- U.S. stock volatility drops to a 10-1/2 year low after Macron victory

- JOLTS job openings expected to remain strong

- Treasury refunding operation begins with today’s 3-year T-note auction

- U.S. Q1 earnings growth improves to +14.7%

U.S. stock volatility drops to a 10-1/2 year low after Macron victory — Volatility in the U.S. markets on Monday dropped following Emmanuel Macron’s victory in Sunday’s French presidential election, which removed the threat of a Frexit referendum vote if Marine Le Pen had won. The European markets had already priced in the Macron victory as seen by the fact that the Euro Stoxx 50 index on Monday closed -0.46% lower and EUR/USD closed -0.67% lower. The S&P 500 index on Monday closed unchanged after earlier edging to a new record intra-day high.

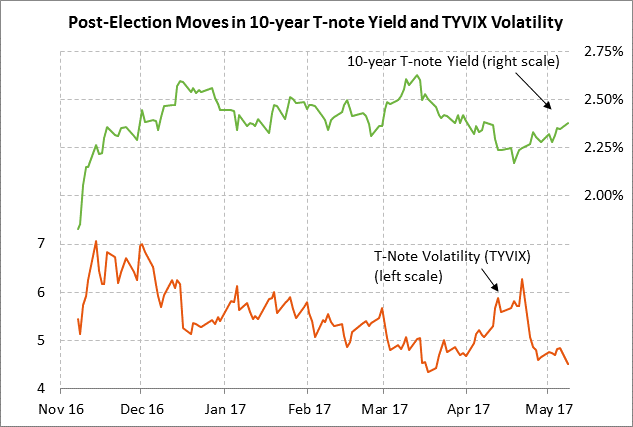

The VIX index on Monday fell to a daily low of 9.67% and closed the day at 9.77%. The VIX on Monday’s low of 9.67% fell to a 10-1/2 year on an intra-day basis, the lowest level since December 2006. Not far below current levels, the 23-1/2 year low for the VIX is 9.39% (posted in December 2006) and the record low for the series (which has data back to 1992) is 8.89% (posted in December 1993). Meanwhile, the TYVIX index on Monday fell to a 7-week low of 4.52%, illustrating expectations for lower volatility in the 10-year T-note futures market as well.

Volatility in the U.S. stock and bond markets is low since both the economy and earnings are supporting the stock market and since the market feels it has a good handle on what the Fed will do this year on interest rates. While the volatility outlook remains calm for the time being, however, there is still the chance for some new developments that could spark some renewed volatility.

Those potential new volatility factors include (1) any change in the outlook for Fed rate hikes or any unexpected news of the Fed’s balance sheet deliberations, (2) any substantial change in the growth rate of the U.S. economy or in the inflation outlook, (3) the possibility of a melt-down in oil prices if OPEC doesn’t take sufficient support action, (4) Washington developments such as trade moves or legislative developments on health care and taxes, (5) an even sharper sell-off in the Chinese stock and bond markets on the government’s leverage crackdown, (6) geopolitical hot-spots such as North Korea, and (7) the fiscal cliff this fall when Congress must pass a fiscal 2018 spending bill by Sep 30 and a debt ceiling increase by Oct/Nov.

JOLTS job openings expected to remain strong — The consensus is for today’s Mar JOLTS job openings report to show a small decline of -5,000 to 5.738 million following Feb’s strong increase of +118,000 to 5.743 million. The JOLTS series remains in strong shape at just above the 12-month trend average of 5.65 million, indicating that there are plenty of job openings in the U.S. economy that need to be filled.

Last Friday’s April payroll report of +211,000 was a relief since it indicated that hiring rebounded in April after the weak report of +79,000 seen in March that was largely caused by weather-related issues. A strong JOLTS report today would further bolster confidence that the U.S. labor market is continuing to grow at a steady pace.

Treasury refunding operation begins with today’s 3-year T-note auction — The Treasury this week will conduct its $62 billion quarterly refunding operation by selling $24 billion of 3-year T-notes today, $23 billion of 10-year T-notes on Wednesday, and $15 billion of 30-year T-bonds on Thursday. Both the 10-year and 30-year auctions will involve new securities as opposed to reopenings of existing issues. Today’s 3-year T-note was trading at 1.55% in when-issued trading late yesterday afternoon, which translates to an inflation-adjusted yield of -0.09% against the current 3-year breakeven inflation expectations rate of 1.64%.

The 12-auction averages for the 3-year are as follows: 2.79 bid cover ratio, $48 million in non-competitive bids, 4.4 bp tail to the median yield, 15.7 bp tail to the low yield, and 54% taken at the high yield. The 3-year is the second least popular security among foreign investors and central banks behind the 2-year T-note. Indirect bidders, a proxy for foreign buying, have taken an average of only 51.8% of the last twelve 3-year T-note auctions, well below the average of 60.0% for all recent Treasury coupon auctions.

U.S. Q1 earnings growth improves to +14.7% — Q1 earnings season has been very favorable and has been a major factor supporting stock prices. Moreover, earnings growth is expected to remain strong with SPX earnings growth of +11.3% in 2017 and +11.9% in 2018. The current forward P/E ratio of 18.5 remains high relative to the 5-year average of 16.3 and the 10-year average of 15.2. However, the good news is that strong earnings growth will at least boost the denominator in the P/E ratio and perhaps keep the P/E in reasonable shape.

There are 33 of the S&P 500 companies that are scheduled to report during the remainder of this week as Q1 earnings season winds down. The market consensus for Q1 SPX earnings growth is now +14.7% y/y (+10.5% ex-energy), which is substantially stronger than expectations of +10.2% seen on April 1 before the earnings season began, according to surveys by Thomson Reuters I/B/E/S. That Q1 consensus of +14.7% is a blended rate of already-reported earnings combined with the consensus for yet-to-be-released figures.

Of the 412 companies in the S&P 500 that have reported Q1 earnings so far, 75.2% beat the consensus, which is substantially better than the long-term average of 64% and the 4-quarter average of 71%, according to Thomson data. Performance was favorable on a revenue basis as well with 63.4% of reporting companies beating the revenue consensus, better than the long-term average of 59% and the 4-quarter average of 53%.