- Democratic spending bill shape-shifts as Sinema rejects tax hikes

- U.S. existing home sales expected to remain strong

- LEI expected to remain strong

- Unemployment claims expected to show continued labor market strength

- 5-year TIPS auction

Democratic spending bill shape-shifts as Sinema rejects tax hikes — The Democratic spending bill is changing shape quickly as the Wall Street Journal and other media outlets reported Wednesday that Democratic Arizona Senator Sinema is rejecting higher taxes on corporations and high-income taxpayers. Her demand has led the White House to consider other revenue-raisers such as taxing billionaires and stock buy-backs.

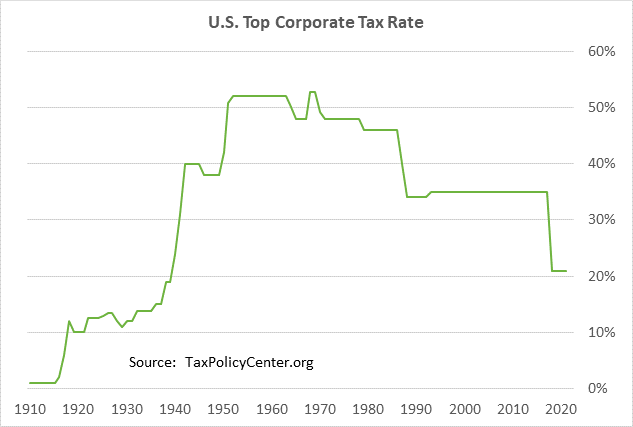

The stock market, of course, would be very pleased if there is a smaller-than-expected hike in the corporate tax rate. A higher corporate tax rate takes a direct bite out of after-tax earnings and thus stock prices.

Republicans in 2017 slashed the corporate tax rate to 21% from 38%. House Democrats have been focused on raising the tax rate to 26.5%, below President Biden’s initial plan of 28%. However, Senator Manchin has said he would support a hike to only 25%. It now turns out that Senator Sinema is now saying she wants no corporate tax hike at all.

Democrats may be forced to further trim the size of their spending bill from the current target of $2 trillion if they have to give up some of their tax-hike plans. According to the WSJ, the hike in the corporate tax rate is worth $540 billion over a decade, while the hike in income and capital gains taxes on high-income taxpayers is worth nearly $800 billion. Democrats have no way to easily fill that $1.34 trillion revenue hole. There are many Democrats that want to pay for the entire spending bill so that they are not open to charges that they are boosting the national debt.

The fact that the Democrat’s plan has been thrown up in the air will make it much more difficult to meet Senate Majority Leader Schumer’s goal of having a framework deal by the end of this week. The new chaos also makes it less likely that House Speaker Pelosi will meet her goal of passing the $550 billion infrastructure bill and the reconciliation bill by the end of next week. However, Democrats are desperate to get a final deal and are showing enough flexibility that they may still be able to get an agreement within a matter of days.

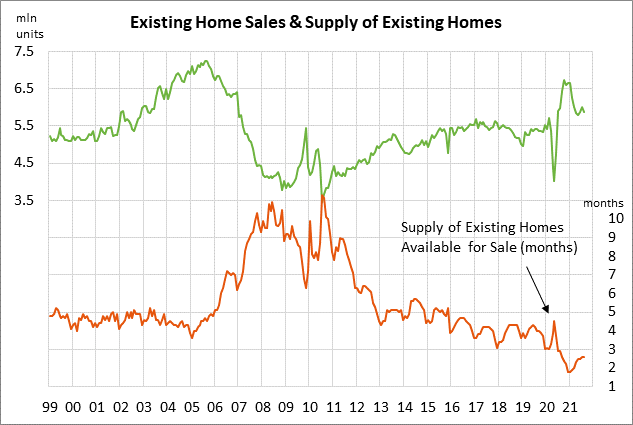

U.S. existing home sales expected to remain strong — The consensus is for today’s Sep existing home sales report to show a +3.6% m/m increase to 6.09 million, more than overcoming August’s -2.0% decline to 5.88 million. Home sales have fallen sharply by -13% from last year’s upward spike to a 15-year high of 6.73 million units in October 2020. However, home sales are still relatively strong and are +7% above the pre-pandemic level of 5.51 million units seen in December 2019.

Home sales continue to be hurt by the lack of homes available for sale. The supply of existing homes available on the market was at only 2.6 months in July and August, which is well below the average of about 4 months seen in the several years before the pandemic.

Home sales have also been hurt as some potential home buyers have refused to pay the extremely high prices for the homes that are on the market. The FHFA home price index has surged by +24% from the pre-pandemic level, and the index is up +11% on a year-to-date basis.

However, home sales remain generally strong due to pent-up demand. There are still a large number of people who are looking to move to larger homes, move to vacation areas, or escape from multi-family units. Also, the low level of mortgage rates continues to be a major bullish factor for home sales. The 30-year mortgage rate has risen to a 6-month high of 3.05%, but that is still well below the pre-pandemic level of 3.75% seen at the end of 2019.

LEI expected to remain strong — Today’s Sep leading indicators report is expected to show continued strength, with a +0.4% m/m increase that would add to August’s +0.9% increase. The LEI has risen sharply by +6.8% on a year-to-date basis, illustrating the strong economy. The consensus is for very strong GDP growth this year of +5.8%. However, GDP growth is then expected to ease to +4.0% in 2022 and +2.4% in 2023.

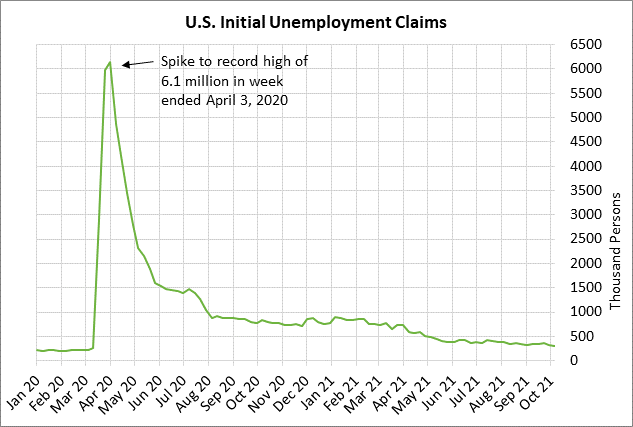

Unemployment claims expected to show continued labor market strength — The consensus is for today’s weekly initial unemployment claims report to show a +4,000 increase to 297,000, but that would only retrace a small portion of the declines of -35,000 and -36,000 seen in the past two weeks. Initial claims last week fell to a new 1-1/2 year low of 293,000 and were only 77,000 above the pre-pandemic level.

Today’s continuing claims report is expected to show a decline of -45,000 to 2.548 million, adding to last week’s sharp decline of -134,000 to 2.593 million. Continuing claims are in strong shape as the series fell to a new 1-1/2 year low last week. The series is now elevated by only +885,000 from the pre-pandemic level.

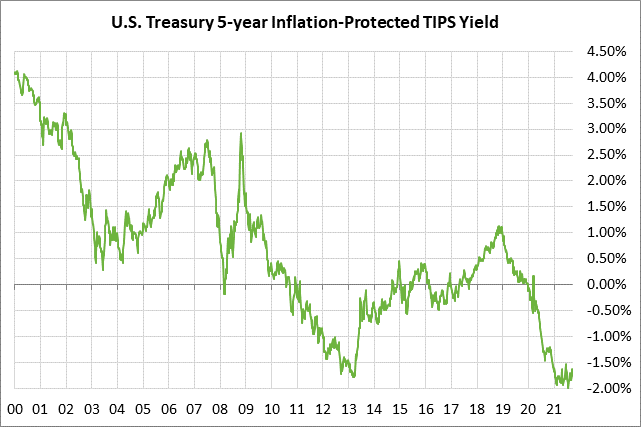

5-year TIPS auction — The Treasury today will sell $19 billion of new 5-year TIPS. The benchmark 5-year TIPS yield on Wednesday closed at -1.72%.

The 12-auction averages for the 5-year TIPS are as follows: 2.69 bid cover ratio, $43 million in non-competitive bids, 4.8 bp tail to the median yield, 22.1 bp tail to the low yield, and 51% taken at the high yield. The 5-year TIPS is the second most popular security behind the 30-year TIPS among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 71.5% of the last twelve 5-year TIPS auctions, which is well above the median of 63.7% for all recent Treasury coupon auctions.