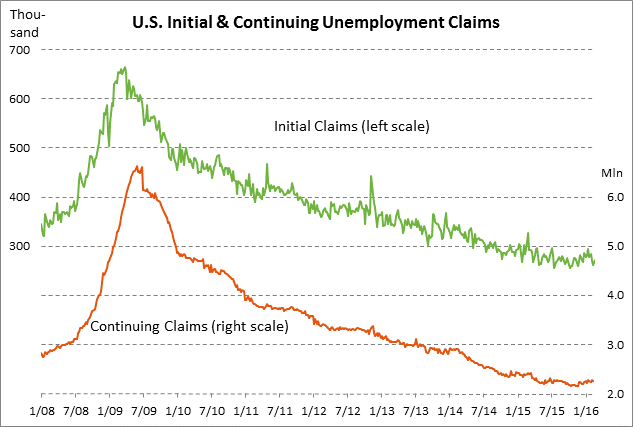

- U.S. initial unemployment claims are near a 42-year low, indicating no increase in layoffs despite recent turmoil

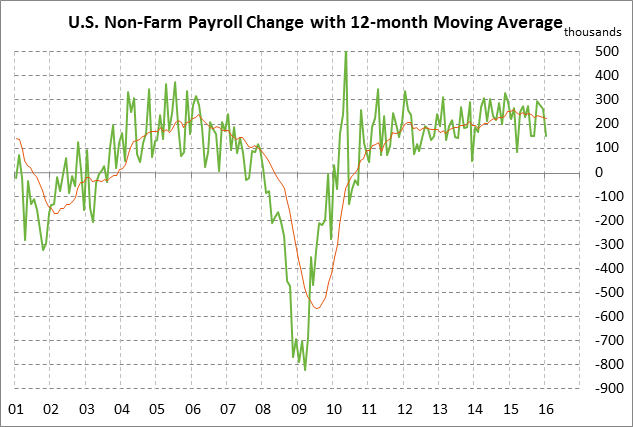

- Friday’s payroll report is expected to show an improvement from Jan’s poor report

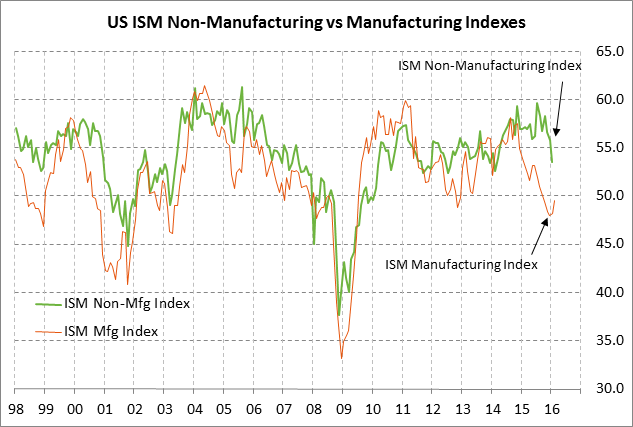

- ISM non-manufacturing PMI expected to extend its 6-month plunge

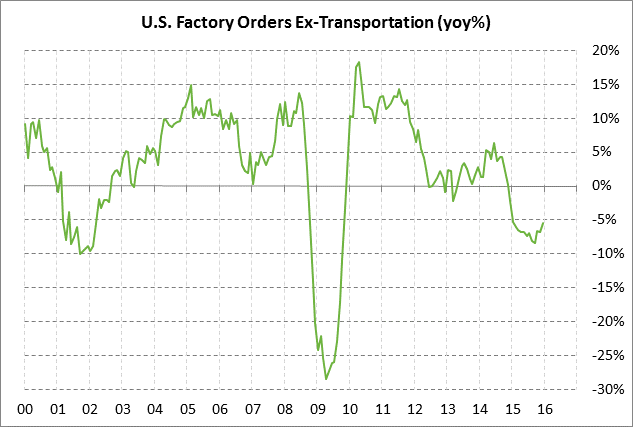

- Factory orders expected to show a solid increase

U.S. initial unemployment claims are near a 42-year low, indicating no increase in layoffs despite recent turmoil — The initial unemployment claims series is currently only +17,000 above the 42-year low of 255,000 posted in July 2015. This indicates that the financial market turmoil seen so far this year has not yet led to any sustained increase in layoffs and suggests that businesses are shrugging off the recent turmoil. The continuing claims series is moderately above October’s 15-year low of 2.146 million by +107,000.

The market consensus is for small declines in today’s unemployment claims report. Specifically, the market is expecting today’s initial unemployment claims to show a -2,000 decline to 270,000 (after last week’s +10,000 to 272,000) and continuing claims to show a -3,000 decline to 2.250 million (after last week’s -19,000 to 2.253 million).

Friday’s payroll report is expected to show an improvement from Jan’s poor report — On the labor front, the market is mainly looking ahead to Friday’s Feb unemployment report. The market consensus is that Feb payrolls will improve to +195,000 from January’s weak report of +151,000. However, the expected Feb payroll report of +195,000 would still be well below the 2015 monthly average increase of +228,000. Moreover, the expected 2-month Jan-Feb average of +173,000 would be even farther below the 2015 average of +228,000.

Yesterday’s ADP report showed an increase of +214,00, which was better than the market consensus of +185,000. Combined with Jan’s revised report of +193,000, ADP jobs showed an average monthly increase of +204,000 in Jan-Feb, which was very close to the 2015 monthly average increase of +207,000.

Friday’s payroll report will show whether businesses are still hiring at the levels seen in 2015 or whether they are pulling back on hiring to gauge the outcome of the recent overseas turmoil and the U.S. stock market correction. A dip in hiring in early 2015 would obviously be a negative development for consumer confidence, income, and spending, as well as the overall economy. Yet the labor market may be due for some correction considering that U.S. businesses have hired a net 13.6 million people since the jobs trough was posted in early 2010. With the poor U.S. Q4 GDP growth rate of +1.0% and with overseas growth prospects looking dim, U.S. businesses may start curbing their hiring. This is particularly the case since labor productivity growth has been non-existent over the past two years, which means that companies are not getting much bang for their buck from their employees. In addition, weak corporate earnings growth means that companies are under some pressure to reduce labor costs and boost earnings.

Meanwhile, the market consensus is for Friday’s Jan unemployment rate to be unchanged from January at 4.9%. The unemployment rate in January fell to that new 8-year low of 4.9%, which was only +0.2 points above the 4.7% level that the Fed is expecting as its long-run midpoint forecast. The unemployment rate has fallen as sharply as it has in recent years partly because many people have dropped out of the labor market for various reasons. The low unemployment rate, therefore, does not provide any confirmation that the U.S. labor market has returned to health.

ISM non-manufacturing PMI expected to extend its 6-month plunge — The market is expecting today’s Feb ISM non-manufacturing PMI to show a -0.4 point decline to 53.1, adding to January’s sharp -2.3 point decline to 53.5. The ISM non-manufacturing PMI has fallen sharply in 5 of the last 6 months by a total of -6.1 points to post a new 2-year low of 53.5 in January. The index is still above the expansion-contraction level of 50, but the sharp decline seen over the last six months indicates the extent to which business confidence in the non-manufacturing sectors of the U.S. economy has dropped.

Separately, the market is expecting today’s final-Feb Markit U.S. services PMI to be revised higher by +0.2 points to 50.0, which would leave the index down by -3.2 points from Jan rather than down by the preliminary-Feb decline of -3.4 to 49.8. The sharp -3.4 point decline in the Markit index in early-Feb does not bode well for today’s Fed ISM non-manufacturing report. On the brighter side, Tuesday’s +1.3 point increase in the ISM manufacturing PMI to 49.5 was stronger than market expectations and suggested that confidence in the manufacturing sector may have finally bottomed out.

Factory orders expected to show a solid increase — The market consensus is for today’s Jan factory orders report to show a +2.1% increase, recovering somewhat from December’s decline of -2.9% and -0.8% ex-transportation. Expectations for a +2.1% increase in today’s Jan factory orders report are based in part on the recent Jan durable goods orders report, which showed a strong gain of +4.9% and +1.8% ex-transportation. Durable goods orders account for more than half of the factory orders series.

U.S. manufacturing executives in January turned more positive on orders as seen by the fact that the ISM manufacturing new orders sub-index in January rose by +2.7 points to 51.5, climbing back above the expansion-contraction level of 50.0 after spending two months below that level in Nov-Dec. The orders sub-index in February was then unchanged from January’s level of 51.5.