- U.S. ISM manufacturing index expected to inch higher but remain below 50.0

- U.S. vehicle sales expected to regain some strength

- China takes limited monetary stimulus action by cutting reserve ratio in order to avoid sparking new weakness in the yuan

- EIA report

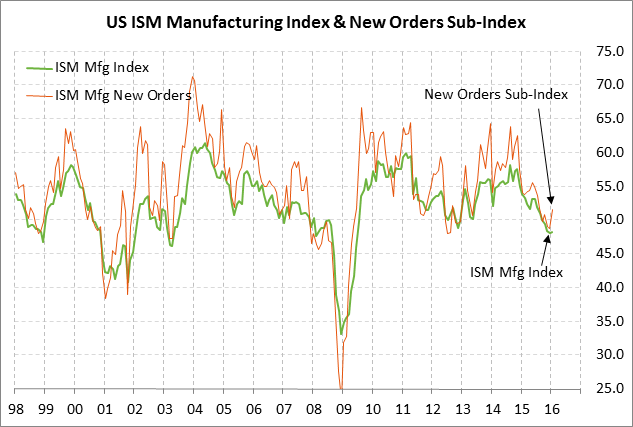

U.S. ISM manufacturing index expected to inch higher but remain below 50.0 — The market is expecting today’s Feb ISM U.S. manufacturing index to edge higher by another +0.3 points to 48.5, adding to Jan’s +0.2 point rise to 48.2. The ISM index fell for six straight months during July-Dec to post a 6-1/2 year low of 48.0 in December. The ISM index then rose by +0.2 point to 48.2 in Jan but remained in contraction territory below 50.0 for the fourth straight month. The fact that the ISM index has been below 50.0 for four straight months illustrates the headwinds that the U.S. manufacturing sector has been facing from the petroleum/mining sector recession and dollar-related weakness in exports.

The prospects for manufacturing activity in February improved based on order activity seen in January. The ISM manufacturing new orders sub-index in January rose fairly sharply by +2.7 points to 51.5 from the 3-1/2 year low of 48.8 posted in December, climbing back above the expansion-contraction level of 50.0 after spending three of the previous four months below 50.0. In addition, last week’s Jan durable goods orders report showed strong increases of +4.9% and +1.8% ex-transportation and capital spending showed a +3.9% increase, the best report in 1-1/2 years.

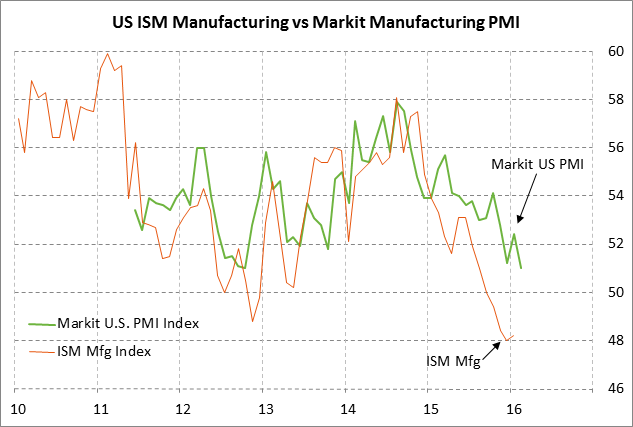

Separately, the market is expecting today’s final-Feb Markit U.S. manufacturing PMI to be revised higher by +0.2 points to 51.2 from the preliminary-Feb level of 51.0. The expected report of 51.2 would leave the index down by -1.2 points from January instead of the preliminary report of a -1.4 point decline. The decline in the Markit index in early February was a negative leading indicator for today’s Feb ISM index, but the ISM index is due for some upside catch-up to the Markit index, which has been able to stay above the 50.0 level thus far while the ISM index sank below 50.0.

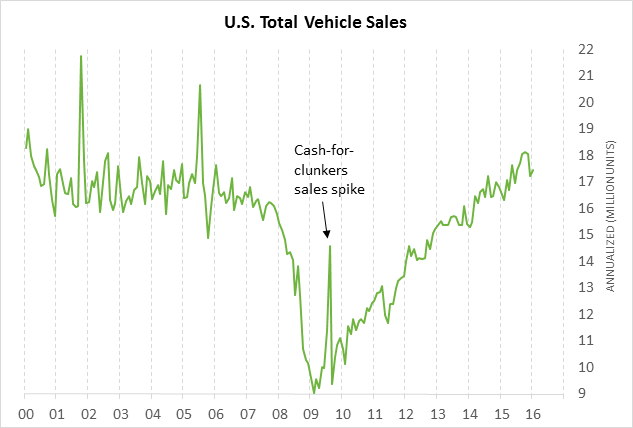

U.S. vehicle sales expected to regain some strength — The market is expecting today’s Feb total vehicle sales report to improve to 17.70 million units from 17.46 million units in January. U.S. vehicle sales remain in generally strong shape, helping to support the U.S. manufacturing sector and illustrating that U.S. consumers are confident about their finances.

Total vehicle sales posted a 10-1/2 year high of 18.12 million units in Oct 2015, fell back in Nov-Dec, and then showed a small increase in January. January’s vehicle sales level of 17.70 million units was better than the average of 17.0 million units seen in 2000/05 before the Great Recession emerged, illustrating that vehicle sales are currently at a stronger level than they were before the recession.

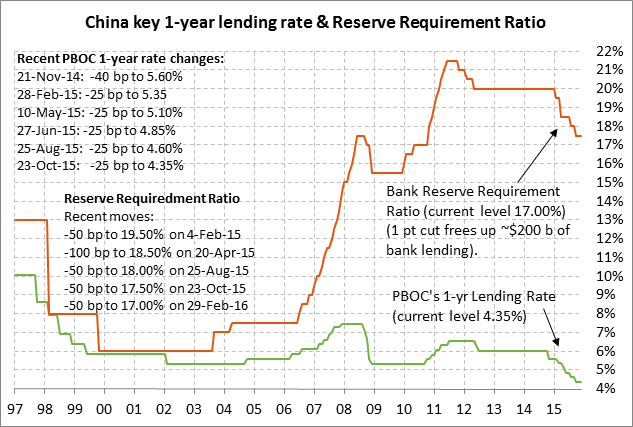

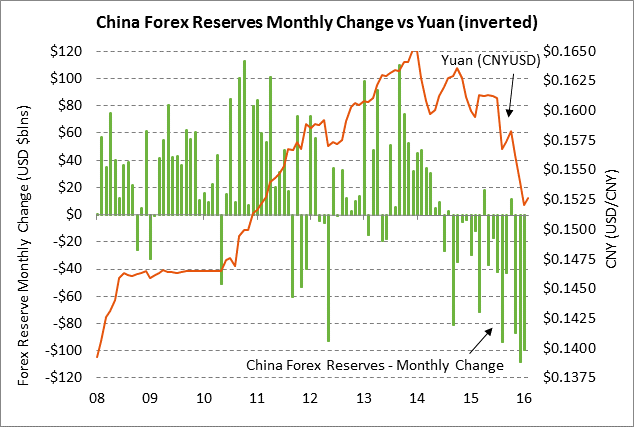

China takes limited monetary stimulus action by cutting reserve ratio in order to avoid sparking new weakness in the yuan — The Chinese central bank (Peoples’ Bank of China or PBOC) on Monday announced a surprise 50 bp cut in the bank reserve requirement ratio to 17% effective March 1. The action will free up about 685 billion yuan ($105 billion) of bank lending since banks can now support a higher level of lending with the same level of reserves. The PBOC over the past year has cut the reserve requirement ratio by a total of 3 percentage point to 17% from the 20% level that prevailed during 2012-14. In a parallel stimulus move, the PBOC since late 2014 has cut its 1-year lending rate by a total of 165 bp to 4.35% from the 6% level that prevailed during 2012-14. The PBOC has been cutting its benchmark lending rate and freeing up bank reserves in an effort to engineer a soft landing for the Chinese economy.

The markets on Monday were initially a little disappointed that the Chinese government did not announce any specific stimulus measures during the 2-day G-20 meeting that was held in Shanghai on Friday/Saturday. However, the PBOC did, in fact, follow through with a stimulus measure on Monday after the markets closed.

The PBOC may have timed the cut in the reserve ratio to set a more bullish stage for the Chinese economy and stock market ahead of the National People’s Congress which begins this coming Saturday and will last about two weeks. China’s legislature at this meeting will discuss policies for 2016 and for China’s next 5-year plan. The Chinese government wants to avoid any embarrassment during the 2-week legislative session that would stem from any fresh plunge in the yuan and/or the stock market.

The PBOC undoubtedly cut the reserve requirement ratio, rather than cut interest rates another notch, in an effort to provide some additional stimulus to the economy without greasing the skids for further yuan losses. A rate cut would have likely prompted renewed weakness in the yuan, which in turn would have undercut the stock market. Instead, the government appeared to be trying to demonstrate that it can meet the dual policy goals of stimulating the economy while avoiding further yuan depreciation.

The PBOC announced the reserve ratio cut after the Chinese markets had already closed on Monday. That means that the global markets will have to wait until Tuesday’s China open to better gauge the extent to which the move might spark new weakness in the yuan and whether the Chinese stock market gets a sustained boost from the cut.

EIA report — The market consensus for Wednesday’s weekly EIA report is for a +2.75 million bbl rise in U.S. crude oil inventories, a -1.5 million bbl decline in gasoline inventories, a -1.5 million decline in distillate inventories, and a -0.4 point drop in the refinery utilization rate to 86.9%.