected to stabilize after 2-month drop — The market consensus is for today’s Jan ISM non-manufacturing PMI to show a +0.7 point increase to 56.7, recovering about one-half of the -1.3 point decline to 56.0 seen in December. The index in Nov-Dec fell by a total of -3.8 points from the 12-1/4 year high of 59.8 posted in October. Despite that 2-month decline, the index remains in strong shape at 56.0, which indicates that service-sector executives are optimistic about the economy. Last Thursday’s ISM manufacturing index fell by -0.2 points to 59.1, giving back part of Dec’s +1.1 point increase to 59.3.

Rise in 10-year T-note yield to 4-year high sparks further long liquidation pressure in stocks — The 10-year T-note yield has risen sharply by more than 20 bp just in the past 1-1/2 weeks and posted a new 4-year high of 2.85% last Friday. The T-note yield was driven higher last Friday by the stronger-than-expected Jan payroll report of +200,000 and by continued concern about inflation pressures and Fed tightening.

The 10-year breakeven rate last Friday rose to a new 3-1/2 year high of 2.14%, illustrating that 10-year inflation expectations have now moved decisively above the Fed’s +2.0% inflation target. Meanwhile, the market is discounting +67.5 bp worth of Fed tightening in 2018, the largest amount yet and just below the Fed’s forecast for +75 bp worth of tightening in 2018 (i.e., three rate hikes).

The sharp rise in the 10-year T-note yield seen since late-December when Congress passed the tax-cut bill has finally started to take a toll on the stock market. The stock market was already vulnerable to a technical correction due to stretched valuations and the size of the rally seen after the tax-cut bill. The stock market is also displaying some concerns about Washington political strife as the market worries that President Trump might fire Deputy Attorney General Rod Rosenstein and/or Special Counsel Robert Mueller as it comes down to the wire about whether President Trump will be interviewed by the Special Counsel.

Q4 earnings season is now past its peak and is therefore waning as an upside catalyst for stocks. The consensus is for Q4 earnings growth of +13.6%, according to Thomson I/B/E/S. Of the 251 reporting SPX companies, 78% have beaten their consensus, above the long-term average of 64% and the 4-quarter average of 72%.

Weekly global market focus — The U.S. markets this week will focus on (1) whether interest rates continue to rise after the 10-year T-note yield last Friday reached a new 4-year high of 2.85%, (2) whether the stock market will extend its downside correction, which has been caused mainly by the sharp increase in interest rates, (3) Fed policy as the Powell era begins with Jerome Powell being sworn in today as the new Fed Chair, (4) crude oil prices, which remain near their recent 3-year high, (5) another busy week for Q4 earnings season with 93 of the SPX companies reporting, (6) the Treasury’s refunding operation on Tuesday through Thursday, and (7) whether there will be another U.S. government shutdown this Thursday (Feb 8) at midnight when the continuing resolution expires.

In Europe, the focus will mainly be on whether a German grand coalition government can be formed by early this week. Chancellor Merkel’s CDU bloc and the Social Democrats could not reach a final agreement by their self-imposed deadline of Sunday but extended their talks by another two days. The parties are likely to reach an agreement, but if the process should unexpectedly go off the rails, then Ms. Merkel will likely be forced to call new German elections, thus upsetting the European markets.

The European markets are also focused on Thursday’s Bank of England meeting. The BOE is expected to leave rates unchanged but could move to more hawkish language to flag the risk of a rate hike this spring.

The Asian markets are focused on Japanese monetary policy after the BOJ last Friday announced unlimited JGB purchases at 0.11% to combat market speculation that the BOJ is getting closer to normalizing monetary policy. There were no buyers at the 0.11% yield level but BOJ succeeded in reinforcing the view that it will do whatever it takes to prevent the 10-year JGB yield from rising above the 0.1% level that is viewed as the upper end of the BOJ’s target around zero for the 10-year JGB yield.

The Chinese markets face a fairly busy week with trade data on Wednesday evening, CPI-PPI data on Thursday evening, and loan data on Friday evening. The Chinese markets will also continue to watch the strength in the yuan, which reached a new 2-1/2 year high against the dollar last Friday. The strong yuan is undercutting Chinese exports, but is also boosting confidence among Chinese investors about keeping their capital at home. The Shanghai Composite index last week closed -2.70%, which was a smaller drop than the -3.85% weekly drop in the S&P 500 index.

U.S. government shutdown appears unlikely this week — There will be another U.S. government shutdown if Congress does not approve new spending authority by this Thursday (Feb 8) at midnight. However, a shutdown does not appear to be likely because Senate Democrats have already received a promise from Senate Majority Leader McConnell that he will allow a separate vote on the Senate floor on an immigration bill.

Meanwhile in the House, Speaker Ryan reportedly plans to hold a vote in the House on Tuesday for a new continuing resolution that will last until March 22 or 23. The Freedom Caucus is again threatening to vote against the CR but they are likely to relent, thus allowing the CR to pass the House without support from Democrats.

Jan Markit services PMI expected to stabilize after 2-month drop — The market consensus is for today’s Jan ISM non-manufacturing PMI to show a +0.7 point increase to 56.7, recovering about one-half of the -1.3 point decline to 56.0 seen in December. The index in Nov-Dec fell by a total of -3.8 points from the 12-1/4 year high of 59.8 posted in October. Despite that 2-month decline, the index remains in strong shape at 56.0, which indicates that service-sector executives are optimistic about the economy. Last Thursday’s ISM manufacturing index fell by -0.2 points to 59.1, giving back part of Dec’s +1.1 point increase to 59.3.

Rise in 10-year T-note yield to 4-year high sparks further long liquidation pressure in stocks — The 10-year T-note yield has risen sharply by more than 20 bp just in the past 1-1/2 weeks and posted a new 4-year high of 2.85% last Friday. The T-note yield was driven higher last Friday by the stronger-than-expected Jan payroll report of +200,000 and by continued concern about inflation pressures and Fed tightening.

The 10-year breakeven rate last Friday rose to a new 3-1/2 year high of 2.14%, illustrating that 10-year inflation expectations have now moved decisively above the Fed’s +2.0% inflation target. Meanwhile, the market is discounting +67.5 bp worth of Fed tightening in 2018, the largest amount yet and just below the Fed’s forecast for +75 bp worth of tightening in 2018 (i.e., three rate hikes).

The sharp rise in the 10-year T-note yield seen since late-December when Congress passed the tax-cut bill has finally started to take a toll on the stock market. The stock market was already vulnerable to a technical correction due to stretched valuations and the size of the rally seen after the tax-cut bill. The stock market is also displaying some concerns about Washington political strife as the market worries that President Trump might fire Deputy Attorney General Rod Rosenstein and/or Special Counsel Robert Mueller as it comes down to the wire about whether President Trump will be interviewed by the Special Counsel.

Q4 earnings season is now past its peak and is therefore waning as an upside catalyst for stocks. The consensus is for Q4 earnings growth of +13.6%, according to Thomson I/B/E/S. Of the 251 reporting SPX companies, 78% have beaten their consensus, above the long-term average of 64% and the 4-quarter average of 72%.