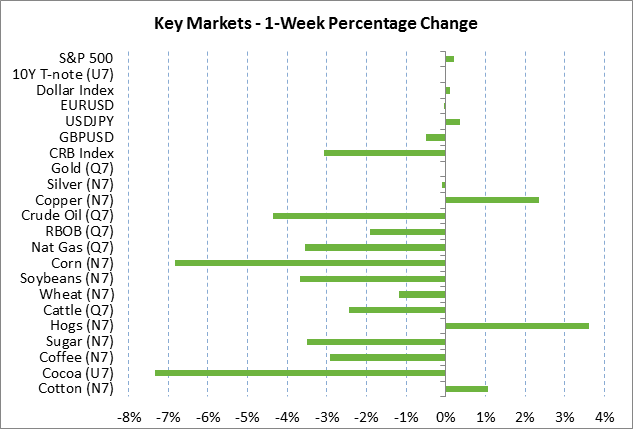

- Weekly U.S. market focus

- Yellen comments on Tuesday headline another busy week for Fedspeak

- Washington focus is on Senate health insurance bill

- U.S. durable goods orders expected to be mixed

- 2-year T-note auction

- T-notes see continued support from tepid inflation expectations

- Stocks see support from earnings expectations and increased tax-cut chances

Weekly U.S. market focus — The U.S. markets this week will focus on (1) Fed Chair Yellen’s comments on Tuesday in London and comments by other Fed officials this week, (2) Washington events as Senate Republicans try to pass a health insurance bill and as the Trump administration promotes U.S. energy this week, (3) whether this week’s batch of U.S. economic data improves after recent disappointments, (4) the Treasury’s sale of $101 billion of T-notes on Monday through Wednesday, (5) another light earnings week with reports from 12 of the S&P 500 companies (including Monsanto and General Mills on Wednesday, and Walgreens and NIKE on Thursday), and (6) oil prices, which continue to trade defensively just mildly above last Wednesday’s 10-month nearest-futures low.

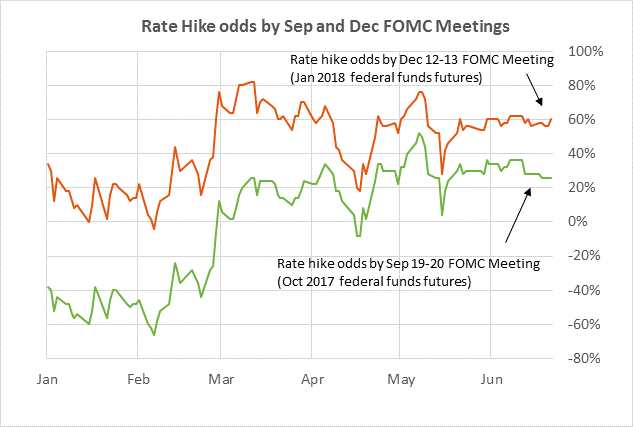

Yellen comments on Tuesday headline another busy week for Fedspeak — There will be five Fed speaking engagements this week including Tuesday’s comments by Fed Chair Yellen at an event in London. The markets are waiting for any new hints on the timing of the Fed’s next rate hike and its balance sheet reduction plan. Fed officials last week made a variety of comments that generally supported the Fed’s rate-hike and balance sheet plans, although some concerns were expressed about weaker inflation. There was little change last week in expectations for future Fed rate hikes. The market is currently discounting the odds for the Fed’s next rate hike at 26% by September and 60% by December, according to the federal funds futures market.

Washington focus is on Senate health insurance bill — The Washington focus this week will mainly be on the Senate’s consideration of the health insurance bill that was unveiled last week. The CBO is expected to release its scoring on the bill early this week. Senate Majority leader McConnell is trying to hold a vote on the bill by this Friday before legislators leave for next week’s July 4th recess. If the Senate can pass the health insurance bill by late this week, then House Speaker Ryan’s goal would be to get the Senate bill approved by the House by the end of July before legislators leave for their August recess.

Congressional Republican leaders still face an uphill battle on getting a health insurance bill approved and sent to President Trump for his signature. The betting odds for the passage of a health insurance bill by year-end that includes repealing the individual mandate are currently at 49%, up 10 points from a week earlier, according to PredictIt.org. Passage of a health insurance bill would improve the chances for a tax cut bill. The betting odds for a cut in the corporate tax rate by year-end are currently at 43%, up from the low of 30% seen in early-June, according to PredictIt.org.

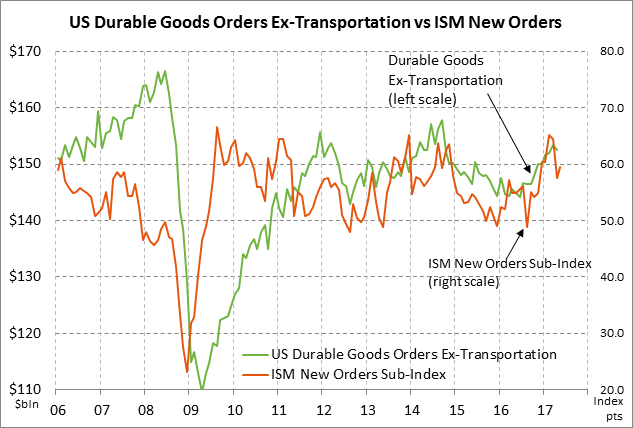

U.S. durable goods orders expected to be mixed — The market consensus for today’s May durable goods orders is for a report of -0.6% and +0.4% ex-transportation, which would be better than April’s report of -0.8% and -0.5% ex-transportation. The consensus for May capital goods orders non-defense ex-aircraft, a proxy for capital spending, is for a small increase of +0.3% after April’s +0.1% report. Durable goods orders ex-transportation since the election have improved substantially and were up +4.9% y/y in April. The ISM manufacturing new orders sub-index was strong at 59.5 in May, which indicates that manufacturing executives are still seeing a substantial improvement in order flow. The U.S. manufacturing sector is seeing support from the oil sector and from a stronger export outlook due to the weaker dollar seen this year, but a weaker auto sector has been a drag on manufacturing.

2-year T-note auction — The Treasury today will sell $26 billion of 2-year T-notes. The Treasury will then continue this week’s $101 billion T-note package by selling $34 billion of 5-year T-notes on Tuesday, and then $13 billion of 2-year floating-rate notes and $28 billion of 7-year T-notes on Wednesday. The benchmark 2-year T-note last Friday closed at 1.34%, which translates to an inflation-adjusted yield of 0.10% against the current 2-year breakeven inflation expectations rate of 1.24%.

The 12-auction averages for the 2-year are as follows: 2.70 bid cover ratio, $163 million in non-competitive bids, 4.3 bp tail to the median yield, 23.5 bp tail to the low yield, and 56% taken at the high yield. The 2-year T-note is the least popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of only 44.2% of the last twelve 2-year T-note auctions, which is well below the average of 60.1% of all recent Treasury coupon auctions.

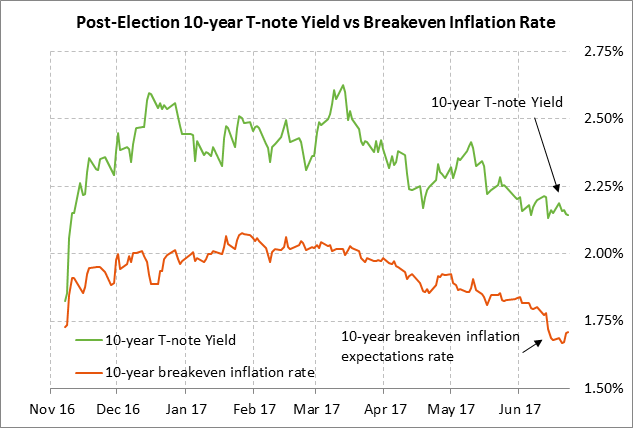

T-notes see continued support from tepid inflation expectations — The 10-year T-note yield last week closed little changed at 2.14% after moving sideways just mildly above the mid-June 7-1/2 month low of 2.10%. T-note prices continue to see support mainly from reduced inflation expectations, which fell to an 8-month low of 1.66% last Wednesday but then rebounded higher to 1.71% by Friday. Inflation expectations have been falling due to the plunge in oil prices and weaker U.S. inflation statistics. Looking ahead, the T-note market is mainly focused on inflation expectations, the U.S. economic data, and the timing of the Fed’s next rate hike and its balance sheet reduction program.

Stocks see support from earnings expectations and increased tax-cut chances — The S&P 500 index last Monday rallied to a new record high but then fell back on some mild consolidation and closed the week just slightly higher by +0.21%. Stocks are seeing support from (1) low U.S. interest rates and reduced fear of Fed rate hikes, (2) increased hopes for a corporate tax cut with the Senate making some progress on health care, and (3) expectations for a positive Q2 earnings season. Bearish factors include the recent weakness in tech and oil stocks.