- Weekly market focus

- FOMC meeting will set near-term market tone

- T-note prices are on the defensive due to the hawkish shift in Fed and inflation expectations

- U.S. stocks remain buoyant

Weekly market focus — The U.S. markets this week will focus on (1) the Tue/Wed FOMC meeting where the FOMC is expected to announce the start date for its balance sheet reduction program, which could be as soon as Oct 1, (2) President Trump’s speech at the UN on Tuesday, (3) any developments in Congress on tax reform as Republicans plan to announce a consensus plan next week (Sep 25 week), (4) this week’s busy U.S. economic schedule and speaking engagements by three Fed officials on Friday, (5) another light earnings week with only seven of the S&P 500 companies scheduled to report, (6) the Treasury’s sale of 10-year TIPS on Thursday, and (7) any new provocations from North Korea.

U.S. weather threats will continue as Hurricane Jose may hit the Northeast U.S. coast later this week and as Hurricane Maria is expected to threaten the Caribbean islands this week. Tropical Depression Lee is a new storm in the mid-Atlantic that bears watching.

The main focus in Europe will be this coming Sunday’s German national election. German Chancellor Merkel is overwhelmingly favored to keep her job with the betting odds at 95% (1/20), according to Oddschecker.com. Friday’s Eurozone Sep Markit PMI is expected to show a small -0.2 point decline to 57.2 after Aug’s +0.8 point increase to 57.4. The markets expect the ECB at its next meeting on Oct 26 to announce its 2018 QE tapering plans.

In Asia, the main focus will be on Thursday’s BOJ meeting, although that meeting is not expected to produce any policy change. Japanese politics will be in focus after reports that Japanese Prime Minister Abe is considering calling a snap election for late October due to the recent recovery in his public support. There are no major Chinese economic reports this week where the main focus remains on the run-up the twice-a-decade Party Congress that is due to begin on Oct 18.

FOMC meeting will set near-term market tone — There is a nearly unanimous market consensus that the FOMC at its meeting this Tue/Wed will not raise interest rates but will announce a start date for its balance sheet reduction program. The odds of a Fed rate hike this week are very small at 14%, according to the October federal funds futures contract.

The most logical start date for the Fed’s balance sheet reduction program is Oct 1 so that the program is synchronized with calendar quarters. The FOMC has already announced that the program will cap security roll-offs at $10 billion per month to begin. The cap will then rise by $10 billion every three months until the maximum cap of $50 billion per month is reached.

The markets will be closely watching (1) any change in the FOMC’s interest rate guidance in its post-meeting statement, (2) any dovish shift in the Fed-dot forecasts, and (3) comments by Fed Chair Yellen in her post-meeting press conference. Any shift in the outlook for Fed rate hikes stemming from this week’s FOMC meeting will have a strong impact on the T-note prices and the dollar and to a lesser extent on the U.S. stock market.

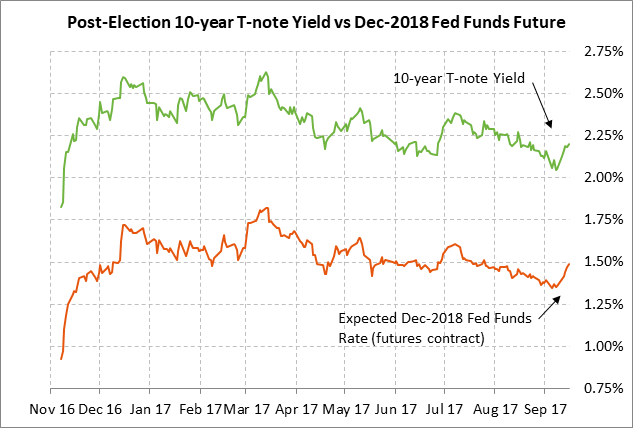

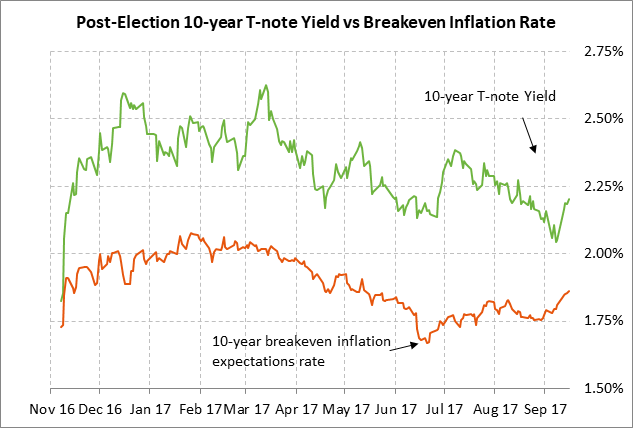

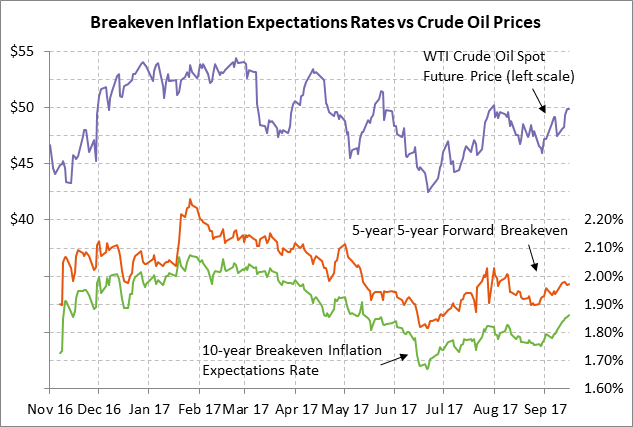

T-note prices are on the defensive due to the hawkish shift in Fed and inflation expectations — The 10-year T-note yield last week rose sharply from the 10-month low of 2.01% posted on Sep 8, closing last week up +15 bp at 2.20%. Last week’s surge in the 10-year T-note yield was due to (1) the sharp 2-week rise in the 10-year breakeven inflation expectations rate by about 10 bp to a 4-month high of 1.87%, and (2) increased expectations for a Fed rate hike by year-end due to heightened inflation expectations and the less-than-expected damage from Hurricane Irma.

Expectations for a Fed rate hike by year-end increased to a 1-3/4 month high of 60% last Friday from as low as 38% two weeks ago just before Irma hit Florida. The rise in the 10-year breakeven inflation expectations rate was due in large part to the recovery in crude oil prices after the initial hit on Hurricane Harvey. Oct WTI crude oil prices last week rallied to a new 3-3/4 month nearest-futures high as (1) Gulf refineries reopened sooner than expected after Hurricane Harvey, and (2) Saudi Arabia already started talking about extending the production cut past Q1-2018.

The T-note market this week will take its cue from the Tue/Wed FOMC meeting and from inflation expectations. This week’s U.S. economic data is mostly for August and will show some impact from Hurricane Harvey, making it more difficult to assess the underlying strength of the economy. The T-note market seems fully braced for the FOMC’s expected announcement on Wednesday of the start date of its balance sheet reduction program, which could be as soon as Oct 1.

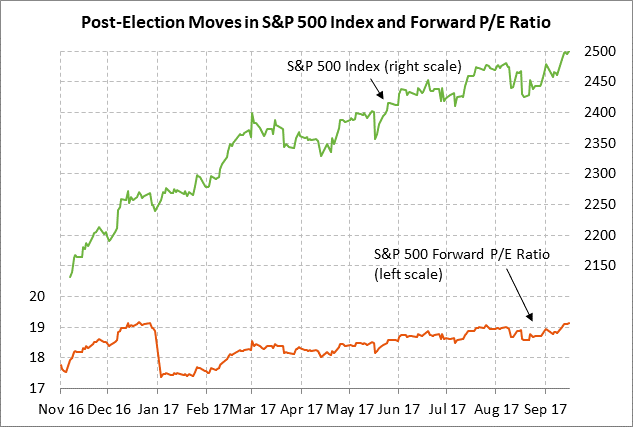

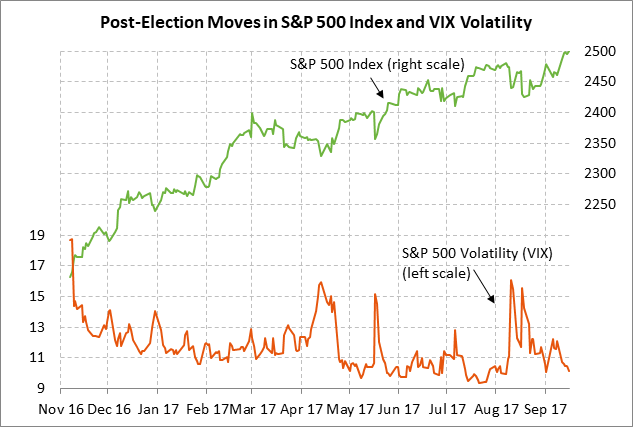

U.S. stocks remain buoyant — The S&P 500 index last Friday edged to a new record high. The U.S. stock market continues to accentuate the positive and shake off negative factors such as (1) North Korea tensions, (2) the recent rise in expectations for a Fed rate hike by year-end, and (3) stretched valuations. The stock market is seeing support from (1) generally dovish expectations for Fed policy, (2) supportive U.S. economic data even in the face of hurricane damage, and (3) expectations for another strong earnings season when Q3 earnings season begins in about three weeks. The forward P/E for the S&P 500 index last Friday rose to 19.13, which was just slightly below the record high of 19.17 posted in Dec 2017. The forward P/E is well above the 5-year average of 16.6 and the 10-year average of 15.3. Last Friday’s rally in SPX to a record high caused the VIX index to fall to 2-week low of 10.17.