- Weekly market focus

- QE tapering appears to be a go for this week’s FOMC meeting

- Democrats continue to hash out reconciliation bill

- U.S. ISM manufacturing index expected to show mild decline but remain strongÂ

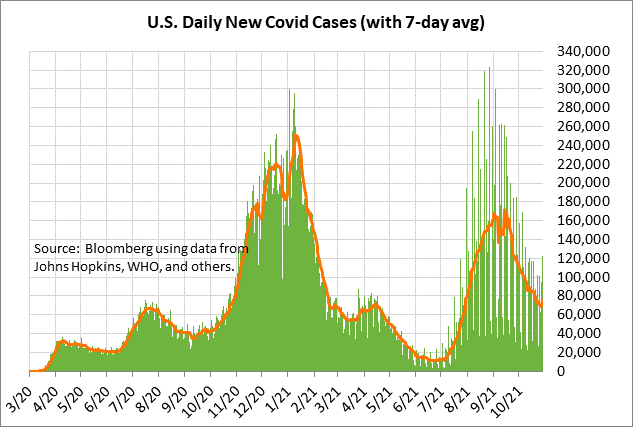

- U.S. Covid infections are down by -56% from September’s high

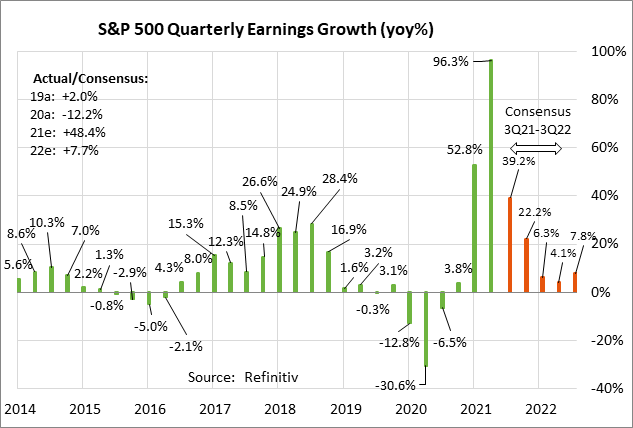

- Q3 earnings season reaches its peak

Weekly market focus — The markets this week will focus on (1) anticipation of this week’s FOMC meeting where the Fed is expected to announce QE tapering, (2) whether the Covid infection figures continue to decline, (3) Q3 earnings season with 167 of the S&P 500 companies reporting this week, (4) oil prices as OPEC+ meets Thursday to decide whether they will stick with their plan to raise monthly production by only +400,000 bpd, and (5) any carry-over from the ongoing debt crisis among Chinese property developers led by Evergrande.

QE tapering appears to be a go for this week’s FOMC meeting — Fed Chair Powell indicated on October 22 that the FOMC at this week’s meeting is likely to announce QE tapering, although he was careful to reiterate that the Fed is not close to raising interest rates. Mr. Powell said, “We are on track to begin a taper of our asset purchases, that, if the economy evolves broadly as expected, will be completed by the middle of next year.” He added, “I do think it is time to taper and I don’t think it is time to raise rates.”

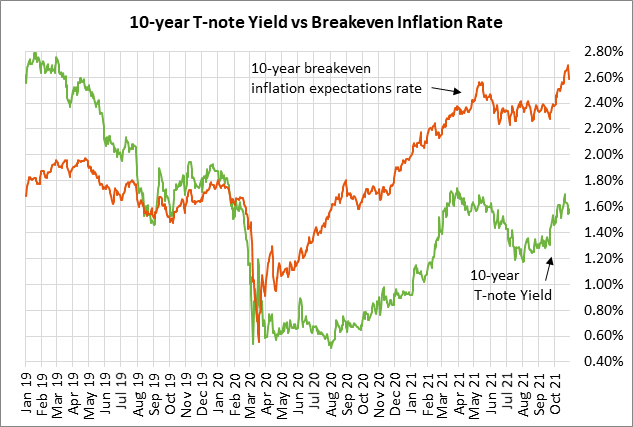

The markets seem to have already fully discounted a QE tapering announcement this week since Fed officials have been very clear about telegraphing that move. However, the markets are now concerned that the current surge in inflation will force the Fed into raising interest rates sooner than earlier expected.

As of this past summer, the markets were not expecting the Fed’s first rate hike until early 2023. However, the inflation situation has since turned more alarming and the markets have quickly accelerated expectations for Fed rate hikes. The 10-year breakeven inflation expectations rate last Wednesday rose to a 9-year high of 2.70%, although the rate then eased to 2.54% later in the week as oil prices fell back. As a result of the poor inflation outlook, and hawkish central banks overseas, the market is now discounting a very strong likelihood of two +25 bp Fed rate hikes by the end of 2022.

Democrats continue to hash out reconciliation bill — President Biden last Thursday announced a framework agreement for the reconciliation bill involving $1.75 trillion of spending and $2 trillion of revenue. The good news in the plan for the stock market was the confirmation that there will be no general rise in corporate tax rates. However, the plan would impose a minimum 15% domestic and global tax rate, and the plan contains a tax on stock buybacks.

Democratic Senators Manchin and Sinema refused to say whether they would support the deal, reserving the right to look at the legislative language and quibble over individual measures. It was unclear whether Ms. Sinema was on board with the tax surcharge on taxpayers making more than $10 million in income per year.

House progressives last week dug in their heels and continued to refuse to vote in favor of the $550 billion infrastructure bill until the reconciliation bill is a done deal. House Speaker Pelosi wanted to hold a House vote on Thursday on the infrastructure bill but she was forced to pull the vote due to the recalcitrance of House progressives.

Democratic Senator Tim Kaine last Friday said he thinks the infrastructure bill will pass the House by the end of this week, but that the reconciliation bill might not be passed by the Senate until right before the Thanksgiving recess.

U.S. ISM manufacturing index expected to show mild decline but remain strong — The consensus is for today’s Oct ISM manufacturing index to show a -1.3 point decline to 59.8, more than reversing September’s +1.2 point rise to 61.1. The ISM index has fallen back from March’s 37-year high of 64.7, but remains in strong shape. The manufacturing sector has seen a deluge of orders and is struggling to keep up with filling those orders due to supply chain disruptions and the high cost of fuel and shipping.

U.S. Covid infections are down by -56% from September’s high — U.S. Covid infections have fallen sharply by -56% in the past 1-1/2 months from mid-September’s peak of 171,850, but are still more than six times higher than June’s temporary trough of 11,299. The 7-day average of new daily U.S. Covid infections last Tuesday fell to a new 3-month low of 68,274, but then bounced back up to 75,374 by Thursday.

The U.S. has administered a daily average of 1.09 million doses over the past week, according to Bloomberg. That figure has risen in the past several weeks due to booster shots. Bloomberg reports that 57.6% of the total U.S. population has now been fully vaccinated.

Q3 earnings season reaches its peak — Q3 earnings season reaches its peak this week with 167 of the S&P 500 companies reporting. Notable reports include Pfizer on Tuesday; Electronic Arts on Wednesday; and Moderna, Regeneron, Kellogg, and Expedia on Thursday.

The consensus is for Q3 earnings growth of +39.2% y/y for the S&P 500 companies, according to Refinitiv. Earnings season has been very positive, with 82% of reporting S&P companies having beaten the consensus, higher than the long-term average of 65.8% although below the 4-quarter average of 84.7%, according to Refinitiv. On a calendar year basis, S&P earnings growth in 2021 is expected to be stellar at +48.4%, but is then expected to fade to +7.7% in 2022.