- Markets adjust to FOMC’s hawkish shift

- Biden says passing BBB bill could take “weeks”

- Covid infection rates remain high as U.S. waits for omicron to fully hit

Markets adjust to FOMC’s hawkish shift — The markets yesterday continued to react to the FOMC’s decision on Wednesday to accelerate QE tapering and adopt a much steeper forecast for funds rate increases over the next several years.

The S&P 500 index yesterday closed -0.87%, giving back more than half of Wednesday’s post-FOMC rally of +1.63%. Meanwhile, the Nasdaq 100 index yesterday closed sharply lower by -2.61%, more than reversing Wednesday’s +2.35% rally.

Tech stocks were hard-hit on Thursday as the market looks forward to several years of steadily-rising interest rates, which will reduce the present value of richly-valued stocks. On a more immediate basis, tech stocks were hit Thursday by a -10% plunge in Adobe after it forecasted full-year revenue that missed estimates.

The plunge in Adobe also undercut other technology stocks, with Xilinx (XLNX) closing down more than -8%, Nvidia (NVDA) closing down more than -6%, Advanced Micro Devices (AMD), Tesla (TSLA) and Qualcomm (QCOM) closing down more than -5%, and NXP Semiconductors (NXPI) and Applied Materials (AMAT) closing down more than -4%. Apple (AAPL) closed down more than -3% to lead losers in the Dow Jones Industrials.

Homebuilding stocks on Thursday also took a hit as the market expects steadily rising mortgage rates. Homebuilders were also undercut by a -4% fall in Lennar (LEN) after it forecast 14,800-15,100 new orders for homes in Q1-2022, weaker than the consensus of 15,500. Other homebuilders also retreated, with DR Horton (DHI) and PulteGroup (PHM) closing down more than -2%.

While stocks saw some rough sledding on Thursday, the T-note market staged a rally as the market gained some confidence that the Fed’s tougher monetary stance will tame inflation. March 10-year T-notes on Thursday closed up +20 ticks, and the 10-year T-note yield fell -4 bp to 1.42%.

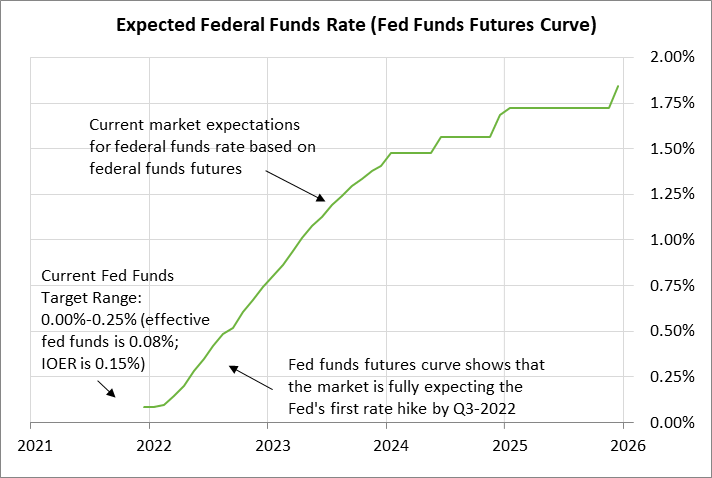

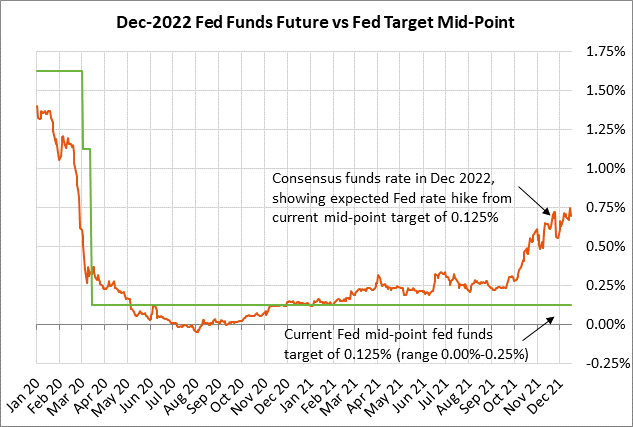

The FOMC on Wednesday announced that it will double the speed of its QE tapering, thus ending its QE program by March 2022, three months earlier than originally announced. That will give the Fed the option to start raising interest rates as soon Q2-2022. Also, FOMC members in their dot-plot forecasted three rate hikes for 2022, likely one per quarter from Q2 through Q4. FOMC officials are then predicting three more rate hikes in 2023 and two more rate hikes in 2024. That path would leave the funds rate at 2.1% by the end of 2024, up by two full percentage points from the current level, spanning the 3-year period of 2022-24.

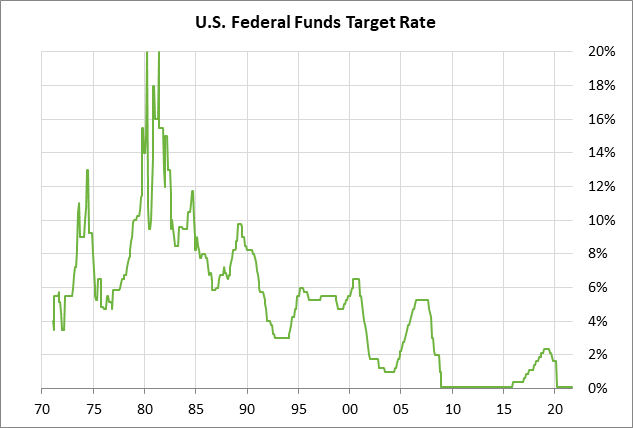

That would be a slower rate-hike path than the one seen in 2017-18 when the Fed raised the funds rate by a total of two percentage points over just two years from 0.375% in late 2016 to 2.375% by the end of 2018. In that episode, the Fed realized it raised rates too quickly due in part to the plunge in stocks at the end of 2018. The Fed was then forced to cut the funds rate by -75 bp to 1.625% by late-2019 to steady the economy and the stock market.

The Fed never had a chance to see if that 75 bp rate cut in the second half of 2019 would be sufficient to revive the economy because the pandemic hit in early 2020. In response to the pandemic, the Fed was forced to slash the funds rate back to near-zero and implement another emergency QE program.

The stock market is hoping that the Fed this time around can properly thread the needle, raising interest rates by enough to curb the inflation threat while not sending the economy and stock market into a tailspin. The Fed has its work cut out for it because the U.S. economy by the second half of 2022 may start slowing on an inventory surge and subsequent economic bust. The Fed’s challenge will be to see if it can successfully let the air out of the current epic boom, without causing a bust on the back-end.

Biden says passing BBB bill could take “weeks” — President Biden released a statement Thursday saying that negotiations on the BBB bill will continue “over the days and weeks ahead,” recognizing that the BBB bill is extremely unlikely to pass the Senate next week. The bill has not yet been fully scrubbed by the Senate parliamentarian and Senator Manchin still has major objections to the bill.

The good news in Washington is that Congress in the past month has managed to avoid a government shutdown and a Treasury default. Congress late Tuesday approved a debt ceiling hike that will last until early 2023. Congress earlier this month approved a continuing resolution that will keep the U.S. government operating until February 18.

The stock market in early 2022 will resume its watch for whether Democrats pass the BBB bill, with its mixed impact for stocks of increased fiscal stimulus but higher corporate taxes.

Covid infection rates remain high as U.S. waits for omicron to fully hit — The 7-day average of new U.S. Covid infections was at 119,371 on Wednesday, which was just slightly below the 2-3/4 month high of 122,307 posted in early December. The markets are now waiting to see if the spread of the more-contagious omicron variant will cause a new surge in infections in early 2022.

The good news is that the U.S. vaccination rate continues to slowly climb. Bloomberg reports that 61.1% of the total U.S. population has now been fully vaccinated, and 16.9% have received a booster shot. In the past week, the U.S. has administered a hefty daily average of 1.55 million doses.