- Yellen speaks in London today

- GDPNow’s cut in its Q2 GDP forecast to +2.9% illustrates the impact of the recent weak economic data

- U.S. consumer confidence expected to give back a bit more of the post-election surge

- U.S. home prices expected to extend the recent surge

- 5-year T-note auction to yield near 1.76%

Yellen speaks in London today — Fed Chair Yellen speaks today at 1 PM ET in London on the topic of global economic issues at an event at the British Academy. There will be an audience Q&A following her remarks. The markets will be watching for any fresh hints on the timing of the Fed’s next rate hike or the beginning of the Fed’s balance sheet reduction program. The markets will also be watching to see if Ms. Yellen makes any comments about the recent soft U.S. economic and inflation data, which she has largely written off thus far as transitory.

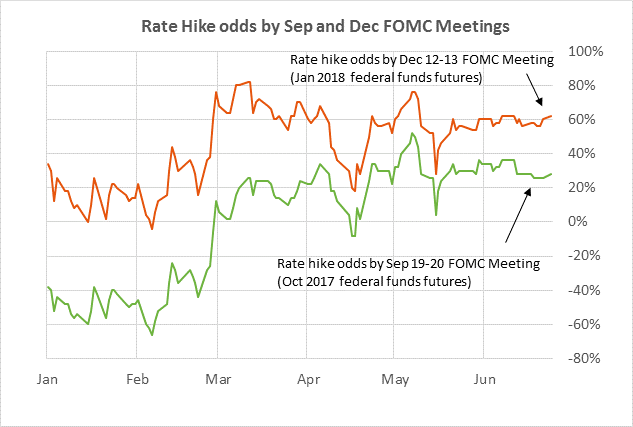

There has been little change over the past month in market expectations for future Fed rate hikes. The market is currently discounting the chances for the Fed’s next rate hike at 30% by September and 62% by December, according to the federal funds futures market. Meanwhile, the Fed has only said so far that it will begin its balance sheet reduction program “later this year” but that could turn out to be as soon as Oct 1 with an announcement at the September FOMC meeting. The Fed has already announced that its balance sheet reduction program will begin with a $10 billion per month cap that will rise by $10 billion per quarter until the maximum cap of $50 billion per month is reached.

GDPNow’s cut in its Q2 GDP forecast to +2.9% illustrates the impact of the recent weak economic data — The Atlanta Fed’s GDPNow on Monday cut its forecast for Q2 GDP to +2.9% from +3.0% due to Monday’s weak May durable goods orders report of -1.1% and +0.1% ex-transportation. That Q2 GDP forecast of +2.9% is sharply lower than the +4.9% forecast that GDPNow started out with on May 1. The Bloomberg survey consensus for Q2 GDP is currently at +3.0%, close to the GDPNow forecast.

The steady reduction in GDPNow’s Q2 GDP forecast has been due to a stream of weaker-than-expected U.S. economic data. Indeed, the Bloomberg U.S. Economic Surprise Index has plunged to a 6-month low of -0.131 from as high as +0.7 in late March, illustrating how the U.S. economic data has substantially under-performance market expectations. U.S. GDP growth was weak at +1.2% in Q1 mainly due to weak consumer spending and some of that weakness is continuing into Q2.

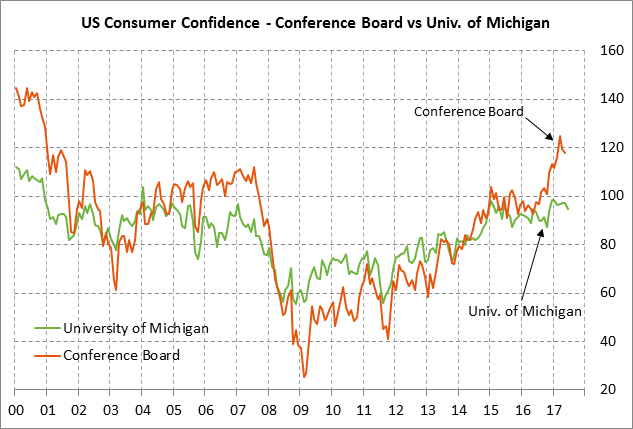

U.S. consumer confidence expected to give back a bit more of the post-election surge — The market consensus for today’s June Conference Board U.S. consumer confidence index is for a -1.9 point decline to 116.0, adding to May’s -1.5 point decline to 117.9. The University of Michigan’s U.S. consumer sentiment index for early June has already been reported at -2.6 points to 94.5, which is partially behind expectations for a decline in today’s Conference Board index.

The Conference Board’s U.S. consumer confidence index moved sharply higher by +24.1 points after the November election and posted a 16-1/2 year high of 124.90 in March. From that March high, however, the index then fell modestly by a total of -7.0 points in April-May, giving back about one-third of the post-election surge.

U.S. consumer confidence continues to see support from record highs in the stock market, rising consumer income and wealth, the strong labor market, and low gasoline prices. Negative factors for consumer confidence include slow wage growth and Washington political uncertainty. Despite the high level of confidence, consumers have been stingy in their spending so far this year. Retail sales have seen only a slight +0.1% net increase since February.

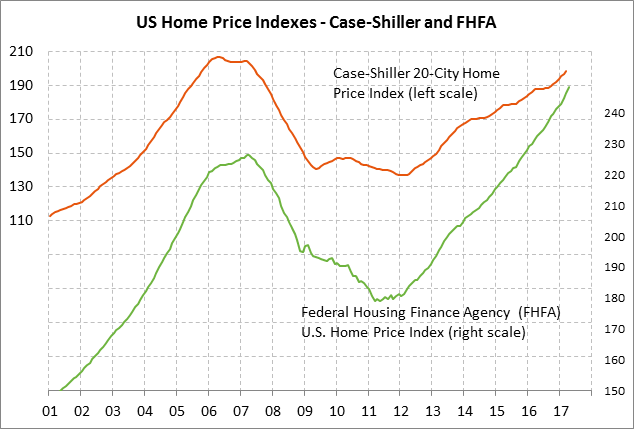

U.S. home prices expected to extend the recent surge — The market consensus is for today’s Apr S&P CoreLogic Composite-20 home price index to show another solid gain of +0.5% m/m and +5.9% y/y. The index showed a lull in the middle of last year but has risen sharply with an average monthly gain of +0.8% since Sep 2016. The index has now soared by +44.8% from the housing-bust low and needs to move higher by only another +4.1% to match the record high posted in April 2006.

U.S. home prices continue to move steadily higher due to the combination of strong demand and tight supplies. U.S. existing home sales are near a 10-year high and there are only 4.2 months worth of homes available on the market, well below the 7-8 month level that the National Association of Realtors says is consistent with steady home prices. The median price of an existing home just reached a record high of $252,800 in May.

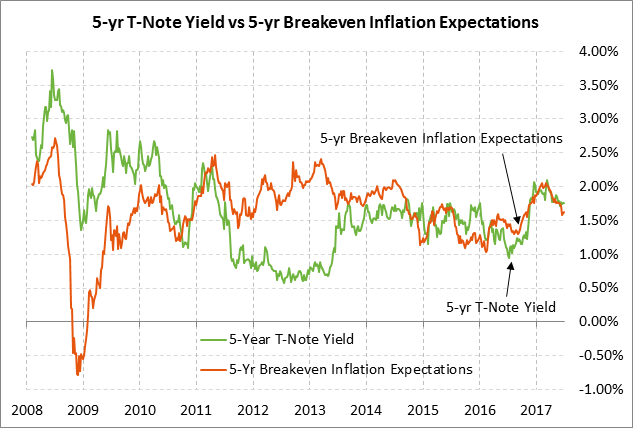

5-year T-note auction to yield near 1.76% — The Treasury today will sell $34 billion of 5-year T-notes. The Treasury will then conclude this week’s $101 billion T-note package on Wednesday by selling $13 billion of 2-year floating-rate notes and $28 billion of 7-year T-notes. The benchmark 5-year T-note late Monday was trading at 1.76%, which translates to an inflation-adjusted yield of 0.14% against the current 5-year breakeven inflation expectations rate of 1.62%.

The 12-auction averages for the 5-year are as follows: 2.43 bid cover ratio, $44 million in non-competitive bids, 5.0 bp tail to the median yield, 13.0 bp tail to the low yield, and 42% taken at the high yield. The 5-year T-note is moderately popular among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.4% of the last twelve 5-year T-note auctions, which is moderately above the average of 60.1% of all recent Treasury coupon auctions.