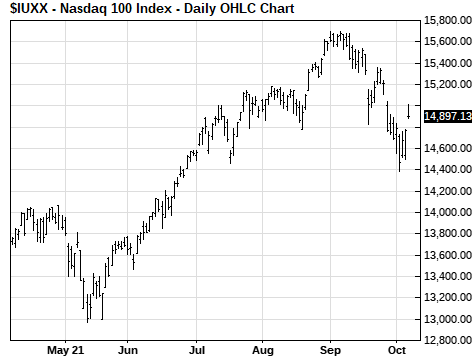

- U.S. payroll report may determine whether FOMC tapers QE at its next meeting

- Senate passes debt ceiling increase but it still has to be passed by the House

U.S. payroll report may determine whether FOMC tapers QE at its next meeting — Today’s Sep unemployment report is particularly important because it will be the last unemployment report before the next FOMC meeting on November 1-2.

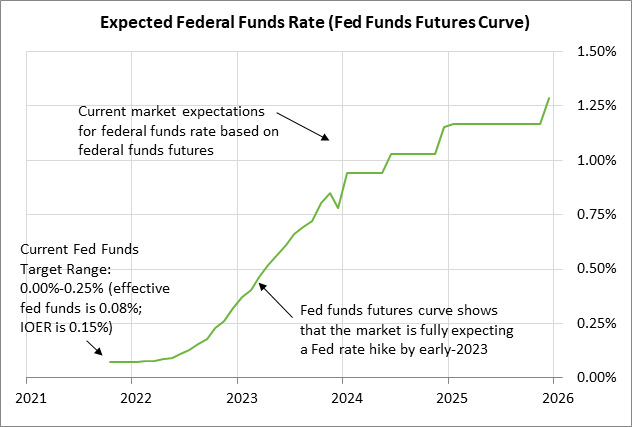

If today’s report indicates “substantial further progress” in the labor market, then the FOMC is more likely to proceed with announcing QE tapering at its next meeting on November 1-2. By contrast, if today’s payroll report is surprisingly weak, such as below +200,000, the FOMC may wait until its December meeting to decide on QE tapering. In any case, the markets are fully expecting the FOMC to announce QE tapering by the end of this year.

The sharp drop in Covid infection rates since mid-September is likely to give the Fed more confidence that the pandemic’s resurgence is over and that Covid infection levels may be permanently headed to much lower levels.

The consensus is for today’s Sep nonfarm payroll report to show an increase of +500,000. The markets are hoping for an improvement in payroll growth after August’s disappointing report of +235,000, which was far below market expectations of +620,000.

There was good news on the labor front on Wednesday. Sep ADP employment rose by +568,000, which was substantially better than expectations of +430,000 and an improvement from the ho-hum increases of +326,000 in July and +374,000 in August.

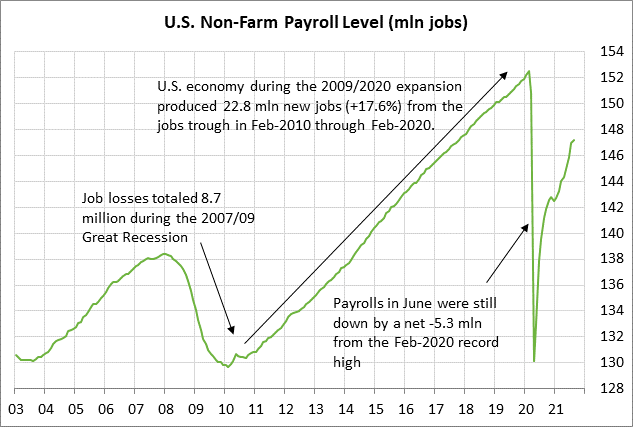

Payroll growth sizzled from May through July as the pandemic eased (May +614,000, June +962,000, July +1.053 million). However, payroll growth then fizzled in August.

Job growth this summer was negatively impacted by the resurgence of the pandemic caused by the delta variant. Businesses pulled back to see how long the pandemic resurgence would last and the extent to which the economy would be hurt. Also, vulnerable sectors were hurt, such as restaurants, travel, and entertainment.

Job gains were curbed in August as the Covid infection figures continued to climb through the month. The 7-day average of daily U.S. Covid infections rose steadily during August, beginning the month at 69,942 and ending the month at 162,273. The 7-day average didn’t peak until mid-September at 171,850.

The good news is that the 7-day average of daily U.S. Covid infections has steadily declined since the mid-September peak and fell to a 2-month low of 101,468 on Wednesday. The decline in the infection rate may have come too late to produce big job gains in September, but the fading pandemic seems likely to produce much better job figures by October. The expiration of enhanced unemployment benefits in early September is expected to give today’s payroll report a boost as more people were pushed into taking a job.

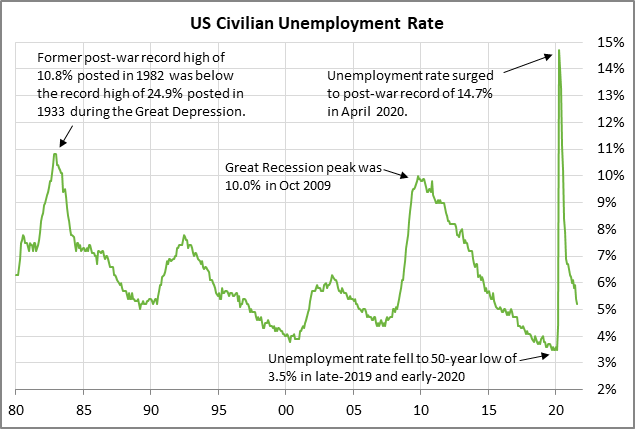

The consensus is for today’s Sep unemployment rate to fall by another -0.1 point to 5.1%, adding to August’s -0.2 point decline to a 1-1/2 year low of 5.2%. The current unemployment rate of 5.2% is still well above the record low of +3.5% seen prior to the pandemic.

Senate passes debt ceiling increase but it still has to be passed by the House — The Senate on Thursday night approved a debt ceiling hike after a long day of wrangling over the details. However, the House still has to vote on the debt ceiling hike, meaning that House Speaker Pelosi has to call House members back from recess. That means a vote may not happen until Monday or Tuesday. Even so, Congress should easily have the debt ceiling hike passed before Treasury Secretary Yellen’s drop-dead date of October 18.

Senate leaders agreed on a $480 billion debt ceiling hike that will last until December 3, which is the same date the continuing resolution expires. If Congress does not act in time, there will be a dual crisis after December 3, i.e., a U.S. government shutdown and the threat of a Treasury default.

Senate Majority Leader Schumer seems to want a combined spending bill and debt ceiling suspension passed by December 3. However, that is a recipe for further bipartisan conflict since Senate Minority Leader McConnell has insisted that Republicans will filibuster any debt ceiling suspension. Yet, Mr. McConnell may allow Democrats to pass a dollar-value debt ceiling hike, which Republicans would then use to pummel Democrats with campaign ads ahead of the November 2022 mid-term elections.

Democrats continue to insist they will not use reconciliation to raise the debt ceiling. Nevertheless, they could include a debt ceiling hike in their $3.5 trillion reconciliation bill or pass a stand-alone debt ceiling reconciliation bill. The good news is that there are multiple ways for Democrats to pass a debt ceiling hike if they are willing to take some political heat for raising the debt ceiling by a dollar value.

The debt ceiling fix through early-December now gives Democrats more time to focus on trying to pass their $3.5 trillion spending bill and the $550 billion infrastructure bill. The stock market would like to see those bills pass since the fiscal stimulus would boost the economy, although the stock market is clearly not happy about the corporate tax hike in the reconciliation bill.

There may not be much progress on the bills next week since both the House and Senate will be on recess for the Columbus Day holiday. The Senate and House are both scheduled to return to Washington on Monday, October 18.