- U.S. inflation expectations soar to 9-year high, raising expectations for Fed tightening

- Manchin expresses doubt Democratic spending deal will meet today’s target

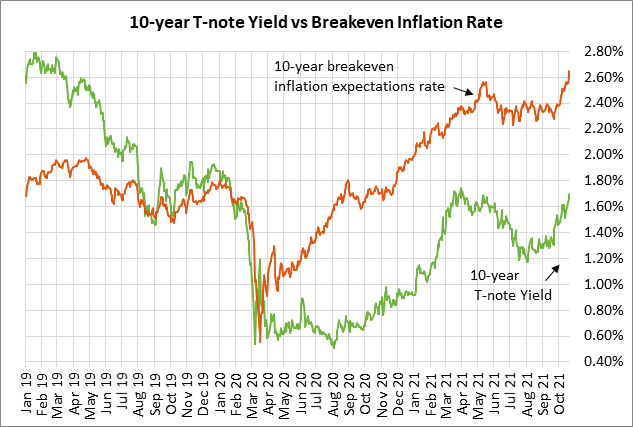

U.S. inflation expectations soar to 9-year high, raising expectations for Fed tightening — The 10-year breakeven inflation expectations yesterday rose by +5 bp to a new 9-year high of 2.65%. The breakeven rate has risen sharply by a total of +10 bp in just the past two days and by a total of +35 bp since September 21.

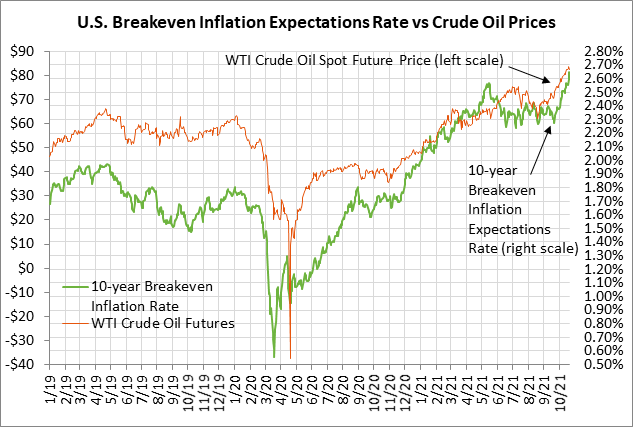

Inflation expectations have risen sharply in the past several weeks partly because of the rally in crude oil prices, which has raised fuel costs for businesses and consumers. The nearest-future WTI crude oil contract reached a 7-year high of $84.25 per barrel on Wednesday, before easing a bit to $82.50 on Thursday. WTI futures in the past 7 weeks have rallied sharply by a total of +23% from the $68.59 level seen on September 1.

Oil prices have rallied mainly because oil demand has recovered faster than OPEC+ has been raising production, causing a global oil deficit and falling inventories. A report from JPMorgan Chase on Thursday warned that if crude oil withdrawals from Cushing continue at the current pace, the WTI storage hub could run out of crude in weeks and push crude prices into “super backwardation” as Cushing’s “operational tank bottoms are likely 20%-25% of capacity,” or about 20 million bbl. The EIA reported Wednesday that crude supplies at Cushing, the delivery point of WTI futures, fell -2.32 million bbl to a 3-year low.

Meanwhile, natural gas prices have blasted off as well, also raising costs for businesses and consumers. The nearest-futures natural gas price rallied to a 7-1/2 year high of $6.466 per MMBtu in early October, up by +158% from the $2.50 level seen as recently as April. Natural gas prices have fallen back in the past two weeks but are still sharply higher than levels seen this past summer.

Natural gas prices have rallied on recovering demand and tight inventories. The EIA reports that U.S. nat-gas inventories are down -11.8% y/y and -4.2% below their 5-year average. The situation is even tighter in Europe, where nat-gas inventories are at the lowest levels in more than ten years.

Commodity prices in general have rallied sharply in the past two months, boosting by recovering demand and lagging supplies. The Bloomberg Commodity index is up +32% on a year-to-date basis.

Inflation expectations have been driven higher, not just by the increase in raw commodity prices, but also by increased prices for a range of goods and services. Some of the price increases are due to a surge in demand in areas of the economy that were hard-hit by the pandemic. Many other price increases are due to supply-chain disruptions and higher shipping and transportation costs.

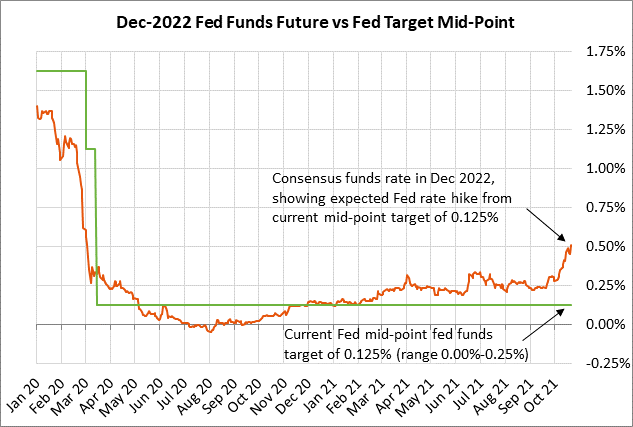

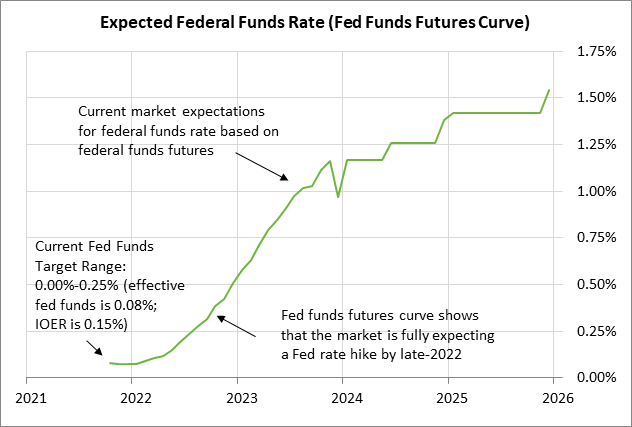

The sharp increase in inflation expectations is leading to expectations that the Fed will be forced to raise interest rates sooner than earlier thought. As recently as this past summer, the markets were not expecting the Fed’s first rate hike until early 2023. However, the market is now discounting the Fed’s first rate hike by Q3-2022 and a likely second rate hike in Q4-2022.

The December 2022 federal funds futures contract (on a yield basis) yesterday rose to a new 1-1/2 year high of 0.51%, up by 25 bp from the 0.235% level seen on September 1. That indicates that the market is expecting an overall Fed rate hike of +43 bp by December 2022 from the current effective federal funds rate of 0.08%. That translates to 100% expectations for one Fed rate hike by December 2022, and a 76% chance of a second rate hike by December 2022.

The sharp rise in inflation expectations, combined with increased expectations for up to two Fed rate hikes in 2022, has taken a toll on the bond market. The 10-year T-note yield yesterday rose to a new 5-month high of 1.70%, which is just 7 bp below the 1-3/4 year high of 1.77% posted earlier this year in March.

Manchin expresses doubt Democratic spending deal will meet today’s target — Democratic Senator Manchin said yesterday that he doesn’t see how Democrats will be able to agree on a reconciliation bill by today’s target. Senate Majority Leader Schumer earlier this week mentioned today as a target date for getting a deal done. House Speaker Pelosi has her own target of getting the infrastructure bill and the reconciliation bill passed by the House by next Friday before highway spending programs expire on October 31.

However, Democrats are far apart on the overall size of the spending bill, and also on how to pay for the bill. Democrats are focused on trimming the size of the spending bill down to the $1.8-1.9 trillion area from the previous level of $3.5 trillion.

However, the negotiations were thrown into chaos earlier this week when Democratic Arizona Senator Sinema finally made her demands known and said she does not want any increase in the corporate tax rate, or in income or capital gains taxes on high-income taxpayers. Giving up those tax increases would blow a $1.35 trillion revenue hole in the plan, which might force further cuts in spending levels. Many Democrats want to fully pay for the spending bill so that they cannot be accused of boosting the national debt.

The stock market, of course, would be very pleased if Ms. Sinema gets her way and there is a smaller-than-expected hike in the corporate tax rate, or no rate hike at all. A higher corporate tax rate takes a direct bite out of after-tax earnings and thus stock prices.