- Stock market is looking toppy with tech stocks having another bad day

- Is the euro just getting started on a QE tapering rally?

- 7-year T-note auction to yield near 2.05%

- Weekly EIA report

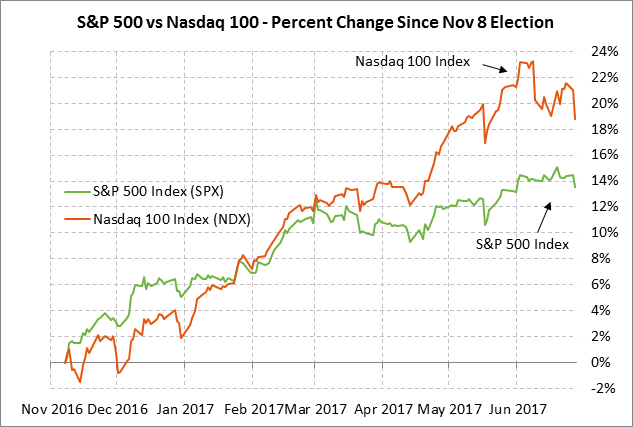

Stock market is looking toppy with tech stocks having another bad day — The stock market on Tuesday was looking a little toppy with the Nasdaq 100 index falling sharply by -1.83%. That helped to drag the S&P 500 index down to a 1-1/2 week low and a close of -0.81%. The Nasdaq 100 gave up all of its gains seen in the previous 6 sessions and needs to sell off by only another -0.67% to take out the 1-month low posted on June 12.

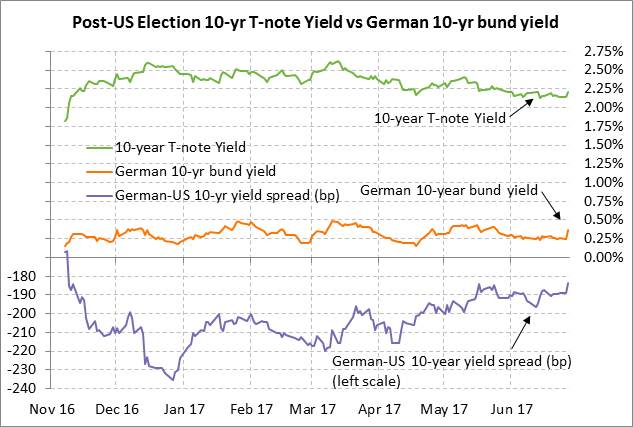

Tuesday’s U.S. stock market sell-off was sparked by (1) a sharp sell-off in the FANG and related tech stocks, (2) references to high stock market valuation by Yellen and Fischer that provide another basis for the FOMC to justify further rate hikes, (3) news that Senator Majority leader McConnell was forced to delay a vote on his health insurance bill until after the July 4 recess, which indicates reduced chances for Republican passage of a health insurance bill and by extension reduced chances for a large Republican tax reform bill, and (4) Tuesday’s sharp +12 bp rise in German 10-year bund yields on hawkish comments by ECB President Draghi, which helped push U.S. 10-year T-note yields higher by +7.0 bp to 2.205%.

Is the euro just getting started on a QE tapering rally? — EUR/USD on Tuesday rallied sharply by +1.40% and posted a new 10-month high. Meanwhile, the 10-year German bund yield soared by +12.5 bp to close at a 1-month high of 0.370%. Those moves were sparked by comments from ECB President Draghi suggesting that ECB officials might be starting to lay the groundwork for QE tapering.

Mr. Draghi on Tuesday essentially said that tighter policy parameters may be necessary to keep policy “unchanged” as the economy recovers. Specifically, Mr. Draghi said, “As the economy continues to recover, constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments — not in order to tighten the policy stance, but to keep it broadly unchanged.”

Mr. Draghi made several other mildly hawkish comments by saying that “All the signs now point to a strengthening and broadening recovery in the euro area.” On inflation, he said that reflationary forces have replaced deflationary forces” and that the ECB can look through the mostly temporary factors that are currently depressing inflation.

Mr. Draghi’s comments suggested a change in tone where the ECB may be starting to look past the current weakness in inflation and towards the need to tighten up policy to address the stronger economy. The markets should not be surprised by such statements since the market consensus is that the ECB will announce as soon as its September meeting that it will taper its QE program during the first half of 2018. Yesterday’s sharp upmove in the euro and bund yields, however, suggested that the market was caught off guard and has not yet fully discounted a QE tapering announcement as soon as September.

Indeed, the reaction of the dollar to the Fed’s 2014 QE3 tapering suggests that the euro could be poised for a big rally if the ECB is in fact moving towards QE tapering. The dollar index soared from mid-2014 through early 2015 as the Fed tapered QE3 during Jan-Oct 2014. The dollar index since the end of QE3 has shown little additional net gain despite three Fed interest rate hikes. The reminder from the dollar’s 2014/15 rally, as well as the 2013 taper tantrum episode, is that the big market moves typically come well ahead of the actual policy moves. That suggests that the euro could be in for big gains as the ECB’s QE tapering draws closer.

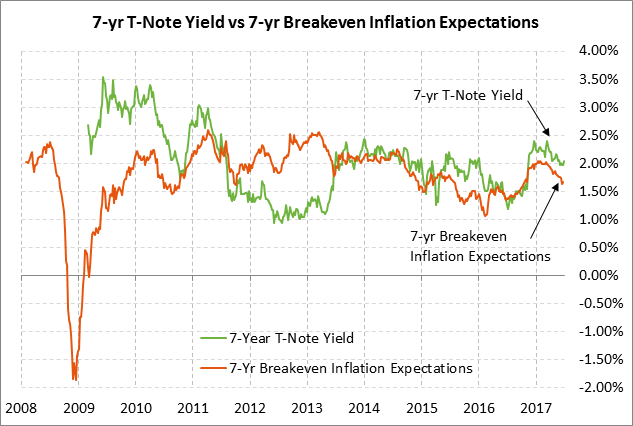

7-year T-note auction to yield near 2.05% — The Treasury today will conclude this week’s $101 billion T-note package by selling $13 billion of 2-year floating-rate notes and $28 billion of 7-year T-notes. Today’s 7-year T-note issue was trading at 2.05% in when-issued trading late Tuesday afternoon, which equates to an inflation-adjusted yield of 0.37% against the current 7-year breakeven rate inflation expectations rate of 1.68%.

The 7-year T-note yield has fallen by -40 bp from December’s post-election peak of 2.45% on the same factors that have driven the rest of the Treasury curve lower, including (1) reduced inflation expectations, (2) soft U.S. economic data, and (3) the slow Republican agenda. However, the 7-year yield is still up by +51 bp from the pre-election level of 1.54% with support coming mainly from the Fed’s +75 bp overall rate hike seen since December.

The 12-auction averages for the 7-year are as follows: 2.53 bid cover ratio, $12 million in non-competitive bids, 4.6 bp tail to the median yield, 19.8 bp tail to the low yield, and 42% taken at the high yield. The 7-year T-note is tied with the 30-year TIPS as the second most popular Treasury coupon security among foreign investors and central banks behind the first-place 10-year TIPS. Indirect bidders, a proxy for foreign buyers, have taken an average of 66.5% of the last twelve 7-year T-note auctions, which is well above the average of 60.2% for all recent Treasury coupon auctions.

Weekly EIA report — The market consensus for today’s weekly EIA report is for a -2.0 million bbl decline in U.S. crude oil inventories, an unchanged level of gasoline inventories, a +350,000 bbl rise in distillate inventories, and a -0.3 point decline in the refinery utilization rate. Crude oil prices after Tuesday’s close fell sharply from the day’s higher close after the weekly API report showed that U.S. crude oil inventories rose by +851,000 bbls. U.S. crude oil inventories remain in a glut at +26.1% above their 5-year average, although that is at least tighter than the +40% level seen as recently as February.