- House intends to approve Build Back Better bill by the end of this week

- U.S. retail sales expected to remain strong

- U.S. manufacturing production expected to rebound

- U.S. housing market index expected to remain strong

House intends to approve Build Back Better bill by the end of this week — Democratic House leaders aim to approve the Democrat’s $1.75 trillion Build Back Better social spending bill by the end of this week, before Congress leaves town for next week’s Thanksgiving holiday. House approval would set the Senate up to consider the bill in December.

However, it remains to be seen whether moderate Democratic House members will vote in favor of the bill this week if the CBO has not fully scored the amount of spending in the bill.

Democratic House moderates and progressives reached a deal last week whereby progressives voted in favor of the $550 billion infrastructure bill with the agreement that moderates would vote for the Build Back Better bill once they had enough information on the cost of the bill. Progressives are going to be very upset if moderates refuse to approve the bill by the end of the week.

In any case, Democratic squabbling over the Build Back Better bill will continue into December after Senators such as Manchin and Sinema put their final stamp on the bill. The question will be how much of the bill is left and whether House Democrats will be willing to sign off on the Senate’s revised bill.

President Biden yesterday signed the $550 billion infrastructure bill. The fiscal stimulus from that bill should be supportive of the economy as various infrastructure projects are carried out over the coming years.

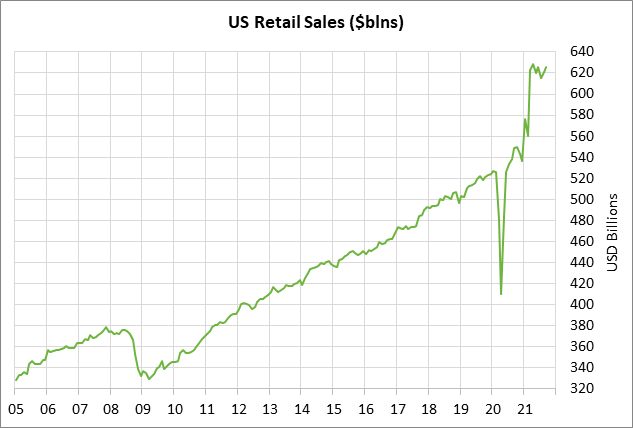

U.S. retail sales expected to remain strong — The consensus is for today’s Oct retail sales report to show a strong gain of +1.4% m/m and +1.0% m/m ex-autos, adding to September’s gain of +0.7% m/m and +0.8% m/m ex-autos.

U.S. consumer spending remains relatively strong as cnsumer spend their increased wages and the large amount of money they saved during the pandemic. U.S. retail sales in September reached $625.416 billion, which was only slightly below April’s record high of $628.751 billion and was up by +17% on a year-to-date basis.

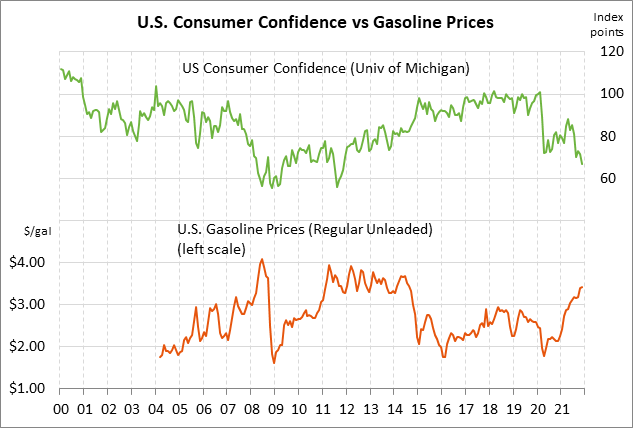

Yet, even as consumers spend money, they are pessimistic about the economic outlook. The University of Michigan’s U.S. consumer sentiment index has fallen in four of the last five months and fell to a new 10-year low in November. November’s index level of 66.8 was even worse than the low of 71.8 seen in April 2020 at the height of the pandemic economic shutdowns.

U.S. consumers remain concerned about the future as the Covid pandemic refuses to fade away and maintains its threat to the economy. The 7-day average of new U.S. Covid infections on Saturday rose to a new 1-month high of 84,113. That was up by +23% from the late-October 3-1/2 month low of 68,274.

U.S. consumers are also concerned about inflation and high gasoline prices, which are taking a bite out of their pocketbooks. Last week’s Oct CPI report showed an increase of +6.2% y/y for the headline CPI and a +4.6% y/y increase for the core CPI. On a 3-month annualized basis, the headline CPI was up +6.7% and the core CPI was up +3.8%.

Meanwhile, the average national price of regular gasoline is at $3.415 per gallon, which is just slightly below the 7-year high of $3.422 seen earlier this month.

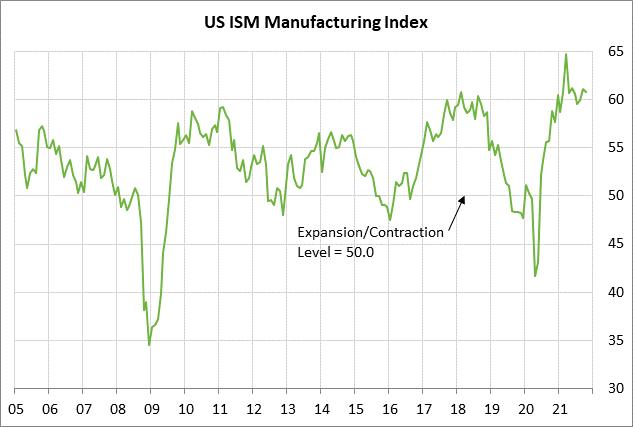

U.S. manufacturing production expected to rebound — The consensus is for today’s Oct U.S. manufacturing production report to show an increase of +0.8% m/m, which would more than reverse September’s decline of -0.7%. Meanwhile, Oct industrial production is expected to show an increase of +0.8% m/m, partially reversing September’s decline of -1.3% m/m.

U.S. manufacturing production has stumbled in the past two months, falling by -0.7% in September and -0.4% in August. U.S. manufacturing production has been hampered by supply chain and transportation disruptions.

However, U.S. manufacturing confidence remains strong, with the ISM manufacturing index in October at the high level of 60.8. U.S. manufacturers have a large backlog of orders to fill that should keep factories humming in the coming months.

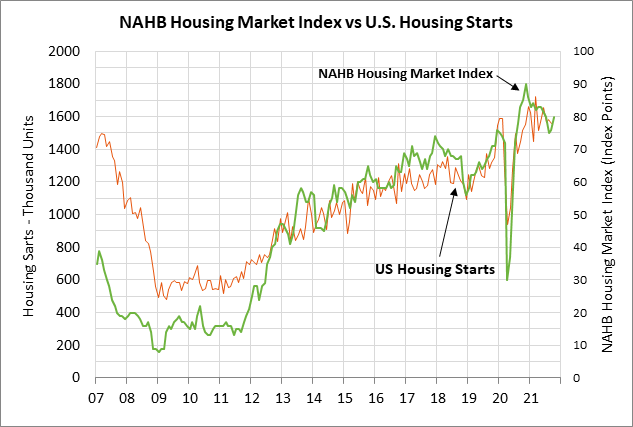

U.S. housing market index expected to remain strong — Today’s Nov NAHB housing market index is expected to be unchanged at 80, holding the +4 point increase to 80 seen in October. October’s strong housing index level of 80 was just 10 points below the record high of 90 seen in November 2020.

U.S. homebuilder confidence remains very strong thanks to continued strong demand for homes and low mortgage rates. The current 30-year mortgage rate of 2.98% is well below this year’s high of 3.18% posted in April and is far below the pre-pandemic level of 3.74% seen at the end of 2019.