- Fed’s Williams may have floated a balance-sheet trial balloon

- Beige Book will detail U.S. regional economic activity

- Chicago PMI expected to follow the recent slide in U.S. manufacturing confidence

- Pending home sales report is expected to indicate continued strength in existing home sales

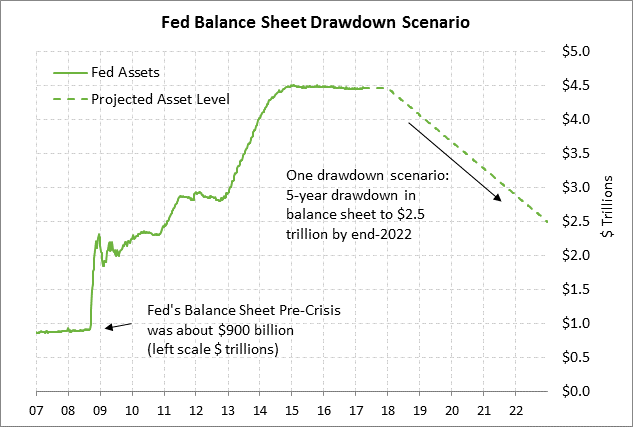

Fed’s Williams may have floated a balance-sheet trial balloon — The next FOMC meeting is now only two weeks away on June 13-14. The market is discounting about a 90% chance for a rate hike at that meeting. However, the main question is whether the Fed at that June meeting will offer any details about its balance sheet discussions.

San Francisco Fed President Williams on Monday in an interview with Bloomberg mentioned a 5-year balance sheet roll-off program that takes the balance sheet down to $2.0-2.5 trillion “or something like that.” It is not clear whether Mr. Williams was offering his own parameters, or whether he was mentioning numbers he heard at the May 2-3 FOMC meeting when the Fed staff presented their balance sheet roll-off plan. Mr. Williams may have been purposely mentioning some balance sheet numbers so the Fed could gauge market reaction. If his comments did represent a trial balloon, the markets on Tuesday did not seem to express any particular worry about the parameters he mentioned.

In any case, a 5-year balance sheet roll-off plan that ends up at $2.5 trillion (from the current $4.5 trillion) would imply a $33 billion per month roll-off ($2 trillion divided by 60 months). Meanwhile, a larger 5-year roll-off plan that ends up at $2.0 trillion would imply a $42 billion per month roll-off ($2.5 trillion divided by 60 months).

However, the FOMC in its May 2-3 meeting minutes said the plan under consideration would start out at a low monthly roll-off amount and then ramp up every 3 months until it reaches the full-phase in amount. A Fed roll-off plan could therefore start later this year as low as $2-10 billion per month, and then ramp up over a year or so to $35-45 billion per month.

The Fed could easily reduce those monthly roll-off amounts by extending the plan beyond five years or by deciding that they don’t need to reduce the balance sheet to as low as $2.0-2.5 trillion. Former Fed Chair Bernanke in an article entitled “Shrinking the Fed’s balance sheet” released in Jan 2017 said, it’s not unreasonable to argue that the optimal size of the Fed’s balance sheet is currently greater than $2.5 trillion and may reach even $4 trillion or more over the next decade.” He added, “In a sense, the U.S. economy is ‘growing into’ the Fed’s $4.5 trillion balance sheet, reducing the need for rapid shrinkage over the next few years.”

The T-note market has so far shown a muted reaction to the Fed’s talk about its balance sheet reduction plan. We do not expect T-note yields to see a taper-tantrum-type surge caused by the balance sheet plan because (1) the Fed is planning to start the program with a small test run, and (2) the Fed is starting early in prepping the markets to fully anticipate the balance sheet roll-off plan and avoid any surprises. The markets can probably expect more trial balloons from Fed officials in coming weeks as the Fed tries to gauge market reaction to various roll-off parameters.

Beige Book will detail U.S. regional economic activity — The markets will be watching today’s Fed Beige Book for confirmation that the U.S. economy is regaining some momentum after the poor first quarter. The Fed’s last Beige Book report, released on April 19, said that the pace of growth in the twelve Fed districts between mid-February and end-March was equally split between “modest and moderate.” Regarding U.S. consumers, the Beige Book said, “Consumer spending varied as reports of stronger light vehicle sales were accompanied by somewhat softer readings in non-auto retail spending.”

Chicago PMI expected to follow the recent slide in U.S. manufacturing confidence — The market consensus for today’s May Chicago PMI is for a -1.3 point decline to 57.0, more than giving back April’s +0.6 point increase to 58.3. A decline in today’s report would not be surprising since the Chicago PMI index has risen for the last three consecutive months by a total of +8.0 points to post a new 2-1/4 year high of 58.3 in April.

On the national front, U.S. manufacturing confidence has been sliding over the last several months due to (1) reduced hopes for large Republican tax cut and infrastructure programs, and (2) weaker prospects for the U.S. auto industry. The market is expecting Thursday’s April U.S. ISM manufacturing index to show a small -0.2 point decline to 54.6, which would bring the 3-month decline to a total of -3.1 points from February’s 2-3/4 month high of 57.5. The Markit U.S. manufacturing PMI index has fallen for the last four consecutive reporting months (Feb-May) by a total of -2.5 points to an 8-month low of 52.5 in May.

Even though manufacturing confidence has faded somewhat in the past several months, the current ISM index level of 54.8 remains solidly above the 50.0 expansion-contraction level. U.S. manufacturing confidence still has solid support from (1) expectations for strong U.S. economic growth in coming quarters, (2) optimism about improved global economic growth, and (3) the decline in the dollar index since January, which helps boost the competitiveness of U.S. exports.

Pending home sales report is expected to indicate continued strength in existing home sales — The market consensus for today’s April pending home sales report is for a small +0.4% m/m increase, recovering half of March’s -0.8% m/m decline. The pending home sales report is a leading indicator for the existing home sales series since pending home sales contracts generally lead closed-home-sales on a 1-2 month basis. U.S. existing home sales remain in very strong shape despite a tight supply of homes available for sale. April’s existing home sales level of 5.57 million was only -2.3% below the 10-year high of 5.70 million units posted in March.